(Bloomberg Opinion) -- The old saying in markets that stocks are not the economy has never been more true. It’s not even August and the S&P 500 Index has already surged some 20% this year despite an economy tracking at its lowest rate since 2016 and earnings growth that has come to a standstill. But that doesn’t mean equities are fully disconnected from reality.

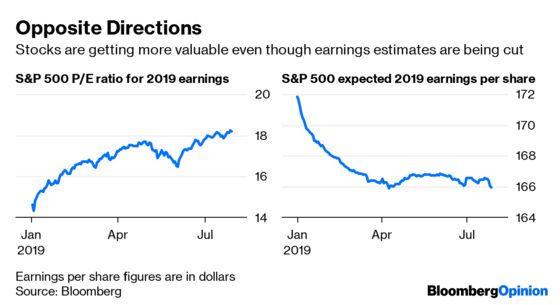

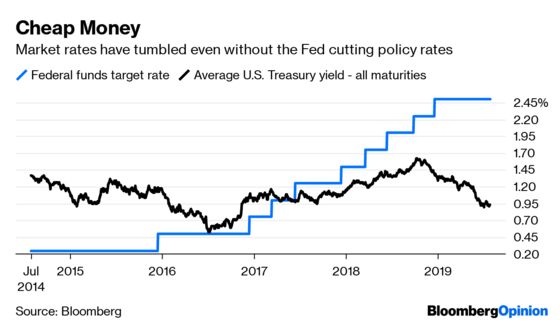

This year’s rally — during which the S&P 500’s estimated price-to-earnings multiple for 2019 has expanded to 18.1 from 14.6 at the start of January — can be credited to the Federal Reserve’s dovish pivot, which has sparked large declines in market interest rates. Simple discounted cash flow analysis shows how lower rates make future earnings more valuable now, justifying higher multiples for equities even though profits are flat from a year earlier and forecasts have come way down.

All this has come without the Fed actually lowering rates. That’s why the monetary policy meeting that concludes Wednesday is so critical for the stock market. Policy makers are widely expected to cut their target for the federal funds rate by a quarter of a percentage point to a range of 2% to 2.25% from 2.25% to 2.50%. But if they decline to signal that more rate cuts are in the cards, market rates will rise and investors will find it harder to justify these relatively lofty equity valuations.

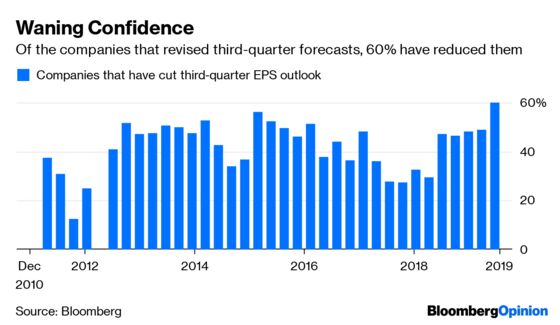

Consider earnings, which are going nowhere. Aggregate net income for members of the S&P 500 is expected to be little changed this year at about $166 a share. What’s worrisome is that most anticipated a big rebound in earnings in the fourth quarter, but that’s becoming more unlikely. Bloomberg News points out that before the bulk of the earnings season began last week, analysts were calling for profits among S&P 500 companies to rise 6.5% in the last three months of the year. Now projections stand at 5.2%, Bloomberg Intelligence data show.

“In a declining interest rate environment, flat earnings are good enough to keep stocks moving higher,” DataTrek Research co-founder Nicholas Colas wrote in a research note to clients. “Yes, it would be nice if we didn’t need to rely on global central banks to see rising stock prices. But this is the world we have.”

There is another reason low rates are critical for stocks, and it has to do with buybacks. Cheap money has allowed companies to issue debt and use the proceeds to buy back their stock, which has helped support earnings per share. In April, the strategists at Goldman Sachs Group Inc. led by David Kostin calculated that net buybacks have averaged $420 billion annually since 2010. “In a world without buybacks, forward EPS growth could be trimmed” 2.5 percentage points, a reduction that has historically corresponded to a 1 point decline in forward price-earnings multiples, the strategists wrote in a report.

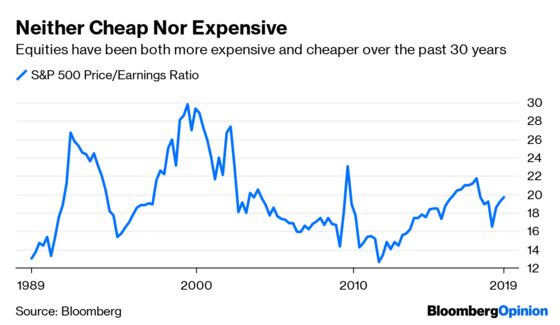

It’s not all bad news for stock bulls. The price-to-earnings ratio for the S&P 500 over the trailing 12 months is only slightly above average compared with the last 30 years, and when adjusted for bond yields is now lower than two-thirds of the time since 1960, according to Jim Paulsen, Leuthold Group Inc.’s chief investment strategist.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.