Fed Has No Choice But to Tackle Both Repo and Recession

(Bloomberg Opinion) -- Heading into October, it was clear Federal Reserve officials would face a difficult decision at their meeting at the end of the month. Just one day into October, the challenges have already become even more intense.

Analysts have been expecting that Fed policy makers would probably announce a plan on Oct. 30, after their two-day meeting, to expand the size of the central bank’s balance sheet. The questions would simply have been by how much and whether Chair Jerome Powell could stress that the move wasn’t a return to post-crisis quantitative easing but rather was “organic” growth in line with Fed tradition. It would have been a tough tightrope act to begin with, particularly given Powell’s tendency to speak off the cuff and the fact that he played down the repo market’s mayhem after the Fed’s most recent decision.

But that act just got tougher because it looks as if the Fed will have to deal with recession fears on top of repo strains.

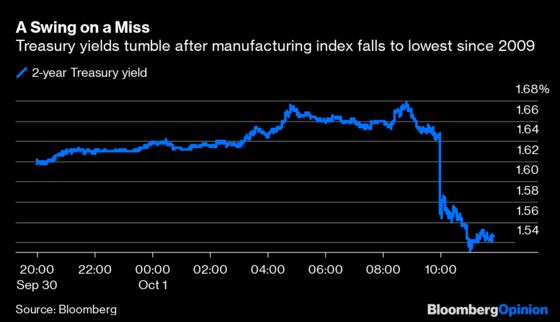

The Institute for Supply Management’s factory index, which measures U.S. manufacturing, dropped to 47.8 in September, the lowest since June 2009. That missed every estimate in a Bloomberg survey and is at a level that indicates contraction. It goes without saying that drawing comparisons to the last month of the previous recession is not a good sign for the health of the economy.

“There is no end in sight to this slowdown; the recession risk is real,” said Torsten Slok, chief economist at Deutsche Bank. “The sharp retreat we are seeing on manufacturing confidence is exactly what a recession looks like,” noted Chris Rupkey at MUFG Union Bank. “Manufacturing weakness is close to dangerous levels,” said FTN Financial’s Christopher Low.

President Donald Trump, for his part, didn’t take long to notice:

Bond traders also reacted quickly. It takes particularly weak data for 10-year Treasury yields to drop six basis points instantly and for two-year yields to tumble eight basis points in a flash. But that’s what happened on Tuesday after the ISM report. Moreover, fed funds futures rushed to price in another quarter-point interest-rate cut from the Fed at the end of this month. The implied odds, which were just 58% on Monday, jumped to 78%. As much as policy makers say they aren’t influenced by the bond market, they’re unlikely to go against traders if conviction remains that high.

The central bank already faces something of a credibility problem for not anticipating the strains in the repo market. Now it looks as if the Fed will have to drop its benchmark rate again, just a month after policy makers’ median projection called for no more rate cuts through 2020. To reiterate: The median on the “dot plot” not only implied that interest rates would stay where they are this year but that they would be unlikely to move next year, either. That’s not to say that forecasts can’t change, but it calls into question the usefulness of the Fed’s forward projections if they wind up having little to no bearing on what actually happens.

The Fed doesn’t want to be seen as reactive. That’s one reason for the past two “insurance cuts,” after all, and why Powell has repeatedly emphasized that his main goal is to take appropriate action to sustain the expansion. It would be one thing if he could just use his next news conference to explain away the stress in the repo market by saying policy makers have found the appropriate level of reserves necessary to control short-term rates. But should economic data continue to miss estimates, the central bank would face a two-front war on its credibility that would be difficult to win.

To be sure, the ISM report could be an outlier — Citigroup Inc.’s U.S. Economic Surprise Index is still close to the highest in more than a year. And as Thomas Simons at Jefferies LLC pointed out: “Manufacturing itself is in a recession, but it does not mean that the overall economy is in a recession.” It only makes up 10% to 15% of the economy, he said, and the U.S.-China trade war, which “could theoretically be resolved at any time,” has been a key reason for the slump.

Powell has admitted that the central bank has no playbook for dealing with a prolonged trade war. So far, his answer has been to drop interest rates time and again. This time might be trickier: He might have to both announce another cut and reveal that the Fed will increase the size of its balance sheet just a few months after shrinking it — and avoid spooking markets at the same time.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.