It Wouldn't Take Much for the Fed to Cut Rates to Zero

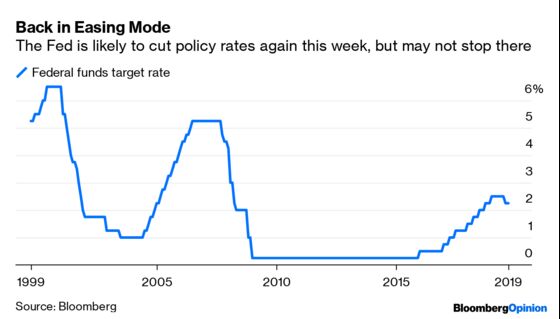

(Bloomberg Opinion) -- The Federal Reserve is set to lower its target for the federal funds rate by another 25 basis points next week while leaving the door open for further reductions. When does this cycle end? When the Fed either stabilizes the economy with something on the order of 75 basis points of rate cuts or the economy slips into recession and rates head back toward zero. There isn’t much room between these two outcomes, though I expect the first to prevail.

While Fed officials such as Chairman Jerome Powell repeat the mantra that the economy is in “a good place,” the risks to the outlook stemming from slower global growth and trade wars remain sufficient to justify rate cuts. As Powell explained again last week, the Fed believes that its dovish pivot toward a lower path for policy rates help explains the economy’s resilience in the face of that uncertainty.

Now that the Fed has shifted policy expectations, it needs to continue to follow through with actual rate cuts starting next week. If it doesn’t, policy makers risk an unwanted tightening of financial conditions that would undermine their efforts to counteract a growing uncertainty about the economic outlook that is not likely to dissipate in the near term. Similarly, the Fed can not cut off the possibility of another rate cut without risking a negative market reaction.

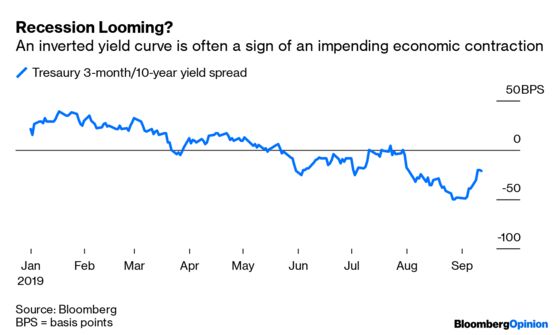

At some point, though, the Fed will say “enough is enough.” If the risks to the economy fail to materialize into a substantial deterioration in the outlook that threatens to send unemployment higher, the Fed will stop loosening monetary policy. It is reasonable to believe that this occurs after three rate cuts of 25 basis points each. That will bring short-term rate to a level that should largely reverse the inversions in key parts of the Treasury market’s yield curve.

Put another way, the yield curve as currently signaling that sustaining the expansion requires another 50 basis points of easing. A total of 75 basis points would be consistent with the other “mid-cycle adjustments” that Powell referred to at the end of the last Fed policy meeting on July 31. What if that isn’t sufficient to stabilize the economy? I suspect that if it looks obvious that the economy needs 100 basis points of easing, it will only be obvious because the job market has slowed enough to push unemployment higher.

And therein lies the risk of much lower policy rates. The unemployment rate hardly ever moves meaningful higher absent a recession. Former Federal Reserve Bank of New York President William Dudley often noted that a 0.3 percentage point to 0.4 percentage point increase in the unemployment rate predicts a recession, a concept quantified by the Sahm-rule.

My concern is that if unemployment looks to be rising enough to justify that next 25 basis points of easing, the economy is almost certainly sliding into recession. And if it is sliding into recession, the most likely scenario is that the Fed will be taking interest rates to zero. In other words, at that point it is an all or nothing situation.

So either the economy stabilizes with a total of up to 75 basis points of easing or rates are going to zero. I am not seeing much room in between these two outcomes, which means sentiment will likely repeatedly flip between these two outcomes. I am optimistic that the Fed moved early enough in this cycle to bring about the first outcome, but we can’t ignore the second.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2019 Bloomberg L.P.