(Bloomberg Opinion) -- When the Federal Reserve first lowered interest rates in July and then a few weeks ago, it was hard not to think that perhaps the central bank was bowing to pressure from the White House. Although there were signs that the economy was slowing, there were few true red flags that suggested the wheels were falling off the cart.

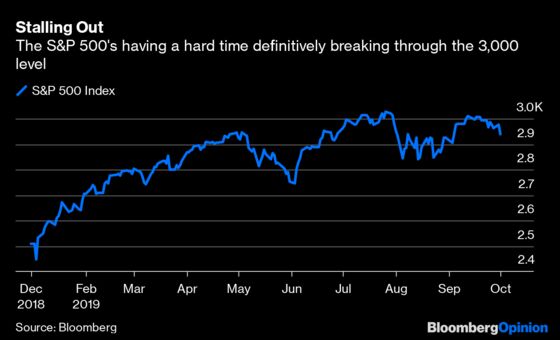

That all changed Tuesday with the release of the Institute for Supply Management’s manufacturing index, which fell to its lowest in 10 years, moving deeper into the zone that signals output is contracting. But that’s not all the Fed needs to worry about. U.S. stocks fell the most in more than five weeks as measured by the MSCI USA Index. The gauge’s 1.24% drop far was triple the 0.31% decline in MSCI’s measure of equities outside the U.S. That’s concerning because it happened even as the bond market stepped up its bets on future rate cuts. This means investors may be starting to doubt that easier monetary policy from the Fed will be enough to spark the economy, especially if the U.S.-China trade war continues to drag on, which looks increasingly likely. “There is no end in sight to this slowdown,” Torsten Slok, the chief economist at Deutsche Bank AG, wrote in a research note. “The recession risk is real.”

In other words, the central bank “put” may be a thing of the past. The longer the data in the U.S. and elsewhere in major economies around the world continue to disappoint, the more investors will perceive policy makers as doing little more than pushing on a string by lowering rates that are already near or at record lows.

BOND TRADERS IGNORE HISTORY

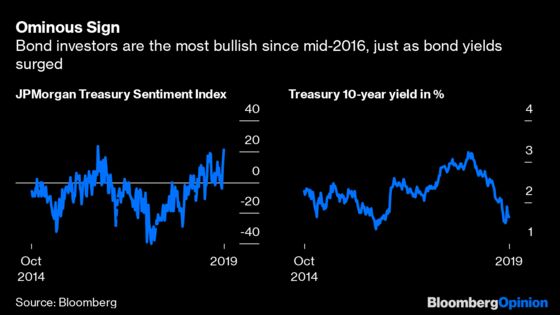

In the eyes of the bond market, the ISM report obliterates the narrative that took hold early last month that perhaps the economy wasn’t as bad as first thought. The yield on the benchmark 10-year Treasury note fell to 1.55% on Tuesday, the lowest since Sept. 6 and down from last month’s high of 1.80% on Sept. 13. The probability of two more Fed rate cuts this year jumped from 20% to about 35%, according to data compiled by Bloomberg. And traders are set up for even more declines in yields, judging by JPMorgan Chase & Co.’s widely followed weekly survey released on Tuesday. The firm’s sentiment index jumped to 21, the highest reading since June 2016. The bad news is that mid-2016 marked the absolute bottom for yields, which started a steady increase from 1.36% to 2.66% that December. The Bloomberg Barclays U.S. Treasury Index dropped 4.11% in the second half of that year. Of course, Donald Trump’s election victory had a lot to do with the decline as investors anticipated his policies would stimulate the economy by cutting taxes. That just shows it pays to keep an eye on sentiment, which can act as a contrarian indicator at extreme levels.

TRUMP IS HALF RIGHT ON THE DOLLAR

Trump took another swipe at the Fed on Tuesday after the disappointing ISM data, calling policy makers “pathetic” for not cutting rates deeper than they have already. If rates were lower, the dollar would be much weaker and manufacturers would be better able to compete on the global stage, Trump explained in a tweet. In some ways, Trump is right. The relative levels of interest rates tend to have an influence on currencies. Economies where rates are higher tend to attract international capital, bolstering their currencies. And right now, no major economy in the world has a policy rate that’s higher than the one overseen by the Fed, which helps explain why the Bloomberg Dollar Spot Index has gained 3.20% from its low this year in late January and more than 9% since February 2018. But interest rates are only part of the equation. Money flows where economic growth is most attractive, and despite the signs of a recent slowdown, the U.S. is still a lure. The OECD said last week that it expects the U.S. economy to expand 2%, more than any other developed economy except Australia’s, which is expected to grow by the same amount.

EMERGING-MARKET FLOWS RETURN

Last month was the best for emerging-market equities and currencies since June. The MSCI Emerging Markets Index of stocks jumped 1.69% while a sister gauge tracking foreign-exchange rates rose 0.79% in September. The Institute of International Finance in Washington figures that emerging markets attracted $37.7 billion of net inflows last month, marking a big turnaround from the $13.9 billion that flowed out in August. The money flowing into emerging markets as well as the rally in their stocks throws some cold water on the notion that these economies should perform poorly when the greenback is rising. The thinking is that the stronger the greenback gets, the harder it will be for emerging-market borrowers to repay the trillions of dollar-denominated debt taken out in recent years. But what many fail to realize is that emerging-market economies on the whole are in a much better fiscal state than ever before. The foreign-exchange reserves for the 12 largest emerging-market economies excluding China just reached a milestone by surpassing $3.25 trillion for the first time. That’s up from less than $2 trillion in 2009.

SOMETHING HAS TO GIVE

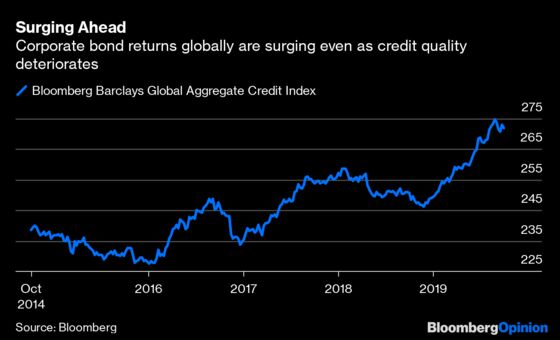

The good news is that companies in the U.S. and globally sold a record amount of bonds in September, issuing $308 billion of debt securities. It was the first time sales topped the $300 billion mark in any month, according to Bloomberg News’s Finbarr Flynn and Hannah Benjamin. This shows that despite worries about the strength of the economy, there are no signs of an emerging credit crunch that would do real damage. The bad news is that credit quality is deteriorating, with the third quarter experiencing the most ratings downgrades for companies relative to upgrades since 2015 in the U.S. alone, according to S&P Global Ratings data compiled by Bloomberg. The firm upgraded 64 issuers and downgraded 164 for an upgrade-to-downgrade ratio of 0.39. The majority of the cuts, or 143, were suffered by speculative-grade borrowers, which had just 33 upgrades. It’s been a banner year for corporate bond issuers and investors, with the Bloomberg Barclays Global Aggregate Credit Index gaining 8.99%. That makes 2019 already the best year for returns since the index rose 10.8% in 2012. Average yields have tumbled to 2.11% from last year’s high of 3.33% in November. But as the actions by S&P show, the high returns have little to do with confidence in credit and more to do with the grab for anything with some sort of yield in a world with some $14 trillion of debt securities carrying yields of less than zero.

TEA LEAVES

Many economists played down the surprise drop in the ISM index by noting how manufacturing is a relatively small part of the economy. The implication is that the slowdown probably isn’t doing much to the jobs picture, which is driven by the much larger services sector. Markets will find out over the next few days whether that’s true as a slew of reports on the job market are released. First up will be the ADP Research Institute’s monthly jobs report for September. The median estimate of economists surveyed by Bloomberg is for a drop to 140,000 jobs created from a better-than-expected 195,000 in August. That would put it closer to the low end of the range over the past five years than the average of 200,000. Then on Friday, the Labor Department is forecast to say that 147,000 jobs were created in September, compared with 130,000 in July. This won’t raise the imminent recession alarms, but it’s also not going to cause anyone to pop the champagne corks.

DON’T MISS

Global Bonds Sell Off for All the Right Reasons: Robert Burgess

Low Rates Are No Reason to Pay Up for Stocks: A. Gary Shilling

Passive Investing Hasn’t Taken Over the World: Barry Ritholtz

Trump’s Impeachment Is Already Hurting the Economy: Karl Smith

Elliott’s Marathon Fight Spells Trouble for MLPs: Liam Denning

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.