(Bloomberg Opinion) -- At first glance, it looks like dealmaking is booming in the U.S. and dead in Europe. Contrast United Technologies Corp.’s blockbuster tie-up with fellow defense contractor Raytheon Co. and Fiat Chrysler Automobiles NV’s decision to pull out of talks with Renault SA.

The reality is more that transactions are getting harder everywhere as protectionism mixes with trustbusters and awkward shareholders. The minute there is a debate about a takeover, more voices will be screaming “no” than “yes.” In Europe especially, dealmakers are struggling to win the argument.

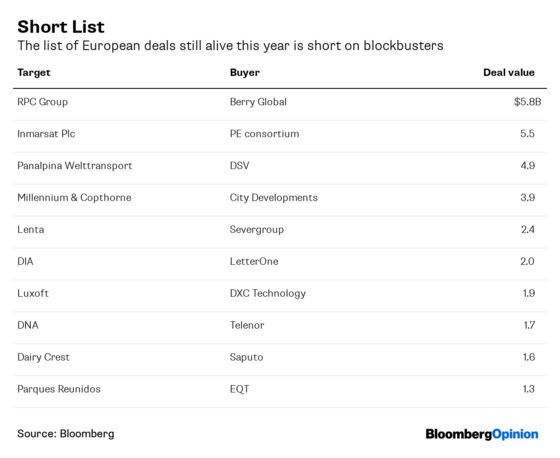

A handful of jumbo takeovers in the U.S. has distorted the picture. The five biggest transactions announced in the U.S. so far this year were valued at about $313 billion. In Europe, the top 10 deals that are still alive are worth only one-tenth of that figure, according to data compiled by Bloomberg.

Consolidation within the U.S. may not be a healthy sign in itself. Why are companies returning to their backyard when their M&A teams had been, until very recently, tapping Europe and Asia for growth? It is possible that U.S. CEOs now perceive too many obstacles in shopping abroad, and with good reason.

Now look at the list of loved and lost in Europe, and see what went wrong.

The usual deal-killing boogeymen are still there, but they appear to be getting even tougher. It wasn’t surprising that trustbusters blocked Siemens AG and Alstom SA’s efforts to merge their giant rail businesses. However, British supermarket J Sainsbury Plc’s purchase of Walmart Inc.’s Asda operation, which was struggling to keep its share of the market, looked a less clear-cut target for regulators.

Protectionism is clearly at work, but so too are broader interventionist forces. All deals are becoming subject to heightened scrutiny; every opposing voice is getting a hearing. If a proposed transaction isn’t sealed as soon as it is announced, the path to agreement and completion is now that much more tortuous.

Fiat-Renault stalled after the French government started dragging its feet, having made supportive noises when the talks became public. In the intervening period, an activist surfaced to complain about the terms. That may have been influential in changing the mood.

Berlin supported Deutsche Bank AG’s talks with Commerzbank AG. But after an initially positive market reaction, growing opposition from labor unions helped to kill the talks.

Even the failure of British subprime lender Non-Standard Finance Plc’s bid for rival Provident Financial Plc fits the pattern: Minority shareholders grumbled about the transaction, giving regulators technical grounds to block it. The Scout24 AG buyout – which would have been the biggest in Europe this year – collapsed because the classified group’s shareholders changed their mind about the price as markets rallied.

Bristol-Myers Squibb Co.’s acquisition of Celgene Corp. had to overcome activist opposition. But it's notable how many of the big U.S. deals were almost fully baked on becoming public. Having a healthy debate about M&A is a good thing. If it stops reckless dealmaking, great; but if it stops the benefits of M&A – removing poor management and tackling overcapacity – then something has gone wrong.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.