Fed Gently Nudges Muni Market and Deadlocked Congress

(Bloomberg Opinion) -- The Federal Reserve’s actions speak louder than its words. Chair Jerome Powell and his colleagues have sent their first shot across the bow of Senate Majority Leader Mitch McConnell, House Speaker Nancy Pelosi and other negotiators who have failed to reconcile their differences in providing aid to strapped state and local governments.

On its face, the Fed’s announcement last week that it would reduce borrowing costs by 50 basis points in its Municipal Liquidity Facility didn’t make much of a splash. Partly that’s because the yield spreads remain far too wide for all but the most troubled issuers. Illinois is the only state that has taken out a loan since the program was announced in April, and New York’s Metropolitan Transportation Authority is the only other borrower that has shown any interest in tapping the central bank. It didn’t help that the updated term sheet was published after U.S. markets closed and less than an hour after Democratic presidential nominee Joe Biden revealed Senator Kamala Harris as his running mate.

Still, what the Fed has made clear during the coronavirus crisis is that it prefers to jawbone the markets it has never backstopped before, like corporate debt and municipal bonds, rather than rushing in with a heavy hand, as it does with U.S. Treasuries and mortgage-backed securities. By and large, that strategy has worked seamlessly: Both investment-grade and junk-rated companies are locking in record-low borrowing costs while interest rates on tax-exempt munis are once again below benchmark Treasury yields, giving states and cities more affordable access to cash.

If that’s the case, then why did the Fed bother to cut interest rates in its municipal-bond facility? It’s most likely because policy makers realized their attempts to jawbone congressional leadership into action have failed.

By my count, here are the central bankers who have implored Congress for fiscal support since the Fed’s last meeting on July 29: Powell, Fed Vice Chair Richard Clarida, Minneapolis Fed President Neel Kashkari, Chicago Fed President Charles Evans, San Francisco Fed President Mary Daly, Cleveland Fed President Loretta Mester, Richmond Fed President Thomas Barkin, Boston Fed President Eric Rosengren, Dallas Fed President Robert Kaplan and Atlanta Fed President Raphael Bostic. Some, including Barkin, Evans and Kaplan, specifically cited the need to send aid to states and cities.

“As you look at the economic outlook there are some negative scenarios, and the ones that are most pessimistic involve not supporting state and local governments,” Evans said on Aug. 9 on CBS’s “Face the Nation.”

Republican leaders have ignored this warning. Democrats are asking for $1 trillion in state and local government aid; Senate Republicans included no such explicit funding in their initial proposal for the next stimulus bill. Treasury Secretary Steven Mnuchin offered an additional $150 billion as a compromise, which Pelosi rejected, arguing “it’s no use sitting in a room and let them tell us that states should go bankrupt.” To that point, Congress is in recess until Sept. 8, and the fact that both parties are holding their respective presidential nominating conventions in the coming two weeks raises doubts that much progress will be made until lawmakers return.

This kind of partisan squabbling is antithetical to how the Fed does things in general and certainly the opposite of how it has reacted to this sharp slowdown and spike in unemployment. If policy makers see something that could derail the economic recovery — say, frozen credit markets leading to a liquidity crunch and a wave of bankruptcy filings — they haven’t hesitated to come up with novel solutions.

That doesn’t mean the Fed is entirely immune to political calculations. If the central bank really wanted to bolster local governments itself, it never would have set such high “penalty rates” for them to borrow through the Municipal Liquidity Facility. Powell and his colleagues recognize that federal grants are a more effective form of stimulus than debt, given that states and cities have to balance their budgets and can’t simply rely on deficit financing to get them through the pandemic. They’re also sensitive to the optics of a group of unelected technocrats being seen as bailing out some states. In some ways, that’s potentially more divisive than coming close to backstopping shares of Apple Inc.

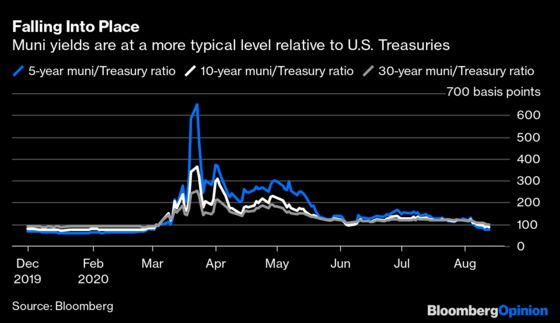

The good news for the Fed is the $3.9 trillion muni market is taking Washington’s bickering in stride. In fact, the oldest gauge of tax-exempt yields, the Bond Buyer index of those on 20-year general-obligation bonds, fell in the week through Aug. 6 to 2.02%, the lowest since 1952. Meanwhile, the ratio of 10-year muni yields to benchmark Treasuries slid to a five-month low, indicating that states and localities can borrow at the cheapest rate relative to the U.S. government since the start of the pandemic. Munis have rallied so much that BlackRock Inc. said it’s cutting back on duration risk given “stretched valuations.”

Even still, I’d prefer to see the Fed offer interest rates that are in the ballpark of current market levels. As it stands, President Donald Trump’s executive-action workaround to provide fiscal relief is practically an anti-stimulus plan for states, which need all the help they can get as they combat sporadic Covid-19 outbreaks. Huge borrowing isn’t ideal, but at a modest short-term rate it at least staves off further layoffs and cuts to public services.

Regardless, this is not a market in need of the Fed’s help. That’s what makes the central bank’s move — and the timing of it in particular — all the more telling. The gentle squeeze in yield spreads serves as a reminder to private muni investors that the Fed’s pricing scale isn’t set in stone and that its facility will step in to absorb any significant selloff. At the same time, supporting states and cities with this kind of action serves to back up policy makers’ arguments that local governments are too crucial to America’s economic recovery to languish because of congressional infighting.

As Bloomberg News reported, the Republican plan did include $105 billion for schools and $16 billion in grants to states for coronavirus testing, contact tracing and surveillance. It would also give states and municipalities more flexibility on how to use unspent portions of the $150 billion provided in the virus relief bill passed in March. But no widespread aid.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.