Forget Trump’s Tax Cuts. Increases Are on the Horizon.

(Bloomberg Opinion) -- It’s pretty clear President Donald Trump’s tax cuts haven’t worked out as well for investors as many had hoped. Before too long they will have to start to worry about how stocks do after his tax increases kick in. (That’s right, there was some fine print in the president’s much self-promoted tax cuts.)

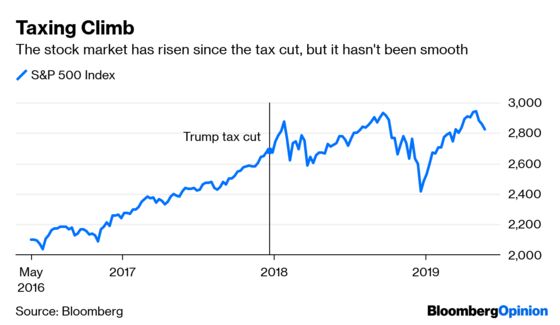

The market, as measured by the S&P 500, has returned 7.4% since Trump’s tax cuts were passed in mid-December 2017, and about 40% of that return comes from dividends. That’s not terrible, but it’s not great given the cost. The change in the corporate rate alone, according to my calculations, is on track to cost as much as $2 trillion over 10 years.

Stocks did rise before the law was passed, and the negatives of Trump’s trade policies plus the overall weakness of the global economy, some related to trade and some not, may be masking gains that came from the tax law. Corporate bottom lines are up. But still, what investors collectively are willing to pay for those earnings, perhaps because they are perceived as inflated, is not what it used to be. The average stock in the S&P 500 now trades for 16.5 times its next four reported quarters of profits, down from nearly 19 just before the tax bill was passed.

And the earnings outlook only gets murkier. To pass the tax bill, Trump and Republicans had to include provisions that would make it less costly. The net effect is essentially a corporate tax increase, and not a small one, with rising government levies as soon as 2022. Companies are already beginning to take notice.

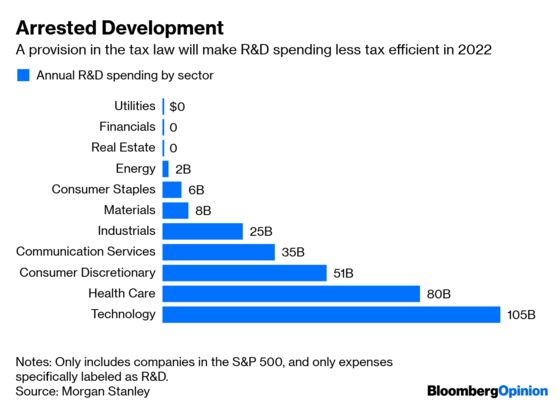

The biggest change will be for research and development. Companies have long been able to expense their R&D costs upfront, even if the product of that research ends up being a product or patent that could generate revenue for years. Recognizing those costs immediately, rather than spreading them over a number of years, like a company would do if it were to build a new plant, reduces near-time profits and therefore corporate tax bills. Starting in 2022, companies will have to amortize their R&D costs over five years, lowering the immediate expenses they can use to offset profits and therefore raising their tax bill. The following year, companies will also have to start phasing out a part of the tax bill that allows them to temporarily expense more of their capital expenditures upfront as well. That provision of the tax bill was meant to spur corporate investments, but it has had mixed results.

All told, strategists at Morgan Stanley estimate that the provisions, which they call tax cliffs, will cost corporate America as much as $800 billion over a decade, which they say is the equivalent of raising the federal corporate tax rate back up to 28%, or halfway back to what it was before the 2018 tax change. The biggest losers could be the big tech stocks, which spend more than $100 billion a year on R&D. The next largest R&D spender is health care. Utilities and financial stocks, two sectors with the lowest R&D spending, will see very little of the tax increase.

Figuring out how much that coming tax increase will dent stocks is a guessing game at this point. Congress could still vote to change the provisions so they don’t actually take effect. More important, analysts have not yet released their earnings estimates for 2022. Based on the market’s current multiple, an $800 billion hit to earnings would lower the value of stocks by about $1.3 trillion. But the rub is that while the change will increase corporate tax bills, that increased cost could be offset by the accounting gains of lower recognized R&D expenses. The big hit will be to corporate cash flows because companies will face higher tax bills along with their R&D expenses, which they will still have to pay for as they take place, even if they can no longer expense those bills immediately.

Lower cash flow will most likely mean less investment down the road and lower profits for companies, as well as some slowdown in economic activity, which could also cut into earnings. But the bigger lesson for investors is not to make decisions based on tax cuts, as attractive as they are in the beginning. The value of stocks, at least in theory, is based on all of the profits a company will make in its existence, and that’s a long time, far longer than tax cuts can maintain their youthful glow.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.