Powell Admits Fed Has No Playbook for a Trump Trade War

The Fed chair calls the policy unprecedented, and the president wastes no time in proving him right.

(Bloomberg Opinion) -- Federal Reserve Chair Jerome Powell doesn’t like how President Donald Trump’s trade war is impacting the U.S. economy. To make matters worse, the central bank has no playbook for how to deal with the current situation, he said in prepared remarks at the Kansas City Fed’s Economic Policy Symposium in Jackson Hole, Wyoming.

He had no idea the starkest example would come about an hour after he delivered his speech when Trump announced he would have an afternoon response to China’s threat to impose additional tariffs on $75 billion of American goods. The stock market, which had been up after Powell spoke, immediately reversed course and was down 1.7% just before noon.

So he and other Fed officials have to draw up their own plan of attack. His suggestion? More interest-rate cuts.

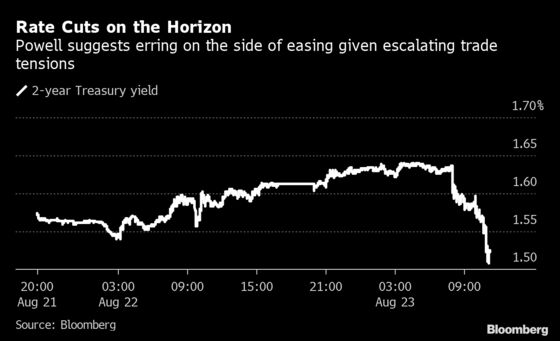

Noticeably missing from his remarks was the phrase “mid-cycle adjustment,” which he and other officials used last month to describe their potentially one-off rate reduction. Instead, he chose to emphasize that the Fed would “act as appropriate to sustain the expansion.” Bond traders read between the lines to take that as openness to as many cuts as the data justifies. Two-year Treasury yields fell about 9 basis points, reversing Thursday’s move after a flurry of regional Fed presidents sounded hawkish and gave Powell cover to push back on market expectations.

What can’t go ignored is that Powell’s speech came amid heavy fire from Trump, who has criticized the central bank for not lowering interest rates faster and sooner. The president, of course, has long been fixated on the Fed, clearly viewing it as an easy scapegoat for any economic weakness. But his derision was especially apparent this week:

- On Monday, he tweeted about “the horrendous lack of vision by Jay Powell and the Fed” and said officials should cut rates by 100 basis points.

- On Wednesday, he lamented that “the only problem we have is Jay Powell and the Fed. He’s like a golfer who can’t putt.” He again called for a “BIG CUT,” and then asked “WHERE IS THE FEDERAL RESERVE?”

- On Thursday, after seeing Germany issue negative-yielding 30-year bonds, he complained that “our Federal Reserve does not allow us to do what we must do. They put us at a disadvantage against our competition.”

- On Friday, just about an hour before Powell was scheduled to speak, Trump flipped to encouragement: “Now the Fed can show their stuff!” he tweeted.

The symposium’s theme in 2019 is “Challenges for Monetary Policy,” though the organizers probably didn’t think the U.S. president’s Twitter feed would be such a glaring obstacle. Trump wasted little time analyzing Powell’s remarks:

Then he couldn’t resist a potshot, comparing the Fed chief with President Xi Jinping of China.

Powell did somewhat push back against Trump, in a telling passage about how much he and other policy makers are struggling to get their hands around his trade policy. Remember the context here — the Fed cut interest rates for the first time in more than a decade on July 31, and a day later, Trump announced additional tariffs on Chinese goods and sent markets into a tizzy. He wasted even less time on Friday, declaring on Twitter “I will be responding to China’s Tariffs this afternoon.” Here’s the central bank’s thinking about trade in its entirety:

“We have much experience in addressing typical macroeconomic developments under this framework. But fitting trade policy uncertainty into this framework is a new challenge. Setting trade policy is the business of Congress and the Administration, not that of the Fed. Our assignment is to use monetary policy to foster our statutory goals. In principle, anything that affects the outlook for employment and inflation could also affect the appropriate stance of monetary policy, and that could include uncertainty about trade policy. There are, however, no recent precedents to guide any policy response to the current situation. Moreover, while monetary policy is a powerful tool that works to support consumer spending, business investment, and public confidence, it cannot provide a settled rulebook for international trade. We can, however, try to look through what may be passing events, focus on how trade developments are affecting the outlook, and adjust policy to promote our objectives.”

All told, though, it comes off as rather meek, and an implicit acknowledgment that the central bank will err on the side of easing as long as trade tensions remain heated. “It will at times be appropriate for us to tilt policy one way or the other because of prominent risks,” Powell said.

Further interest-rate cuts are not a consensus view. Regional Fed presidents including Boston’s Eric Rosengren, Kansas City’s Esther George, Philadelphia’s Patrick Harker, Dallas’s Robert Kaplan and Cleveland’s Loretta Mester all expressed stronger reluctance to further easy monetary policy, given their respective views of the U.S. economy.

Powell is going to have to bridge the divide between that contingent and those who side more with St. Louis Fed President James Bullard. He said on Friday that he expects a “robust debate” on a half-point rate cut among the Federal Open Market Committee voters, adding that “our job is to get the yield curve uninverted.”

At least for today, it’s mission accomplished. The yield curve from two to 10 years, which closed with a negative spread on Thursday for the first time since 2007, is back to positive as short-term yields fell the most on renewed expectations for persistent Fed easing.

Ahead of Powell’s remarks, Kaplan commented that he was open to cutting interest rates, but he’d prefer not to. I’d wager that’s Powell’s line of thinking as well. But clearly, he feels the Trump administration’s policies have boxed him in. The path forward, as long as the U.S.-China trade war wages on, appears to be ever-lower interest rates.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.