Jerome Powell Refuses to Humor Bond Traders’ Tantrums

(Bloomberg Opinion) -- The $21 trillion U.S. Treasury market already set the narrative ahead of the Federal Reserve’s decision on Wednesday. Benchmark 10-year yields stormed to the highest level since January 2020, while 30-year yields reached 2.44% for the first time since August 2019. Bond traders were throwing yet another tantrum as if to dare Fed Chair Jerome Powell and his colleagues to stop them.

Instead, Fed officials stayed true to their new framework. Yes, economic growth will likely be robust this year, and inflation will probably average 2% over the coming years. But until they see proof, they’re not going to be in any hurry to start penciling in interest-rate increases.

The Federal Open Market Committee, as expected, left the fed funds rate unchanged in a range of 0% to 0.25% and didn’t fiddle with its asset purchases after its two-day meeting. Fed officials for the first time since December updated their economic projections, which showed expectations for economic growth of 6.5% this year and core inflation of 2.2% in 2021, 2% in 2022 and 2.1% in 2023. The unemployment rate will probably fall to 4.5% this year, then 3.9% in 2022 and finally 3.5% in 2023, which would match the generational low set in late 2019 and early 2020.

Still, that wasn’t enough to move the median forecast among Fed officials on the much-scrutinized “dot plot,” which still shows an expectation to keep the central bank’s benchmark rate near zero through 2023. That’s not to say some policy makers weren’t swayed by two rounds of fiscal aid and widespread vaccinations: Seven of them now predict raising rates in 2023, up from just five in December, while four of them see rate increases beginning in 2022, rather than just one.

To be clear, if central bankers’ economic forecasts come to pass, the dots are bound to move higher. “The strong bulk of the committee is not showing a rate increase during the forecast period,” Powell said. “Part of that is wanting to see actual data rather than just a forecast at this point. We do expect that we’ll begin to make faster progress on both labor markets and inflation as the year goes on because of progress with the vaccines, because of the fiscal support that we’re getting. We expect that to happen, but we’ll have to see it first.”

Bond traders aren’t quite as patient. The reason Treasury yields have increased so much, of course, is because investors are starting to worry about a pickup in inflation. Longtime bond-fund manager Bill Gross was back in the headlines on Tuesday, saying that he’s betting against long-term Treasuries and sees inflation reaching 3% or 4% in the coming months. Greg Jensen, co-chief investment officer of Bridgewater Associates, said this week that “the pricing-in of inflation in markets is actually the beginning of a major secular change, not an overreaction to what’s going on.”

What bond traders don’t seem to quite understand is that this is exactly what the Fed wants to see. In fact, when Powell debuted the central bank’s new average inflation targeting framework in August, he specifically bemoaned how difficult it is to raise the nation’s collective expectations for future price growth after years of falling short of 2%. Well, according to Jim Reid at Deutsche Bank, more people in the U.S. are now searching Google News for “inflation” than at any time since records began in 2008. As it so happens, the five-year U.S. breakeven rate also reached a 2008 high on Tuesday.

Now comes the trickier part: Actually observing inflation above 2% for a sustained period of time. Fed Vice Chair Richard Clarida has suggested inflation would have to average 2% for a full year before raising interest rates, a hurdle which has almost never been met since the 2008 financial crisis when using the central bank’s preferred gauge. Fed officials have made clear that they expect to see outsized figures in the coming months and that those won’t cause them to change course. “I would note that a transitory rise in inflation above 2%, as seems likely to occur this year, would not meet this standard,” Powell said.

Powell was pressed on what was missing from the Fed’s economic projections to hold off on forecasting an interest-rate increase in 2023. After all, core inflation in each year through 2023 is expected to be at least 2%. “The state of the economy in two or three years is highly uncertain, and I wouldn’t want to focus on the exact timing of a rate increase that far into the future,” he said. “The fundamental change in our framework is that we’re not going to act preemptively based on forecasts, for the most part, and we’re going to wait to see actual data. I think it will take people time to adjust to that, and the only way we can really build the credibility of that is by doing that.”

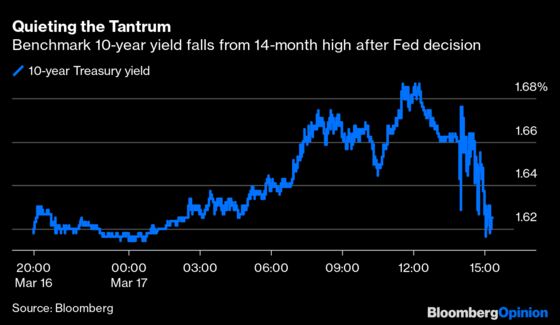

Treasuries seemed to be grappling with this reality in the wake of the decision, with 10-year yield yields fluctuating between as high as 1.68% and as low as 1.62%. It’s also worth noting that the Fed didn’t make any announcement about whether it will extend a measure that allows banks to exclude Treasuries and reserves from their supplementary leverage ratios, with Powell saying only that there will be a decision “in coming days.” In an effort to alleviate pressure on short-term rates, which have been bumping up against zero, the central bank did boost the daily counterparty limit in reverse repo operations to $80 billion from $30 billion, the first increase since 2014. But it didn’t increase its interest rate on excess reserves, which some strategists thought was a possible solution.

Bond traders may yet push longer-term Treasury yields higher in the coming days. But the initial market reaction at least suggests investors are coming to terms with the fact that the Fed isn’t going to be rushed into anything by a few loud tantrums.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.