Exxon Lost 6 Billion Barrels, Which Sort of Matters

(Bloomberg Opinion) -- Six billion? Six shmillion.

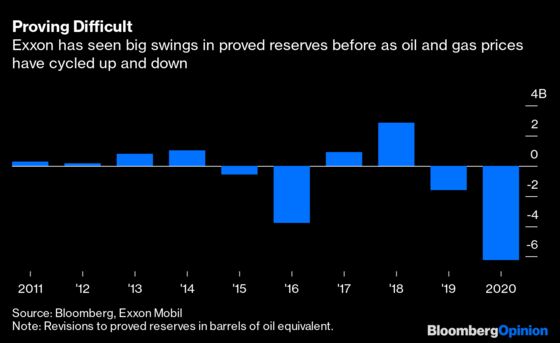

Exxon Mobil Corp.’s annual filing with the SEC, which dropped late Thursday, reveals the company debooked 6.3 billion barrels of oil equivalent in 2020, or almost 30% of its proved reserves. That’s a lot of oil and gas gone.

Except it’s not really gone. Proved reserves are a marriage of geology, economics and artistry. The SEC requires companies to estimate annually how much oil and gas they have below the ground that can reasonably be expected to see the light of day. That reasonableness is largely a function of moving targets: quality of reserves, market prices for oil and gas and expectations of how much the barrels will cost to produce.

Given last year’s Covid-19 crash, it’s hardly surprising that Exxon, along with other producers, was forced to debook a lot of barrels. The same thing happened in 2016, when oil prices bottomed out below $30 a barrel, and Exxon subsequently rebooked a lot of them when prices recovered. The sheer scale of the revisions — last year’s swing was bigger than the entire proved oil reserves of Mexico — raises eyebrows. But these are mathematical adjustments to theoretical constructs.

And yet.

Blithely shrugging off the sudden disappearance of a country’s worth of oil and gas requires ignoring context of roughly similar scale. You don’t just watch as more than a quarter of your most important asset fades on the page like old newsprint and say anyhoo.

While debooking reserves isn’t the same as taking a financial impairment, Exxon just took a big financial impairment. That rather tells you something more fundamental went wrong in the asset base. So does a cursory glance at some other indicators.

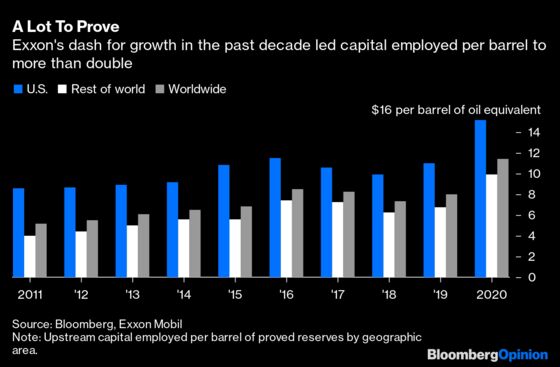

In the past decade, capital employed in Exxon’s upstream business has risen by a third — and that’s net of write-downs. Despite that, production fell 17% and proved reserves by 39%.

Last year’s oil crash, as well as the one five years before, caused those numbers to spike. But the upward trend was apparent before that. This captures the biggest issue that has trashed Exxon’s return on capital and put it in the crosshairs of activists. The company lost its famous discipline with big spending on megaprojects such as liquefied natural gas and Canadian oil sands.

The latter has been a big factor in the proved reserves whiplash, due to a combination of relatively high costs and big discounts on Canadian barrels struggling to secure pipelines to market. Exxon debooked 3.8 billion of them in 2016 when the Canadian benchmark price averaged just under $30 a barrel; rebooked 3.3 billion in 2018 when it averaged $38; and took them down 3.9 billion again when it fell back below $28 .

So maybe those will come back again now that oil is moving up. But does that sort of trading call really comfort investors when it comes to an amount of oil equivalent to a quarter of the company’s reserves? And what would higher, widespread carbon pricing mean for bringing back some of the most carbon-intensive barrels in the world?

Next week, CEO Darren Woods will face analysts and investors to reassure them Exxon’s spending is back under control, its dividend is safe and it has a portfolio of investment opportunities that work at lower oil prices, including the big shale bet that has defined much of his tenure so far. The lost-but-still-there barrels may be brushed off as an accounting wrinkle. Yet the underlying need to generate a return on all that investment spread over fewer barrels is the only thing that matters.

Exxon reports its Canadian proved reserves together with "Other Americas". However, the bulk of these relate to what Exxon classifies as bitumen and synthetic oil, which relateoverwhelmingly to its Canadian operations.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.