(Bloomberg Opinion) -- From the moment the Federal Reserve announced how it would buy bonds for its $250 billion Secondary Market Corporate Credit Facility, something seemed amiss.

After all, the central bank already had criteria in place for buying individual corporate bonds, separate and distinct from exchange-traded funds. And yet, the Fed this week unveiled an entirely new class of eligible assets, called “Eligible Broad Market Index Bonds.” Why? Within an hour, I speculated that this was little more than a workaround for issuers being forced to certify that they’re in compliance with the Coronavirus Aid, Relief, and Economic Security Act.

It turns out that’s more or less the extent of it. In a report provocatively titled “The $250 Billion Loophole,” Daniel Krieter and Daniel Belton at BMO Capital Markets meticulously broke down the latest information about the Fed’s corporate-credit facility. They also concluded that the certification process was rendering the central bank’s program powerless:

The requirement that businesses have significant U.S. operations and a majority of its employees in the U.S. proved problematic for the Fed since the only way the central bank could realistically adhere to this was by having individual corporations certify their compliance with these prerequisites. Having a large percentage of hundreds of American corporations certify compliance was very difficult from an operational standpoint to begin with, and became even more so when certification potentially became stigmatized after credit spreads rallied so significantly. Without certification, the Fed was potentially left with a huge liquidity facility that wasn't allowed to buy anything but ETFs.

Clearly, that didn’t sit well with Fed Chair Jerome Powell, who told the Senate Banking Committee earlier this week in response to questions about corporate-bond buying that “we feel we need to follow through and do what we say we’re going to do.” In other words, even though investment-grade bond yields are at record lows and every creditworthy firm that wants to borrow money can do so, the central bank still felt it needed to prove to investors that it’s capable of purchasing individual bonds.

So, through an extremely generous reading of the CARES Act, the Fed figured out a way to simply become an investor in everything, as the BMO strategists explain:

Section 4003(c)(3)(c) requires purchases of only companies with “significant operations in and a majority of its employees based in the Untied States” unless the purchases are “securities based on an index or that are based on a diversified pool of securities.” This clause was likely included to allow the Fed to buy ETFs. Instead, the Fed created its own index of corporate bonds, the “Broad Market Index,” and will now purchase individual corporate bonds based on this index under this clause. In one swift stroke, the Fed essentially made the entire universe of non-financial corporate debt under five years immediately eligible for purchase.

This is a brazen move. Just take a moment to re-read the provision in its entirety and keep in mind that each individual corporate bond is, by definition, a “security.”

(C) UNITED STATES BUSINESSES. — A program or facility in which the Secretary makes a loan, loan guarantee, or other investment under subsection (b)(4) shall only purchase obligations or other interests (other than securities that are based on an index or that are based on a diversified pool of securities) from, or make loans or other advances to, businesses that are created or organized in the United States or under the laws of the United States and that have significant operations in and a majority of its employees based in the United States.

I just don’t see how a single bond can be considered “based on an index,” nor “based on a diversified pool of securities.” It’s nothing more than a company’s liability (or “obligations,” per the above wording). ETFs, on the other hand, of course fit that billing: Each fund share is a single security that tracks a specific index or derives its value from many other securities. For instance, LQD tracks the iBoxx USD Liquid Investment Grade Index, while JNK tracks a more liquid component of the Bloomberg Barclays High Yield Total Return Index. Both are based on a wide swath of corporate bonds.

Simply put, the Fed has inverted the CARES Act language. By any typical reading of the legislation, the central bank is granted the authority to buy indexed securities — not to invent its own index and buy individual corporate bonds needed to populate it. If the claim is that each individual bond is “based on an index” just because they’re a part of the custom “Broad Market Index,” then why bother with the exercise in the first place? After all, the Bloomberg Barclays U.S. Corporate Bond 1-5 Year Index already exists, has a $2.12 trillion market value and mostly covers the universe of eligible debt. By the Fed’s logic, each of the 2,242 member securities are therefore “based on an index.”

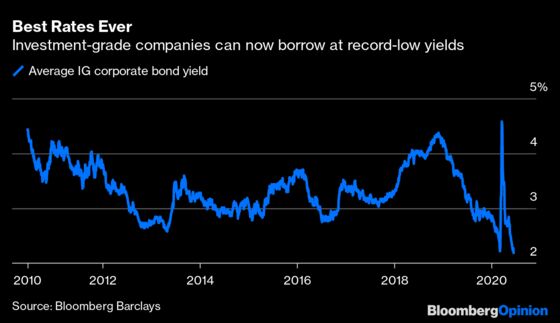

While it may not ultimately be all that much different from buying a basket of ETFs, twisting the rules on the fly casts aside any notion that the central bank was content with serving as a lender of last resort for U.S. companies that couldn’t gain market access. “Yesterday showed that the Fed’s intent is not just to be a backstop, but to be an active participant in driving spreads back to pre-Covid levels,” Steve Kellner, head of corporate bonds at PGIM Fixed Income, told Bloomberg News’s Molly Smith on Tuesday. “This was a game changer.” By day’s end, average investment-grade bond yields tumbled to a new record low, 2.18%.

While Wall Street cheers the move, the Fed’s “loophole” is potentially more sinister for Main Street. Congress granted the central bank authority to buy bonds from companies “that have significant operations in and a majority of its employees based in the United States.” That’s no longer a requirement for “Eligible Broad Market Index Bonds.” Powell has said throughout the coronavirus crisis that his overarching goal is to save American jobs, but this move makes it look as if narrowing credit spreads for large companies is his top priority. It’s hard to interpret this move as anything other than the central bank deciding it’s no longer worth the hassle of making executives certify that they employ a majority of their workforce in America before getting a boost, even though that’s a critical component of the law.

“We’re implementing the law that you passed,” Powell said on Wednesday, in response to questions from Representative Jim Himes, a Connecticut Democrat, about whether the Fed’s credit facilities have terms to prioritize paying workers rather than dividends or debt service. “We don’t think it’s up to us to rewrite the law to achieve goals we might have.”

It’s not clear who would be offended enough (or have the means) to challenge the Fed. Budget watchdogs have been rendered toothless. Jeffrey Gundlach, DoubleLine Capital’s chief investment officer, said in April that the Fed is “acting in blatant non-compliance with the Federal Reserve Act of 1913” but “will make some wonky semantic argument” to justify its actions. That sounds awfully similar to how it’ll get away with skirting CARES Act restrictions.

More broadly, the federal government is distributing $3 trillion of economic rescue funds with little of the intended oversight. Bloomberg News’s Laura Davison reported Wednesday that even though three new oversight bodies are barely functional, about $2 trillion has already been distributed. There’s a balance between getting funds out fast and preventing abuse. Someday, we may know how it all shook out.

Powell has repeatedly praised the speed and size of the government’s relief efforts, which may explain why he was willing to search for shortcuts to start the Fed’s corporate bond purchases. The central bank may yet be a minor player in the market — Powell claimed on Tuesday that “we’re not actually increasing the dollar volume of things we’re buying, we’re just shifting away from ETFs.” Consider me skeptical. At the very least, the Fed has carved out a path to maximizing the facility’s $250 billion of buying power. The Fed would have likely tapped out at $50 billion with ETFs alone.

In the end, it almost certainly won’t matter that the Fed warped its power. For traders, that’s arguably the most important lesson in all of this: When the central bank puts its mind to something, don’t expect anything to stand in its way. Perhaps not even the law.

The passage in question is on page 193.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.