Forget Bitcoin or Tesla. Muni Bonds Are the King of Costly.

(Bloomberg Opinion) -- Believe it or not, the $3.9 trillion municipal-bond market and Bitcoin have much in common.

A flood of money pouring in? Check: Muni bond funds added about $2 billion in the week ended Feb. 17, according to Refinitiv Lipper US Fund Flows data, building upon a $2.6 billion inflow in the prior period that was the fourth-largest on record. Scarce supply? You bet: Some analysts estimate that states and cities in 2021 will bring to market the smallest amount of tax-exempt bonds in 21 years. Fiscal stimulus supporting its case? Indeed: The prospect of $350 billion in aid to state and local governments should help stave off any widespread credit stress.

Perhaps most remarkably, though, muni investors appear to have fully embraced the “HODL” mentality of the crypto crowd. In typical times, February’s sharp selloff in U.S. Treasuries, which has sent the benchmark 10-year yield up almost 30 basis points to 1.35% (for a monthly loss of almost 2%), would have reverberated by now across the market for state and local bonds. Instead, tax-exempt yields have been borderline immovable; they only finally started to budge toward the end of last week.

By that time, municipal bonds became arguably the most expensive asset class anywhere. As Bloomberg News’s Danielle Moran noted, yields had fallen so low on top-rated tax-free debt that even after accounting for the exemption from federal taxes, it still made more sense for investors to purchase Treasuries instead. It’s certainly fair to argue that Bitcoin isn’t worth more than $50,000, or that shares of Tesla Inc. shouldn’t be trading at more than 1,000 times earnings. But it’s at least possible to make the case that they should. It’s not every day that a corner of the bond market rallies to such an extent that it’s objectively a bad deal.

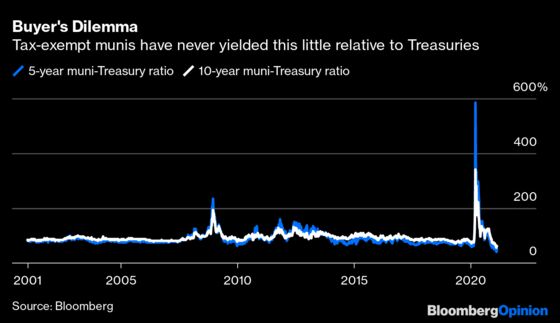

Because most municipal bonds are exempt from federal income taxes, analysts prefer to gauge the market’s relative value using the muni-Treasury ratio, which divides the yield on triple-A rated tax-free debt by Treasuries with the same maturity. A higher ratio indicates munis are relatively cheap — if it’s above 100, investors are effectively getting the tax exemption for free. A lower ratio signals munis are getting pricier.

If you believe the likes of Delaware, Maryland, North Carolina, Texas and Virginia are roughly as creditworthy as the federal government, then it’s only natural that their yields would be lower than Treasuries. For those in the top tax bracket, a 1.35% taxable yield like that on 10-year Treasuries is equivalent to a 0.85% tax-free yield. The market usually never reaches that breaking point.

That all changed last week. The 10-year muni-Treasury ratio tumbled to a record low 54%, meaning tax-exempt bonds were barely paying half of 10-year U.S. notes. The 30-year ratio crumbled to 69% — before this year, the previous low was 86%. And for five-year securities, the muni-Treasury ratio dropped to a puny 37.3%. According to Bloomberg Valuation data that tracks bond yields for 20 different states, five-year debt from all but Illinois and New Jersey yields less than five-year Treasuries, and many state obligations would yield less even after factoring in the tax exemption.

It’s not as if this caught anyone in the muni market by surprise. Citigroup Inc. analyst Vikram Rai called it “excruciating richness.” John Flahive, head of fixed-income investments at BNY Mellon Wealth Management, said “you really gotta scratch your head” at valuations. Bank of America Corp.’s strategists called it “futile” to call a bottom to muni-Treasury ratios. Adam Stern, co-head of research at Breckinridge Capital Advisors, said, “We’re trying to find value where we can, and if you can’t, hold your nose and move along.”

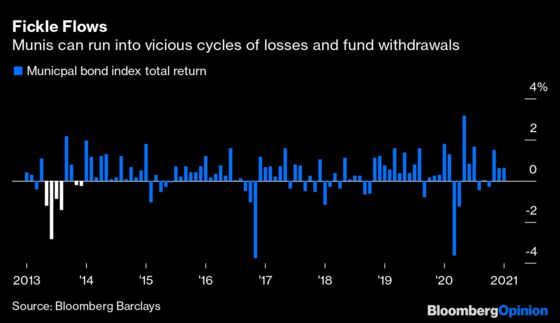

The unspoken fear here is that the muni market can be particularly susceptible to painful reversals. It’s dominated by individual investors who own shares of mutual funds or specific bonds in separately managed accounts. In either case, they tend to not react well to monthly losses on their supposed safe assets. The clearest example of this was in 2013, when a combination of the “taper tantrum” and high-profile distressed situations in Detroit and Puerto Rico led individuals to pull $60.7 billion from muni mutual funds that year, the most since at least 1992, as losses mounted in six of the final eight months of that year.

It doesn’t have to be that way this time around. From a pure public policy perspective, no one should root against low borrowing costs for states and localities that are on the front lines of keeping the Covid-19 pandemic in check and distributing vaccines. In fact, part of the reason tax-free bond supply looks to be so low this year is that municipalities are opting to sell more taxable debt, which is more costly upfront but grants them greater flexibility to use the proceeds.

But it’s also fairly obvious that muni-Treasury ratios can’t permanently remain at levels that make tax-exempt bonds borderline impossible to buy. One of the more troubling dynamics of this supply-demand mismatch is that fund managers are clearly reaching to purchase longer-dated debt or riskier securities. High-yield muni funds drew in $578 million in the week ended Feb. 17, after adding $832 million the week before, which was the second-biggest inflow ever. As is often the case in fixed-income investing, that strategy will work until it doesn’t.

Yes, if an investor in the top tax bracket is convinced that taxes are going to go much higher in the coming years, then it's possible to make the case that munis still have some value relative to Treasuries. But legislation could potentially work in the opposite direction, too.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.