(Bloomberg Opinion) -- You can’t turn a supertanker quickly, as the old saying goes. Bailing out, on the other hand, takes no time at all.

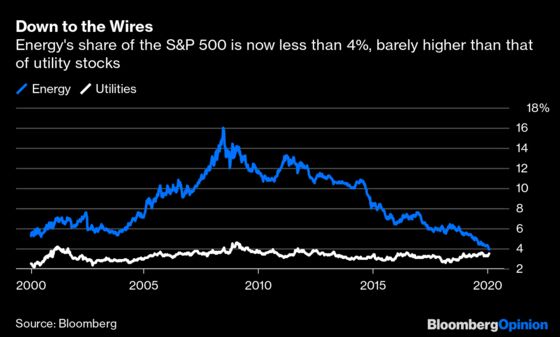

Friday’s double dose of weak Big Oil earnings from Exxon Mobil Corp. and Chevron Corp. followed hard on the heels of Royal Dutch Shell Plc’s debacle on Thursday. Shares of both companies were down about 4%. The market was ahead of them, though: Last Monday, energy’s weighting in the S&P 500 Index slipped below 4% for the first time in at least four decades. Incredibly, that weighting is now less than half a percentage point above that of the utilities sector:

My colleague Nathaniel Bullard and I wrote last year about how energy’s dividend yield had recently reversed a decades-long relationship with that of utilities by rising above it. On Friday, the spread widened to a record, with energy’s yield of 4.3% now a full 1.5 percentage points higher than utilities. Short-term factors are at play here, of course; coronavirus, especially, has pushed money toward perceived havens like utilities and away from oil. But that is exacerbating an existing revolt as investors have looked at Big Oil’s track record of managing capital and demanded more of it back.

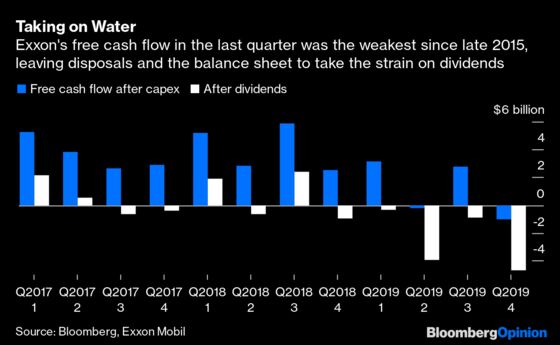

Exxon’s fourth-quarter results stoked that backlash in spades. Performance was weak across the board. Exxon’s integrated model took hits on oil and gas prices in the upstream business and weak margins in both refining and chemicals. Meanwhile, a counter-cyclical investment spree promises great things in areas such as Guyana’s offshore discoveries and improvements in refinery performance, but right now it is a cash sink. Exxon’s cash from operations failed to cover capital expenditures, and it was the fifth quarter in a row in which the company resorted to asset sales or borrowing to cover its dividend.

The underlying, and continuing problem, is weak returns. Exxon’s return on equity was notably less than its 5.6% dividend yield — itself the highest since the merger that formed the company two decades ago; investors have backed away and thereby raised the threshold demanded.

Rival Chevron also had a bad morning, albeit better in key respects. Return on equity of 7.5% for the fourth quarter still isn’t where it needs to be, but it was still roughly 2 percentage points higher than Exxon’s. Moreover, Chevron covered its capex and about two-thirds of its dividend payment from cash flow. With this year’s capex budget held flat, the company has more flexibility, raising its dividend by 8.4%. Throw in $5 billion of buybacks, and Chevron’s all-in payout yield for 2020 of 7.2% compares with Exxon’s prospective yield of less than 6%.

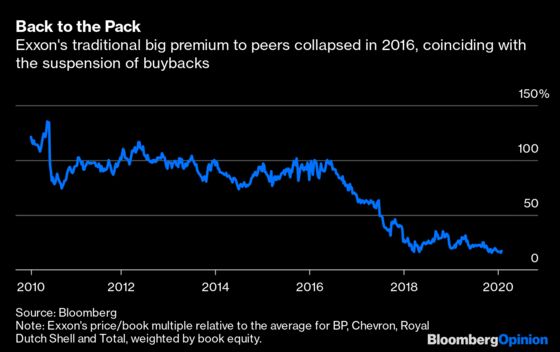

Exxon’s inability to restart its buyback program, which used to be its calling card, is a big reason its traditional premium has plunged. Exxon’s price-to-book ratio used to be roughly double that of its peers, but the suspension of buybacks in 2016 coincided with a big relative decline in the multiple placed on its book value by investors. Exxon would respond that its buybacks are for excess cash and that it is investing in growth assets to generate future returns. Its problem is that energy investors’ benefit of the doubt is in exceedingly short supply.

Even so, Exxon retains a premium that is looking ever harder to defend. It was notable that Chief Executive Officer Darren Woods joined the earnings call Friday. Yet his demurral in response to a question about the price assumptions the company uses for budgeting — referring the analyst to the company’s energy outlook for clues — carried an echo of the old days when Exxon’s solid financial performance allowed it to brush off such requests. Today, with Big Oil’s relative position in the stock market slipping beneath the waves, it feels like a relic of a bygone age. As former supermajor ConocoPhillips demonstrated a couple of months ago, this is a time to over-deliver — not just cash, but information. It’s the only way to keep investors on board.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.