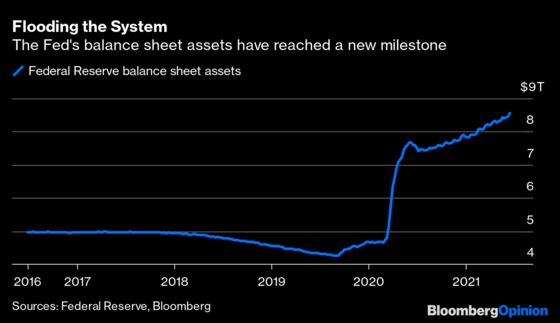

The Most Important Number of the Week Is $8 Trillion

(Bloomberg Opinion) -- Overlooked this week amid all the talk about the Federal Reserve starting the process of eventually paring back on its unprecedented stimulus efforts was the fact that the central bank’s balance sheet assets surpassed $8 trillion for the first time. This milestone should be a reminder that just because the Fed may soon start reducing, or “tapering,” the $120 billion a month it has been pumping into the financial system since the start of the pandemic, it doesn’t mean the forces that have underpinned markets are going away anytime soon — perhaps not for years.

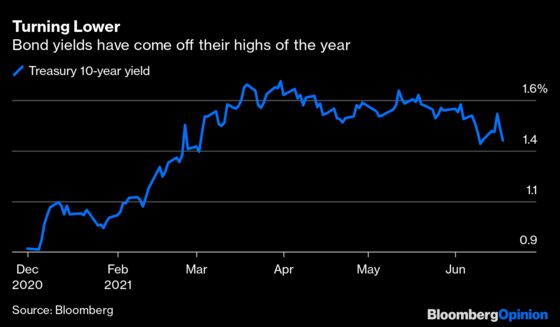

The situation could set the central bank up for a repeat of former Fed Chairman Alan Greenspan’s “conundrum” when the central bank started tightening monetary policy in 2004 only to see long-term bond yields fall, contributing to easier financial conditions and spurring equities higher. We saw a hint of that last week, with the yield on the benchmark 10-year Treasury note dropping to some of its lowest levels since early March.

The first thing to know about the Fed’s taper plans is that it won’t mean all the money the central bank has created will be pulled out of the financial system, or at least not yet. Many strategists would say the central bank’s largesse is the prime reason that riskier assets such as equities have soared not just during the pandemic but since the financial crisis more than a decade ago. Putting a graph of the S&P 500 Index next to one showing the expansion in the Fed’s balance sheet would only strengthen that notion.

The second thing to know is that the central bank has arguably created more cash through its quantitative-easing measures than banks know what to do with. Data compiled by Bloomberg show banks’ surplus liquidity has grown to $6.74 trillion from $3.21 trillion at the end of 2019 and from less than $300 billion before the Fed began using quantitative easing as part of its policy tools in 2009. And just look at the Fed’s reverse repurchase agreement facility. This program allows financial institutions to park excess cash with the central bank. Rarely used in recent years, demand has skyrocketed lately even though the Fed was paying 0% interest on the money deposited. (The rate was bumped to a “juicy” 0.05% this week.)

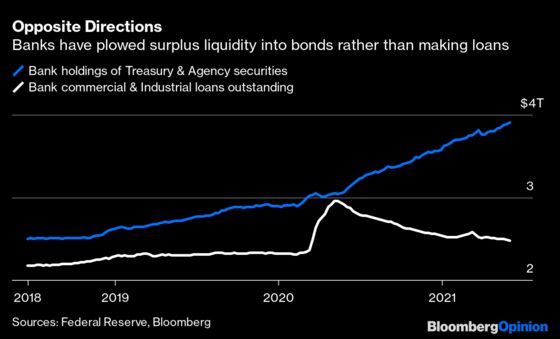

Banks are also recycling a ton of money back into government securities. The growing divergence between bank holdings of Treasuries and related securities and the amount of commercial and industrial loans outstanding is stark, offering further proof that there is too much money sloshing around in the financial system.

The key questions are when will the tapering start and how long will it last? The answer is that tapering will most likely begin either later this year or early 2022, depending on the strength of the economic recovery, and will last perhaps until 2023. An April Federal Reserve Bank of New York survey of market participants and the 24 primary dealers that trade with the central bank found that the taper was expected to last 12 months, according to Morgan Stanley.

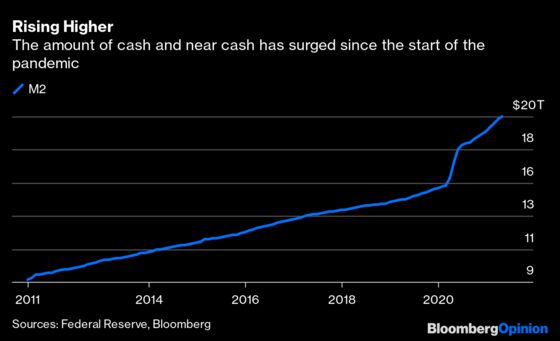

No matter what the Fed does or when it does it, there are forces that should keep the cost of money near record low levels not just in the immediate future, but long past the end of tapering. Such a scenario should limit any rise in bond yields, and that, in turn, should provide a favorable backdrop to equities and other risk assets. That’s what happened from mid-2004 to mid-2006, when the Fed raised interest rates nine times, from 1% to 5.25%; both the S&P 500 and Bloomberg Barclays U.S. Treasury Index managed to generate positive returns in each of those years. And while 2013 was a terrible year for the bond market as the Fed reduced its purchases, resulting in the “taper tantrum,” the S&P 500 actually soared 29.6%. Plus, there is much more excess liquidity in the financial system, as measured by M2 — which is cash, checking deposits, savings deposits, money-market funds and other items defined as “near money.”

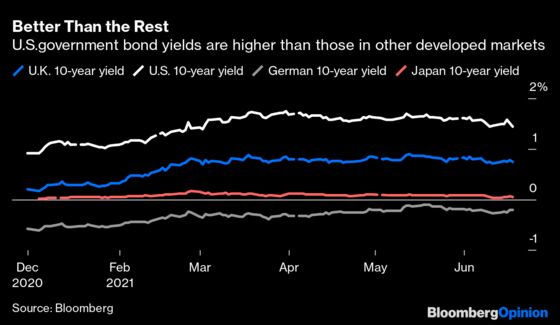

The rates strategists at BMO Capital Markets, regularly ranked as the best in the business in Institutional Investor’s widely followed annual surveys, laid out a number of forces that are keeping yields low in a note to clients Friday. These include the high yields offered on U.S. Treasuries relative to what investors can get on sovereign debt almost anywhere else in developed markets; the persistent global savings glut; aging populations; advances in technology tempering long-term inflation; and the reduction in volatility around interest rates as central banks have become more transparent about their policy intentions. Here’s how they summed it up:

This isn’t to suggest that 10-year yields will never reach a 2-handle again, rather that the prospects for such an eventuality (was) just lowered and will require a longer runway than many in the market might have assumed at the end of Q1 when (yields) touched 1.77%.

To Greenspan, the performance of financial assets as the Fed pulled back the punch bowl was a conundrum. Now, no one should be surprised if the reaction is just the same. The Fed itself has seen to that.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.