Fiat Billionaires Can Extract a Price From Peugeot

(Bloomberg Opinion) -- Right now is a highly opportune moment for PSA Group boss Carlos Tavares to negotiate a merger with rival European carmaker Fiat Chrysler Automobiles NV. Shares in PSA, the owner of Peugeot, have had a great run in recent months, making them a strong deal-making currency. The flip side is that this is a reason for shareholders in Fiat to demand that any “merger of equals” actually includes a premium for them.

The two carmakers have relatively similar market capitalization but the precise details matter. Crunch the duo together at their closing market values on Tuesday and Peugeot shareholders would deserve to own 55% of the combination. The snag is they would then enjoy more than half of the future value creation from a deal. That’s a bit unfair: It takes two to tango. This could be solved by giving each side 50% ownership, but shrinking Peugeot via a big dividend ahead of the deal closing. That way each side would contribute an equal amount of equity value, and own and equal share of the bigger group.

But is it possible such an arrangement would still be unfair? Fiat shareholders, including the billionaire Agnelli clan, might think so based on what they’re putting in. For starters, Fiat’s sales and profits are bigger than Peugeot’s. There’s also an argument that Fiat’s share-price upside may be higher too.

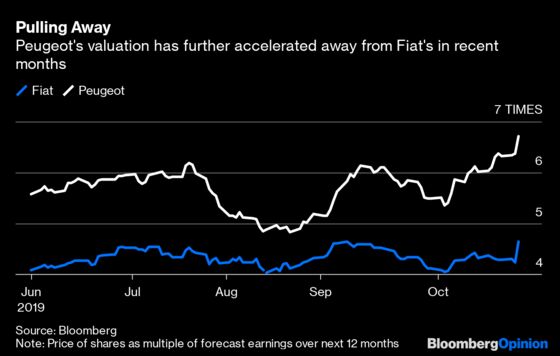

Fiat’s valuation is markedly lower than Peugeot’s on the common profit-multiple measures. That valuation gap, and the difference in the pair’s market values, has widened in recent months as Peugeot stock has rallied. Meanwhile, the average analyst price target on Fiat shares is more than 20% higher than where the shares closed Tuesday. Peugeot shares were pretty much at their target price.

On top of that, there’s the question of who will be running the show. It’s likely Tavares will be the driving force of the combination. This risks looking and feeling like a Peugeot takeover of Fiat.

The remedy for such concerns would be to give Fiat shareholders a bit more than what they appear to put in. There’s a precedent: The proposed merger between Fiat and rival French carmaker Renault SA from May. In those talks, Fiat was the larger partner based on prevailing market capitalizations, and so the plan was for a Fiat special dividend beforehand to bring it closer to a 50:50 deal. But even then, Renault shareholders would have gotten a slight premium. The terms were designed to placate feelings that Renault was chronically undervalued.

Tavares should get the idea. Back then, musing from the sidelines in an internal memo to Peugeot staff, he called the proposed Renault deal a virtual takeover by Fiat. And when a merger becomes a takeover, a premium is paid. Fiat needed to address the concern that it was getting Renault on the cheap. Peugeot may now need to do the same with Fiat.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.