Covent Garden Could Be the Ultimate Brexit Bargain

(Bloomberg Opinion) -- Brexit isn’t resolved yet, but takeover interest is already stirring in the deeply unloved U.K. commercial property sector. Controversial real estate tycoon Nicholas Candy is mulling a bid for the owner of London’s famous Covent Garden retail and leisure district. The ambition seems highly tentative right now. Even so, shareholders in the target — Capital & Counties Properties Plc — need to beware of letting this company slip away to an opportunistic bid from Candy or anyone else.

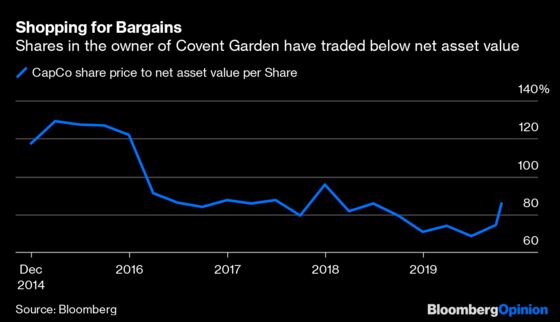

CapCo stock had dropped almost 50% between August 2015 and last Friday, before Candy’s interest was revealed by The Sunday Times newspaper. The main drag has been CapCo’s failure to develop a huge swathe of land in west London’s Earls Court, earmarked for largely residential use. That needs outside funds to get going. Brexit uncertainty, a softening London housing market and a complicated ownership structure have left the site undeveloped.

The company has a plan to deal with the problem: jettisoning its Earls Court stake, valued at 426 million pounds ($553 million) in the last accounts, and leaving someone else with the hard work of un-gumming the project. CapCo would then be focused on Covent Garden, valued at 2.6 billion pounds, and have extra funds to invest there.

But this separation is a work in progress. There are exclusive talks with a possible Earls Court buyer but no deal yet. Meanwhile, there are signs that negative sentiment around Brexit, and potentially London and U.K. real estate, may have bottomed out, judging by the recent bounce in sterling.

This is a natural moment therefore for any CapCo bidder to pounce, given that market uncertainty is lessening but the stock price remains depressed. The company’s net asset value was 315 pence per share at the end of June, when using Europe’s so-called EPRA standardized measure.

The shares haven’t traded at or above NAV for nearly four years. An offer at that level would represent an alluring 47% premium to the three-month stock price average, but only a lowish 26% premium to CapCo’s closing price on Friday. As such, a bid at the NAV level may not be enough. CapCo is not distressed and there’s only one Covent Garden.

It’s not clear whether Candy is really committed to a deal, and whether he could afford an offer. He talked with Saudi Arabia’s Public Investment Fund about possible financing, according to the Sunday Times. Yet Monday’s confirmation of takeover interest made no mention of that or any other funding source. Nor is it obvious what Candy could do differently to add value to these assets that would justify a chunky premium.

CapCo shareholders may be desperate for some good news. Still, the board needs to be on alert to repel approaches that are simply trying to pre-empt a re-rating of the London property market, or its own separation plan. For now, Candy’s interest provides some useful tension in the current negotiations over Earls Court. The company would be well advised to exploit it, and get a buyer for that asset on the hook fast.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.