(Bloomberg Opinion) -- The U.K. government is calling on the nation’s pension funds to participate in an “investment big bang” by allocating more capital to domestic and long-term illiquid investments. It’s a proposal that’s short on detail and fraught with difficulties, and one that pension fund trustees should treat with an abundance of caution.

Prime Minister Boris Johnson and Chancellor of the Exchequer Rishi Sunak recently wrote an open letter to the overseers of Britain’s 2.6 trillion pound ($3.6 trillion) pension industry. They bemoaned foreign pension funds reaping the benefits of what they called “the fruits of U.K. ingenuity and enterprise,” and called on U.K. investors to “back British success stories and secure higher returns and better retirements.”

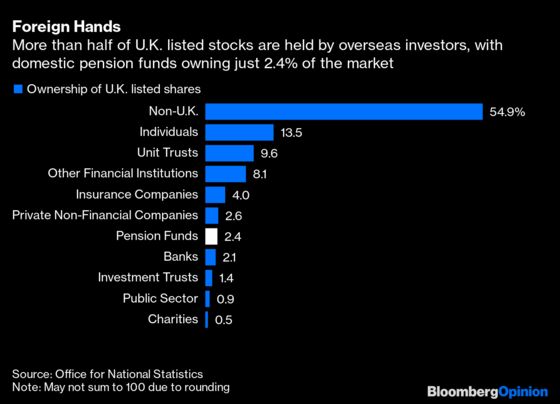

British institutional funds have definitely been putting more of their money offshore. The Pensions Policy Institute estimates that about a third of the equity holdings of U.K. pension funds are invested domestically, with the remaining 70% allocated to overseas stocks. Foreigners own more than half of U.K. listed stocks. Local pension funds own just 2.4%.

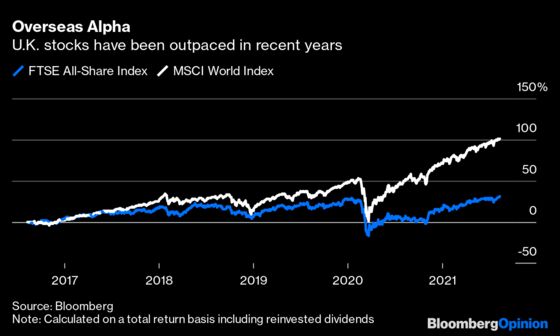

“Buying British,” though, would have been a losing strategy in recent years. The FTSE All-Share index has delivered a total return of just 30% in the past five years, with the MSCI World Index posting gains that are three times better.

In their letter, the government ministers argue that pension plans are missing out on potential returns because only a fifth of U.K. assets are in the form of listed securities. Public market investments, meantime, comprise more than 80% of pension plans’ allocations. Johnson and Sunak urge “a change in mindset and behavior among institutional investors.”

Investing in private equity is tricky, though. Clients of fund manager Neil Woodford found out to their cost when his firm blew up two years ago after loading up on illiquid stakes in closely held companies. Backing startups demands specialist expertise, as well as patience and, arguably, more than a modicum of luck.

As you’d expect, the people running pension portfolios pay most of their attention to the bulk of their holdings in public equities and debt. And specialist private equity firms charge higher fees for their services than pension funds pay for vanilla purchases in public markets.

Moreover, the increased scrutiny of environmental, social and governance concerns is already absorbing a lot of the attention of fund trustees, reducing their capacity to expand into new, riskier asset classes, no matter how much cajoling the government does.

The fragmentation of the pension industry is another obstacle. One of the stated aims of adding illiquid investments to a pension plan’s portfolio is to increase its diversification. But the average size of a U.K. pension plan is less than 300 million pounds, according to boutique investment bank Ondra Partners.

So the mismatch between the minimum layout required in private investments compared with the total assets available to many smaller pension plans can fatally undermine that strategy. “Often there is a minimum amount of 10 million pounds or more,” the Pensions Policy Institute said in a report published in May. “A scheme with AUM of 40 million pounds would not want a quarter in one investment.”

The gating of property funds has also tarnished the reputation of hard-to-sell assets and highlighted their incompatibility with daily dealing. After the 2016 Brexit referendum, trading in seven funds worth about $23 billion was halted amid a wave of redemptions. And as the pandemic began to spread in March of last year, funds overseeing about $13 billion closed to redemptions after the Association of Real Estate Funds said it was impossible to value their property holdings.

The government says it wants to marshal the nation’s long-term savings to secure “an innovative, healthier greener future.” Pension trustees have a fiduciary duty to take on the minimum risk possible while delivering adequate returns to finance retirements. They should be very wary of the government’s attempt to raid their members’ pension nest-eggs to pay for its utopian future.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.