Federal Reserve Turns Hawkish Now to Avoid Real Pain Later

(Bloomberg Opinion) -- The Federal Reserve, caught embarrassingly offside in its view of U.S. inflation, had to do something to wrest back the narrative with its final policy decision of 2021. What appears to be a sharply hawkish pivot — a forecast for three interest-rate increases in 2022 — is likely a gambit that a tougher stance today will make for a softer economic landing in the coming years.

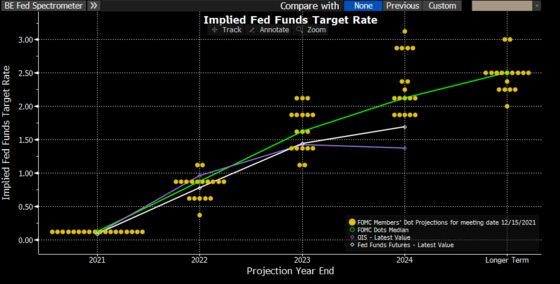

The U.S. central bank said Wednesday that it would accelerate the tapering of its bond purchases, scaling back by $30 billion a month rather than the $15 billion pace it announced just last month. That moves the end date to March instead of June, opening up the possibility that policy makers could raise the fed funds rate from its current range of 0% to 0.25% as soon as the first half of 2022. Indeed, the updated “dot plot” forecast of the short-term benchmark shows a median expectation among policy makers for three interest-rate increases next year, up from less than one in September. And two officials expect to increase rates four times in the coming 12 months, potentially putting the March decision in play for liftoff from the zero lower bound.

In case it wasn’t already obvious, inflation is weighing heavily on the minds of Fed officials, who badly underestimated the staying power of consumer price growth. The median forecast among policy makers is now for the personal consumption expenditures price index to be 2.6% in 2022, up from 2.2% in September’s projections, and the core measure to be 2.7%, up from 2.3%.

Former New York Fed President Bill Dudley, writing for Bloomberg Opinion, correctly anticipated that policy makers would signal three interest-rate increases in 2022, while the consensus among economists was for just two. However, he thought the dot plot would show four more in 2023 and enough in 2024 to get the projected target rate to 2.5%, which is considered “neutral.” Instead, officials penciled in just three rate increases in 2023 and two more in 2024, leaving the central bank in an accommodative stance.

Of course, it’s far from a sure thing that even three interest-rate increases in 2022 will do much to jolt inflation back toward 2%, so the Fed may yet have to do more in future years. Still, the sharply hawkish turn now, combined with the expectations that inflation will return close to 2% by 2023, leaves little doubt that the Fed is aiming to jawbone price growth lower now to avoid having to follow through with a larger number of rate increases later, which could in a worst-case scenario push the economy into a recession. Powell has said before that “we’re going to need a long expansion” to get back to the pre-pandemic labor market, which in turn will require getting inflation under control. In the mind of the recently re-nominated Fed chair, that means interest-rate increases coming sooner.

Part of the central bank’s new longer-term monetary policy framework involved somewhat deliberately falling behind the curve on inflation — requiring officials to observe price growth at or above 2% for a while to make up for persistently undershooting the target. But the inflation narrative has moved too swiftly against Fed officials in recent months, with the consumer price index just hitting a nearly four-decade high. It reached the point that without more quickly ending bond purchases, which opens the door to interest-rate increases starting early next year, the central bank risked losing credibility on maintaining price stability.

Recall that Powell was pressed in September 2020 to define each of the central bank’s benchmarks to lift rates from zero. He largely ducked the question, but this was how he described the requirement that inflation “moderately exceed 2% for some time”:

“What does moderate mean? It means not large. It means not very high above 2%, it means moderate. I think that’s a fairly well-understood word. In terms of ‘for a time,’ what it means is not permanently and not for a sustained period. We’re resisting the urge to try to create some sort of a rule or a formula here, and I think the public will understand pretty well of what we want. It’s actually pretty straightforward.”

It turns out it actually wasn’t.

Fed policy makers, and, by extension, Biden administration officials, spent most of 2021 using the term “transitory,” only for Powell to abruptly say on Nov. 30 that it’s “a good time to retire” that word. Soon thereafter, November’s U.S. consumer price index rose at the fastest annual pace since 1982. The New York Fed’s survey of consumer expectations shows the median estimate of inflation three years from now is 4%, hovering near the highest since at least 2013. A year from now, Americans expect a 6% rate — hardly moderate.

In an important exchange during his press conference, Powell discussed what used to be called “the balanced approach provision,” which kicks in when the central bank’s goals of full employment and price stability are in tension. “It is a provision that would enable us to, in this case because of high inflation, move before reaching maximum employment,” he said. He added that “we’re making rapid progress toward maximum employment” and “I don’t know we’ll have to invoke that.” But just bringing it up hammers home the point that he and his colleagues will start tightening next year to bring price growth back to trend.

Here’s another crucial comment on the trade-off between inflation and the labor market from Powell, which will likely be the Fed’s party line in the months ahead:

“One of the two big threats to getting back to maximum employment is actually high inflation. Because to get back to where we were, the evidence grows, it’s going to take some time. What we need is another long expansion.”

…

“That’s what it would really take to get back to the kind of labor market we’d like to see. And to have that happen, we need to make sure that we maintain price stability.”

The Fed hasn’t raised interest rates yet, but make no mistake: It’s lining up on the starting blocks. Policy makers are hoping that a sprint in 2022 to catch up to the inflation reality will allow the economy to settle into a marathon pace rather than run short of breath.

More from other writers at Bloomberg Opinion:

- In Closing Out 2021, Powell Needs Room to Maneuver: John Authers

- The Fed Can’t Make People Go Back to Work: Michael R. Strain

- The Fed Faces a Troubling 1965 Parallel: Narayana Kocherlakota

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.