(Bloomberg Opinion) -- After eight difficult years doing whatever it took to support Europe’s economies, Mario Draghi is about to step down as the president of the European Central Bank. In taking up this challenge, his successor, Christine Lagarde, faces the same underlying problem: The currency union at the center of the European project is unfinished work.

From the beginning, the euro has been incomplete by design. Its creators knew that to share a currency, countries must also share risks — as, for example, states in the U.S. do through federal institutions such as a common budget, social safety net and financial backstops. Otherwise, the centrifugal forces of divergent economies would threaten to tear the union apart. These essential mechanisms were left out, because member nations weren’t ready for the loss of sovereignty they would entail.

Visionaries such as Jean Monnet and Tommaso Padoa-Schioppa thought that the resulting crises would push Europe in the right political direction. To some extent, this has happened. The sovereign-debt debacle that began earlier this decade — and that brought Greece to the brink of abandoning the common currency — compelled Europe’s leaders to take steps toward deeper integration. They established elements of a banking union, for example, including centralized entities with the power to supervise, take over and shore up the region’s financial institutions.

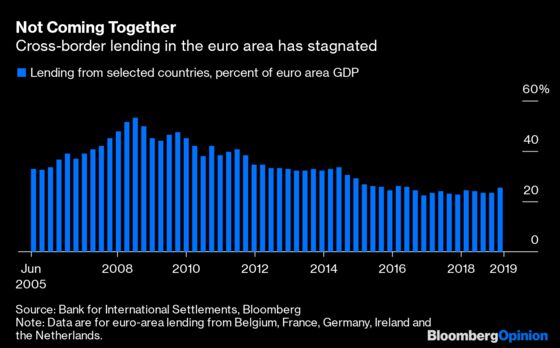

What remains to be done, though, dwarfs the progress that’s been made so far. Efforts to create a euro-area budget to mitigate recessions — as federal transfers do for states in the U.S. — have gone nowhere. And the banking union has stopped short of real risk-sharing: It won’t spend joint public funds on recapitalizations, and its “third pillar” — a mutual deposit-insurance system — is still only a proposal. As a result, measured by cross-border lending, financial integration in Europe has stalled.

The flaws in the euro’s structure have taken a heavy human, economic and political toll. Greece endured a depression and untold suffering that, in a proper risk-sharing union, would have been largely unnecessary. Draghi’s extraordinary efforts to hold the currency together — necessary as they were — depleted the ECB’s resources, leaving it ill-prepared to fight the next recession. Europe’s dysfunction shattered faith in the political establishment, contributing to the populist and right-wing resurgence that has swept across the Western world.

The U.K.’s bid to exit the EU should be seen as a warning: If the next country to leave is a member of the euro area, the whole enterprise — aimed at binding Europe together so that the horrors of two world wars would never happen again — could fall apart. The strategy of forging closer union through successive crises has reached its limits, achieving too little at far too great a cost, and undermining rather than building support.

This leaves Europe’s leaders with just one safe course: Find the will to act in relatively benign times, so that the next crisis won’t happen in the first place, or won’t be quite so painful if it does.

Now would be a good moment. Lagarde, who takes over from Draghi next month, knows from bitter experience what needs fixing in the euro area. In a way, Brexit helps too — both by highlighting the costs of disunity and by sidelining a reflexive opponent of European integration. Slow economic growth underscores the need for coordinated fiscal policy. And the abrupt change in U.S. trade policy from promoting global commerce to throttling it challenges Europe’s nations to stand together and defend their interests.

Naturally, obstacles abound — particularly in Germany, where politicians see any moves toward greater risk-sharing as anathema. That said, the incoming president of the European Commission, long-serving German cabinet member Ursula von der Leyen, is better placed than her predecessors to navigate her country’s politics.

Pretty much everybody recognizes what needs to be done. Here are the main elements, borrowed from a recent proposal by a group of French and German economists:

- Complete the banking union. Institute mutual deposit insurance and jointly pledge ample public funds to recapitalize banks when necessary, so that people will perceive a euro deposited in Germany as equivalent to a euro deposited in, say, Greece or Italy. To ensure that such backstops aren’t abused, require banks to operate with ample loss-absorbing capital and limit their investments in the bonds of their own governments. Grant more power and independence to the entities responsible for the financial system — such as the Single Resolution Board — so Europe’s leaders won’t have to convene an emergency summit every time a bank gets into trouble.

- Share more fiscal risks. Create a euro-area stabilization fund, which would gather contributions in boom times and provide emergency funds to members experiencing severe recessions. To enforce prudent policies, set up an independent council to establish spending caps, beyond which governments would have to finance expenditures with riskier junior bonds, creating market pressure to keep their finances in line. Finally, institute a sovereign bankruptcy mechanism that imposes losses automatically, to prevent public euro-area funds from being used to bail out private creditors (as happened in Greece).

- Break down barriers to the free flow of capital across Europe. Empower the European Securities and Markets Authority to harmonize financial, bankruptcy, accounting and other relevant rules, with the goal of encouraging people to invest — and hence diversify risk — across borders.

No doubt, this is a tall order, especially for a Europe whose people and leaders are suffering from crisis fatigue. Regardless, they need to rouse themselves. In the next crisis, Lagarde won’t be able to do what’s required on her own. Better that governments overcome this inertia now than during a new emergency that might just test the European project to destruction.

Editorials are written by the Bloomberg Opinion editorial board.

©2019 Bloomberg L.P.