Inflation ‘Near’ 2% Doesn’t Cut It Anymore for the Fed

(Bloomberg Opinion) -- In case it wasn’t obvious before the Federal Reserve’s January meeting on Wednesday, it should be crystal clear now: The central bank is obsessed with inflation.

One of the only changes to the Federal Open Market Committee’s statement was the following:

The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation returning to

nearthe Committee's symmetric 2 percent objective.

This was intentional. Chair Jerome Powell said during his Q&A after the statement was released that the goal of that tweak was to “send a clearer signal that we’re not comfortable with inflation running persistently below our 2% symmetric objective.” He added: “We’re not satisfied with inflation running below 2%, particularly at a time such as now where we’re a long way into an expansion and a long way into a period of very low unemployment when in theory inflation should be moving up.”

But even more tellingly, Powell made a clear, concise argument during his opening statement about exactly why the Fed is so determined to see inflation run hot, in what could very well be the consensus view among policy makers:

“While low and stable inflation is certainly a good thing, inflation that runs persistently below our objective can lead longer-term inflation expectations to drift down, pulling actual inflation even lower.

In turn, interest rates would be lower as well, closer to their effective lower bound. As a result, we would have less room to reduce interest rates to support the economy in a future downturn, to the detriment of American families and businesses.

We have seen this dynamic play out in other economies around the world, and we’re determined to avoid it here in the United States.”

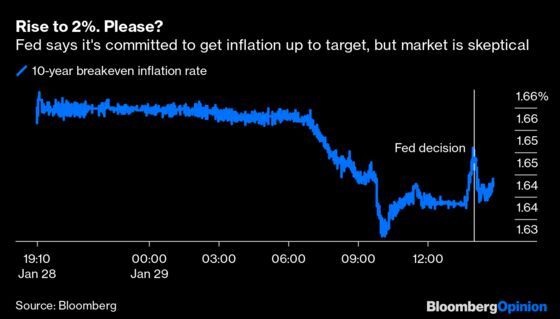

The 10-year breakeven rate, which reflects the difference between yields for nominal and inflation-linked Treasuries, expressed a healthy dose of skepticism that the Fed could simply move inflation higher with current monetary policy:

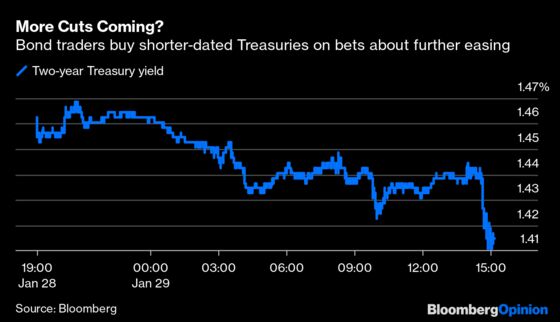

But more broadly, the $16.7 trillion U.S. Treasuries market took Powell’s inflation comments to mean that the Fed will consider lowering interest rates again, perhaps as soon as this year, if inflation doesn’t materialize. Two-year yields tumbled right about when Powell addressed inflation in his Q&A and continued to slide to near the lowest level since October:

At first glance, this would seem like an overreaction. Powell reiterated multiple times that the central bank views the current stance of monetary policy as appropriate and that it would take a material change in the economic outlook for it to alter course. Obviously, if the fed funds rate stays in a range of 1.5% to 1.75% for some time, buying two-year notes at a 1.41% yield is a poor wager.

But in what could be taken as a hint of what’s to come, he drew a distinction during the Q&A between the Fed’s “current framework” about inflation and an “average inflation targeting framework.” Under the former, the committee views price growth above and below 2% as equally concerning. That means inflation “near” target is just fine.

Under the latter, “near” might not be good enough. Indeed, with an average inflation targeting framework, “over time it would lead to a different approach to policy,” Powell said.

Whether that “different approach” means lower interest rates remains to be seen. But one thing has never been more clear: The Fed has no interest in raising interest rates anytime soon, no matter how long the economic expansion rolls on or how many records the stock market breaks. Not without persistently higher inflation.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.