(Bloomberg Opinion) -- More than most weeks, Big Oil had reason to cheer the arrival of Friday. The day before, the CEOs of Exxon Mobil Corp., Chevron Corp. and other industry bigwigs had been called to Congress (virtually) for one of those hearing/shellacking rituals, where they were accused of hiding the dangers of climate change. This weekend, the latest UN climate summit kicks off in Glasgow, an event not generally conducive to Big Oil’s health.

Friday, poised between the two, saw Exxon and Chevron doing what they prefer: reporting giant profits. Chevron’s beat was bigger, but both delivered what oil investors demand these days. Combined free cash flow for the quarter of almost $15 billion is the highest in at least a decade and isn’t far below the $18.6 billion they reported for the entire year of 2019, before the pandemic. Exxon announced the resumption of buybacks for the first time in years.

The inverse of the world’s anxiety about winter energy shortages is higher prices, portending a good fourth quarter to follow. As an added bonus, it provides a schadenfreude-inflected counterargument on days like Thursday. Exxon CEO Darren Woods mentioned it in his opening remarks to the House Oversight Committee to emphasize the difficulty of moving away from fossil fuels.

As an added added bonus, one of those oil majors moving a bit more quickly than most, Royal Dutch Shell Plc, has attracted the attention of an activist, Third Point LLC’s Dan Loeb, calling for it to split its green operations (plus gas) from its old oil business. And as an added, added, added bonus, even as Woods was being grilled, congressional Democrats were still wrangling over President Joe Biden’s (reduced) budget, leaving him with less ammo as he headed off to Europe.

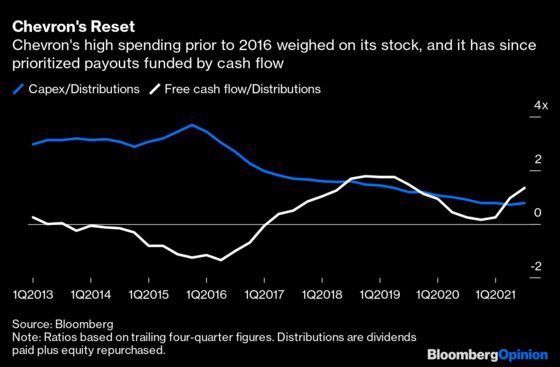

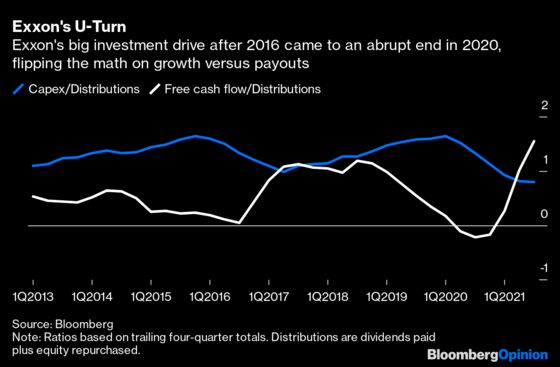

And yet, as satisfying as that all may be in the moment, it can also be read from a different perspective. Those stellar results, for example, reflect a favorable recovery in demand and energy prices, a hyper-cyclical turn in commodities. In terms of what the companies actually control, the most salient aspect is that they remain committed to paying out cash rather than spending it. With oil around $80 a barrel, Chevron and Exxon are now spending about 40% less than the last time prices were so high. Even if, as I think, this reflects penance for past sins more than new religion on energy transition, the model fits that theme anyway.

Energy’s weighting remains stuck below 3% of the S&P 500. This continuing relative ambivalence from investors can be blamed in part on lingering memories of poor performance. Yet it also reflects other elements that can be loosely grouped under the moniker of ESG.

Energy’s low weighting reflects in part the heavy weighting of existential rivals such as Tesla Inc. Is it worth a trillion? I don’t think so, but (a) I could be wrong and (b) it doesn’t matter in this context. What matters is that oil majors are being forced to return cash while opposing businesses can raise as much as they like. You can read Friday’s news that Amazon.com Inc. has a 20% stake in electric truck maker Rivian Automotive Inc. in much the same way.

Meanwhile, news that giant Dutch pension fund ABP is joining the divestment movement is a blow, not just for Shell, but for the entire sector. And as much as Loeb casts a shadow over the theme of oil-major transitions, he surely drew encouragement from Exxon’s earlier proxy-battle defeat at the hands of a small transition-minded fund.

This is not to say Big Oil’s Friday feeling is illusory. Rather, it’s a bright spot in an otherwise murky environment.

The Oversight Committee hearing was of course kabuki theater. But the underlying issue of oil’s relationship with society being corroded by irresponsible lobbying isn’t a fiction, as that recent footage of an Exxon lobbyist displayed all too well. Woods may be right that Exxon’s public view on climate change has “evolved” since the days of former CEO, and arch-skeptic, Lee Raymond, just as the scientific consensus has. But come on. That scientific consensus hasn’t undergone some amoeba-to-homo sapiens leap; it’s just gone from from sure to really really really sure.

Similarly, even if Biden’s green plans are truncated, passed in their current form they would still be the biggest green federal support package ever. Glasgow, meanwhile, almost certainly won’t deliver some transformational agreement. But it has already elicited more net-zero pledges from even the unlikeliest of candidates and may also bring progress on less ballyhooed, but important, issues such as international emissions trading. The Paris Agreement abides.

Kevin Book of ClearView Energy Partners captures succinctly the real danger posed to Glasgow’s negotiators by price spikes that “tend to usher out incumbent politicians faster than they usher in new technologies.” Even if that disrupts the broad trend toward decarbonization, though, it’s tough to imagine it being derailed altogether, especially if momentum in capital markets endures. As ever, enjoy Fridays for what they are, while accepting that another Monday’s never far off.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.