The Fed Needs to Do More Than Just Head Off a Recession

(Bloomberg Opinion) -- The Federal Reserve is widely expected to reduce interest rates when it meets this afternoon. Chairman Jerome Powell has been explicit that the U.S. economy is “in a good place,” and undoubtedly sees three cuts in one year (the Fed cut rates in August and September) as sufficient insurance against a recession.

But avoiding recession is too low of a bar. The Fed made a major mistake by prematurely raising rates in 2018, and it shouldn’t risk compounding that mistake by prematurely ending its efforts to lower them now. The Fed’s dual mandate is to achieve maximum employment and stable prices. There is little to indicate that the U.S. is at full employment, and market-based measures of inflation expectations are falling.

Rather than making just one more rate cut, the Fed should continue lowering rates to ensure that inflation rises above its 2% target — and stays there for two or three quarters.

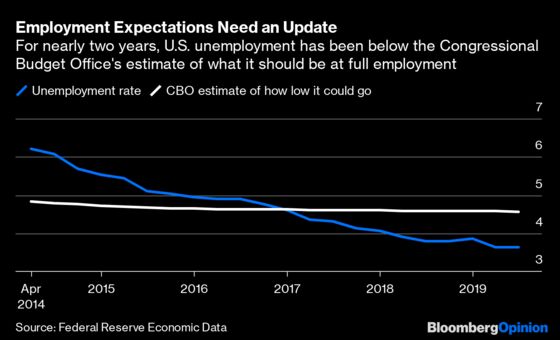

The first reason for the Fed to be aggressive is because it has repeatedly underestimated how much job growth the economy could sustain. In 2016 The Fed began raising rates because it believed that the unemployment rate (then 4.8%) was about as low is it could get without sparking inflation. Since then, the unemployment rate has fallen to 3.5%, while inflation has remained below 2%.

How many jobs did the Fed’s mistake cost? About 500,000 by August 2018, according to one estimate. And while the job market is the best it has been in years, there are still millions of discouraged workers who are underemployed or detached from the labor market. Settling for slower job growth risks leaving them on the sidelines.

Besides, the Fed has long argued that its 2% inflation target is “symmetric” — meaning that inflation should be above 2% as often as it is below it. Yet inflation has been below 2% for all but a dozen months in the last decade. Unless the Fed is able to generate sustained inflation above 2%, it will lose credibility.

Meanwhile, market measures of future inflation continue to fall. If the Fed fails to arrest the decline, then it risks exposing the U.S. economy to deflation when the next downturn hits. Deflation is especially dangerous for an economy in recession, because when prices are falling, businesses have little extra revenue to hire new workers or raise wages. This can send the economy into a spiral of stagnation.

Powell is correct that the U.S. economy is healthier than those of other developed countries. And he undoubtedly wants to prevent the U.S. slowdown in investment and manufacturing from becoming a full-blown recession.

But there are other dangers facing the U.S. economy. There is little reason to believe that the U.S. is at full employment or that inflation will reach (much less exceed) 2% anytime soon. The Fed’s focus should be on fulfilling its mandate.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a former assistant professor of economics at the University of North Carolina's school of government and founder of the blog Modeled Behavior.

©2019 Bloomberg L.P.