(Bloomberg Opinion) -- Elon Musk likes to boast that Tesla Inc. is one of only two U.S. carmakers never to have gone bankrupt. The other one has been around for a bit longer.

Ford Motor Co. has certainly had its hairy moments, not least the 2008 financial crisis that upended General Motors Co. and Chrysler Corp. Back then, CEO Alan Mulally saved the company by mortgaging it down to the blue oval and streamlining it with gusto. Now the company must reinvent itself again, only this time because of Musk and his electrified, autonomy-aspiring bandwagon. It was a big deal in 2017 when its market cap was surpassed by Tesla’s. Now, with Tesla valued at almost a dozen Fords, the idea they were ever in the same ballpark seems quaint. Indeed, in finance terms, they occupy different universes.

One reading of Musk’s mini bombshell on Tesla’s last earnings call that it might be his last one (at least for a while) is that the company is becoming more normal, sporting profits and the other humdrum accoutrements of maturity. The market seemed to interpret it that way: Despite billion-dollar earnings, the stock fell. Even after analysts bumped forecasts, Tesla trades at 135 times forward earnings. What investors want here is a story of never-ending growth narrated by Musk. Black ink is nice but incidental.

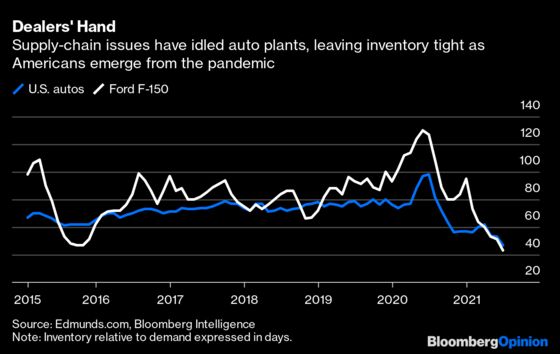

Ford’s results, delivered Wednesday evening, came with no bombshells — CEO Jim Farley runs a more conventional Q&A session — but also a surprise profit. Similar to Tesla, investors fretted over the damage inflicted on Ford by the great chip shortage, but it came with a silver lining: sparse dealer lots. So even as inflationary trends perturb Americans — and soaring prices for chicken wings have surely made it real for many — automakers that are accustomed to discounting metal are actually enjoying some pricing power. Inventory is way below normal levels across the industry, especially for Ford’s flagship F-150 truck. Meanwhile, higher used-car pricing, and thereby residual values, juiced Ford’s credit profits.

Musk frequently bemoans the difficulties of manufacturing. You could say Detroit’s problem is that it manufactures too well — as in, it builds a lot but not always what people want at a profitable price. One of the more interesting elements of Ford’s pitch on Wednesday evening was its expanding build-to-order bank. As underwhelmingly normal as that might sound in 2021, it isn’t for this industry. Apart from giving consumers greater control, online ordering offers Ford a clearer look at real demand and, thereby, a chance for sharper management of its production line. Managing its dealers might get trickier as the order bank gets bigger. But leaner lots look set to outlast the pandemic and chip shortage. Ford now aims for inventory at 50 to 60 days of demand, down from the usual 75.

Mundane as that may seem, delivering on it is as critical to Ford’s investment case as, say, the Cybertruck is for Tesla.

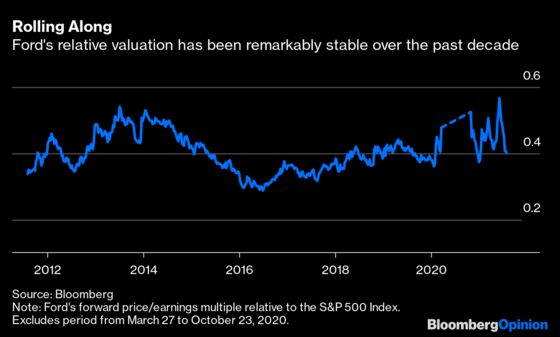

Tesla’s task is to grow into its stratospheric multiple. Ford’s is to just raise its multiple to high single digits or (heavens) double digits. It tends to drift between five to eight times earnings; relative to the S&P 500, its valuation has been pretty consistent.

Ford’s latest strategic update, in May, boosted its relative valuation briefly to the highest level of the past decade as the company unveiled plans to catch up on electrification, software updates and other Tesla-isms. Years of ambivalence have given way to the realization that a post-combustion plan is no longer blue-sky stuff for conference panels but the ante to stay in the game. On that front, Ford’s sharp turn means the excitement must be tempered. Tesla is a case study in the early pitfalls of industrial innovation, and there will be setbacks and recalls as the incumbents crank up their battery factories and AI labs.

Yet there are also hopeful signs, not least Ford’s claim that the Mustang Mach-E is already profitable at the bottom line. Apart from being remarkable for a sub-$50,000 electric vehicle less than a year old, it bodes well for next year’s release of the F-150 Lightning. The latter, which will now most likely beat the Cybertruck to market, is make-or-break for Ford, simultaneously defending its most important model and trying to reinvent it for a wider market.

That dual mission for its premier model captures Ford’s innovation diffculty neatly. Unlike Tesla, Ford must prove the billions it is spending on EVs will generate a decent profit, and quickly. Hence, its ability to nail the seemingly routine stuff of managing inventory and building to order is critical. Investors have an inherent distrust of the car business, especially when it is spending big. Demonstrating the traditional operations can be run profitably over time is the hurdle Ford (and others) must clear if they want a little slack on delivering the new stuff and the higher multiple that might go with that. Being Detroit’s least bankrupted automaker is, after all, praise of a decidedly backhanded nature.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.