Careful Choosing Your Oil Supertanker in the Trade Storm

(Bloomberg Opinion) -- So, energy investors, to recap:

- The U.S. just branded China a currency manipulator in the latest escalation of the trade/currency/who-will-run-things-in-the-21st-century war;

- Venezuela – where, like fellow OPEC member Iran, Washington thinks some regime modification is in order – just got some new sanctions;

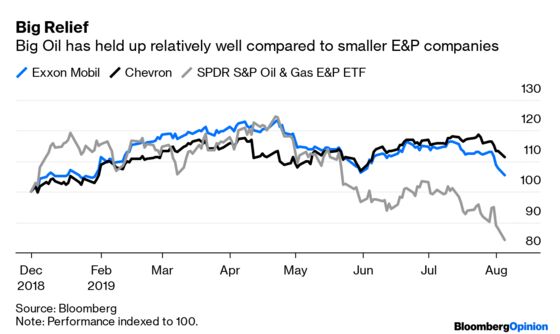

- The SPDR S&P Oil & Gas Exploration & Production ETF closed at its lowest level since March 9, 2009 (the week the S&P 500 hit bottom after the financial crisis).

Interesting times. And at such times, oil investors would typically run for the relative safety of the majors, and one in particular: Exxon Mobil Corp. Except that it is also interesting times, or timing, for Exxon.

Today’s apparent reprieve in the currency war, with the Chinese yuan nudging back below 7 to the dollar, is far from an armistice. The long list of U.S. grievances against China, from FX to fentanyl, along with President Donald Trump’s November 2020 timetable and President Xi Jinping’s lack of one, portend a drawn-out conflict. This is why Brent dipped briefly below $60 this morning, even though the U.S. has not one but two OPEC producers under tightening sanctions.

Oil majors, with their bigger balance sheets and diversification, usually do better than their smaller brethren at such times. And lately they have.

The latest earnings from Exxon and Chevron Corp., however, suggest the smaller of the two may offer a better refuge this time around.

Exxon missed the consensus earnings estimate (after stripping out a tax-related gain in Canada). The real issues lay beneath that number, starting with the nominally defensive chemicals business. Profits here collapsed by almost 80% compared to the same quarter in 2018, to their lowest in years. Exxon characterized this as a temporary problem of excess capacity, albeit one that was likely to weigh on pricing for the next 12 months. What’s tricky about this is (a) excess supply is always also a function of demand, and (b) the trade war could have something to say about that.

Exxon’s real engine, the upstream business, isn’t suffering to nearly the same degree but isn’t firing on all cylinders either. Absent that tax benefit, earnings were flat with the first quarter, despite higher crude oil prices. Lower output and falling gas prices were to blame, but so too is Exxon’s weaker position vis-à-vis Chevron in their increasingly important shale portfolios. The latter’s U.S. upstream business has earned more than $2 for every one Exxon has earned over the past four quarters. If oil prices remain weak (or even weaken further), Exxon looks more vulnerable in this regard.

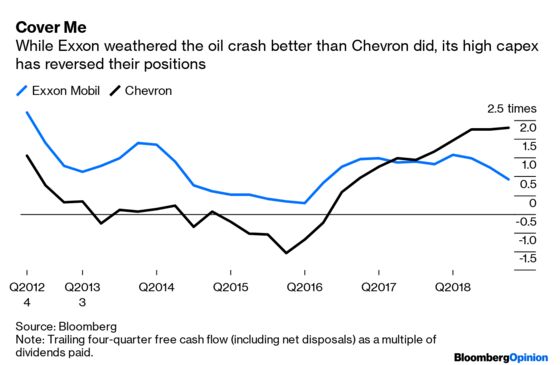

There is an element of luck at play here, and timing is against Exxon. When oil prices first collapsed toward the end of 2014, Chevron was in the doghouse because it was locked into heavy spending on some major liquefied natural gas projects. It is now over that hump – just as Exxon has moved into spending mode.

The result is that, while Exxon had to borrow to cover its dividend in the second quarter, Chevron’s free cash flow covered its own payout twice over; and it’s resuming buybacks after its brief pursuit of Anadarko Petroleum Corp. (which also netted it a break fee and plaudits for walking away).

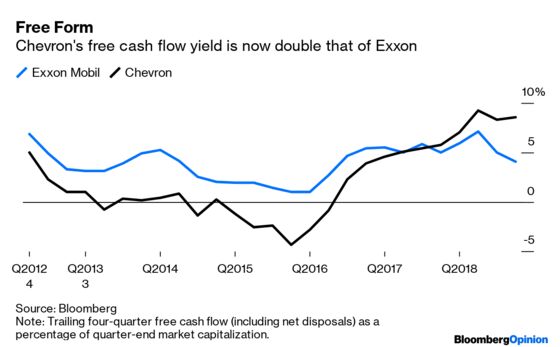

Those payouts are critical in keeping an already skeptical investor base onside. But while Exxon now yields almost 5% on dividends versus Chevron’s 4%, the latter’s buybacks chip another 2% or so of yield. In terms of trailing free cash flow yield, there’s no contest.

Dividend yield aside, on every measure from earnings to book value, Exxon continues to trade at a premium. As insurance against what promises to be an ever more interesting year or so, that’s tough to justify.

A note on this ETF, the XOP, to use its ticker. Though it is billed as focused on exploration and production, it actually has a hefty weighting of refining stocks, too – six out of its top 10 holdings, in fact. Which means the E&P sector’s performance is worse than even the XOP suggests. Look at the Russell 3000 Crude Producers sub-index, for example, and it is actually substantially below the level of early 2009. (Hat-tip to Kevin Kaiser, @kfkaiser17, for pointing this out).

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.