(Bloomberg Opinion) -- It’s a good day for Exxon Mobil Corp. Oil prices are up.

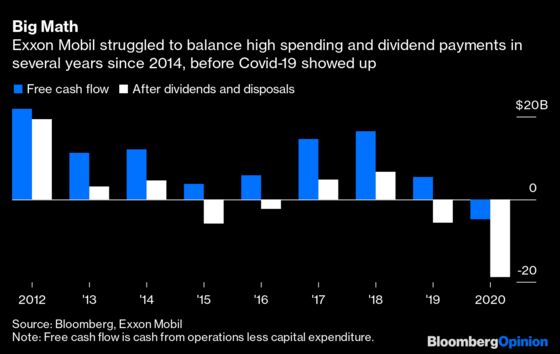

Tuesday’s earnings report? That was not so good. Exxon reported its first annual loss in at least three decades. Within that, it took a $19 billion impairment. Free cash flow swung negative to the tune of almost $5 billion, or almost $20 billion after dividends were paid out. Net debt to capital, 19% at the start of last year, jumped to 29%.

Last year was bad for everyone, but among the oil majors, Exxon had it worse because it had further to fall. Besides the red ink, it was forced to adjust strategy, faced doubt about its sacrosanct dividend and even attracted the attention of activist funds. Along the way, there was a whistleblower complaint that Exxon was overvaluing its Permian assets and a report that it considered merging with rival Chevron Corp. All in all, a very un-Exxon cascade of events.

Since late November, just before the activists went public, Exxon has tried to draw a line under all this. The release itself reflected this, with a greater level of detail than investors and analysts are used to. There was an extensive discussion of Exxon’s ambitions in carbon capture. A new director has been elected to the board, with more to come.

The immediate priority concerns the cash flow math. It was Exxon’s giant capex budget, and the resulting strain on the balance sheet as the company borrowed to fund its dividend — even before Covid-19 struck — that got it into trouble. Reassurance on this front is paramount, and Exxon went a long way in doing that on Tuesday.

In particular, Exxon made it plain that capex will take the fall before the dividend does; the budget for this year is the lowest since the merger with Mobil Corp. back in 1999. More importantly, Exxon provided specific breakeven oil-price assumptions. It now expects to cover this year’s low capex figure and the dividend at somewhere between $45 and $50 a barrel (Brent has averaged almost $55 so far this year, versus about $42 in all of 2020). By 2025, reductions in operating expenses and cash flow from new projects are projected to reduce that breakeven to more like $35 a barrel, with capex of more like $20 to $25 billion supported by Brent at $45-$50.

This alleviates concerns around the dividend; the yield, which had been creeping back up toward 8%, was below 7.5% by the end of Tuesday morning’s call.

But it would be going too far to say this has drawn a line under Exxon’s problems. Consider it more like Exxon having embraced the notion that it has problems.

A curious thing has happened. As 2021 dawns, the differences between the oil majors are wider than they have ever been, mainly around strategies to deal with the energy transition. This follows two decades during which they were, at least in terms of business model, largely interchangeable. Yet Exxon, long distinguished by superior financial performance, has actually moved closer to the pack in that regard. This is reflected in the loss of its traditional valuation premium — and leaves it in the unfamiliar position of having to win back trust.

So while the new cash-flow guidance is what investors want to hear — more humble oil than Big Oil — it remains to be seen how well Exxon can actually balance that dividend, capex, paying off debt and growing earnings. Implicitly, Exxon needs oil to move higher; hence the helpful backdrop provided by $57 Brent on Tuesday. And it’s lost on no one that Exxon reached this point only after the ravages of 2020 and the arrival of shareholder activists.

The same applies to the company’s new focus on carbon capture. In terms of energy-transition technologies, carbon capture fits most neatly with Exxon’s worldview of rising demand for oil. Yet it is stretching things to breaking point in claiming, as Exxon did Tuesday, that carbon capture “mitigates emissions at an affordable cost.” Yes, the Intergovernmental Panel on Climate Change has estimated the cost of limiting temperature change below 2 degrees will be much higher without the deployment of carbon capture technology. That certainly gives Exxon grounds to work toward it.

But as the past decade has demonstrated amply, what’s “affordable” in energy and climate terms is a fast-moving target. And as the company acknowledges, making the business work at scale will require governments to implement more policies that incentivize it. Only last week, America’s only project capturing carbon from a coal-fired power station was shuttered (ironically, because it needed higher oil prices to work). This stuff is hard and expensive, and Exxon has only just organized it as a dedicated business line — again, only after activists showed up.

So there is potential there, but much to prove. Moreover, the focus on carbon capture still speaks to a mindset geared to higher oil demand, leaving Exxon vulnerable if the world doesn’t work out that way. Right now, it’s an oil major focused on preserving its ability to pay out capital, fighting against upstarts enjoying the peculiar indulgence of a green bubble.

There has been an explosion of investment in other transition technologies such as electric vehicles. General Motors Co.'s recent announcement that it intends to sell only zero-emission vehicles by 2035 should unnerve Exxon’s leadership. That isn’t because GM is leading the charge; indeed, its “aspiration” had a sheen of greenwash. Rather, even if GM achieves only half its objective, that has huge implications for oil demand — precisely because there’s a decent chance GM would be a laggard compared with others.

If Exxon’s hunch that lower investment in oil supply is teeing up a sustained increase in prices, then its focus on resilience at lower prices will pay dividends (or protect them at least) in the near term. The bigger question — whether there’s a long-term future for a $15 billion dividend as oil demand flattens and falls — remains hanging.

Net debt divided by net debt plus shareholders' equity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.