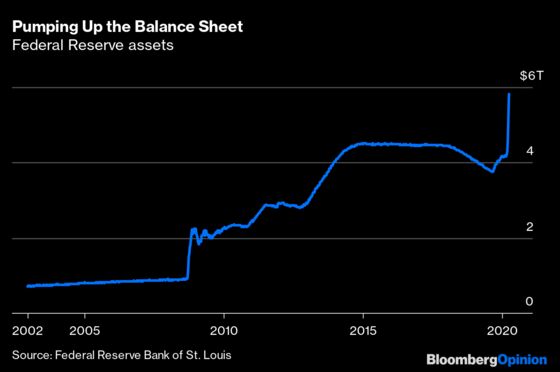

(Bloomberg Opinion) -- The Federal Reserve seems determined to do whatever it takes to help protect the U.S. economy from being devastated by coronavirus-related shutdowns. It’s buying so many bonds that its balance sheet is approaching $6 trillion:

Traditionally in recessions, the Fed buys increasing amounts of government bonds, which reduces interest rates. That usually lowers borrowing rates for businesses as well, helping them ride out an economic storm. But in a situation like the present one, that’s unlikely to be enough. Because shutdowns and the danger of disease are threatening many businesses with bankruptcy, they’ll have pay interest rates that reflect the rising risk of default, making it costly and hard for them to borrow in private markets even with Treasury rates at or near zero.

If companies are unable to roll over their debts, many will go bust, throwing more people into the overloaded unemployment insurance system. Furthermore, banks that lend money to companies and hold corporate debt will also be put in danger. That could cause a financial crisis whose impact long outlasts the shutdowns, turning a one- or two-year recession into a lost decade.

The Fed thus needs to buy lots of corporate debt as well to keep corporate borrowing rates low. It has started doing this via a series of new facilities. These include the Commercial Paper Funding Facility, which buys short-term corporate debt; the Primary Market Corporate Credit Facility, which lends money directly to companies by buying newly issued bonds; the Secondary Market Corporate Credit Facility, which buys up existing corporate bonds in the market; and, in a few weeks, the Main Street Business Lending Program, which will lend money to small and medium-sized companies.

These programs required some creative legal maneuvering. Because the Fed, unlike some other central banks, is only technically allowed to buy government bonds, these lending facilities will actually be separate entities funded by the Fed -- basically, like shadow banking, but for the central bank.

But it’s worth it. There’s no reason to punish companies for failing to see a history-changing, once-in-a-century pandemic, or anticipate the shutdowns that would result. A wave of corporate bankruptcies won't free up resources for more productive activities as in normal times; thus, it wouldn't make the economy more efficient or healthy in any way. Nor would a wave of bank failures. U.S. businesses are, for the most part, perfectly viable under normal conditions. The goal should be to get them back to their previous state as fast as possible after the shutdowns are over, and these Fed lending programs help accomplish that goal.

But as Benn Steil and Benjamin Della of the Council on Foreign Relations have pointed out, the Fed’s programs are so far aimed at either investment-grade corporate debt or small businesses. This leaves out one major category of corporate debt: high-yield bonds, also known as junk bonds. That category might also now include collateralized loan obligations, which are bonds backed by risky loans.

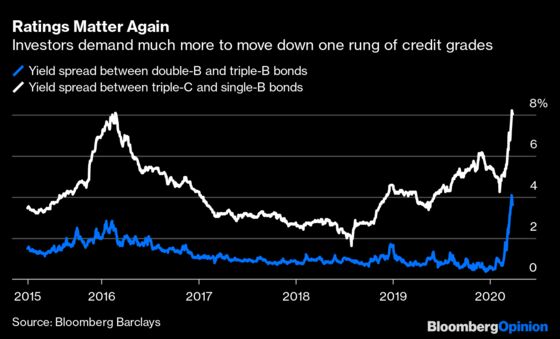

During the past few years, corporations have been taking out ever-more risky leveraged loans, often without the covenant protections that used to accompany such loans. Those loans were looking a bit shaky even before the crisis, as was the junk bond market. Now, credit-ratings downgrades threaten to cut off the flow of lending to these borrowers. That will leave companies that recently relied on risky debt in danger of default, as risk spreads rise:

That will in turn threaten the balance sheets of banks and other financial institutions that hold this debt and have lending relationships with these companies.

To stop this wave of defaults, the Fed could use the new facilities to buy junk bonds, CLO, and other risky corporate debt. This will certainly cause a political outcry. Many people were warning that corporations were borrowing too much and taking on too much risk even before coronavirus. Having the Fed extend those risk-takers a lifeline will be rightfully seen as a reward for bad behavior.

This will make risky debt purchases politically unpopular and difficult. Some, such as my Bloomberg Opinion colleague Brian Chappatta, will worry about encouragement of excessive risk-taking in the future. Others will see it as one more sign of a rigged capitalist system, where gains for rich people are privatized and losses are socialized.

But nevertheless, the U.S. can ill afford a wave of corporate bankruptcies at this time. Like it or not, risky corporate debt must be bailed out. One potential solution is to make junk-bond and leveraged-loan purchases conditional on companies keeping workers on their payroll. That might take more creative legal maneuvering or even new congressional action. But at least it would help distribute the bailouts in a more egalitarian fashion.

A pandemic like this presents the U.S. with no good options. The danger of bailing out irresponsible companies is much less than the lasting danger from a wave of bankruptcies and mass unemployment.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2020 Bloomberg L.P.