Brexit Deal: Here's What Will Happen to U.K. Interest Rates

(Bloomberg Opinion) -- It can’t be much fun being a central banker when there’s a binary event like Brexit to make a mockery of all economic forecasts.

The Bank of England has stuck resolutely to its expectation that it will raise rates over its three-year forecast horizon. But there are clear signs that several members of its Monetary Policy Committee are wavering as the global growth picture dims and the rest of the major central banks cut rates.

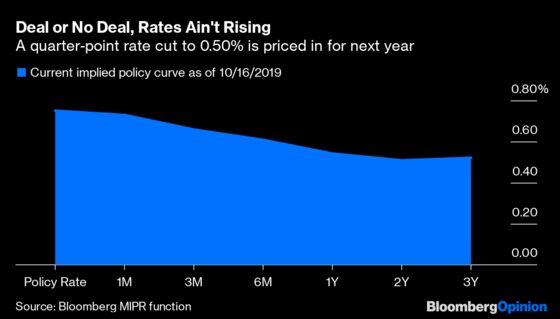

This means the BOE is catching up finally with what the money markets have long priced in: A quarter-point rate cut probably sometime in the middle of next year. Traders are well aware that even if Prime Minister Boris Johnson manages to pull off a miracle and delivers a Brexit deal, any subsequent market bounce would struggle into the economic headwinds of U.S. President Donald Trump’s international trade wars. And that’s before Britain’s really crucial negotiations begin with the European Union over a long-term trade deal. Those talks will be brutal.

The International Monetary Fund on Tuesday trimmed its global growth estimates yet again to just 3% for this year. The U.K. may be an island but it’s highly exposed to global trade.

Gertjan Vlieghe, an external member of the MPC, said in a speech at Bloomberg on Tuesday that the case for an interest rate hike had evaporated, citing rising economic slack and the worsening international outlook. That echoed an even more surprising interview on Bloomberg TV last week with the BOE’s resident hawk Michael Saunders, where he suggested a rate cut might be needed even in a smooth Brexit scenario. Mark Carney, the bank’s governor, repeated on Tuesday that rates could be cut close to zero in a downturn. The bar for a rate hike has got a lot higher.

Recent U.K. economic data show signs of weakening, led by a surprise 56,000 drop in August in the three-month rolling average of employment. The rise in average weekly earnings (including bonuses) — a key criteria at the bank for rate hikes — dipped from 4% to 3.8% in August. The September survey of purchasing managers dropped below the 50 growth line. Even inflation is on the wane, with consumer prices dropping to 1.7% in September, below the bank’s 2% target. Growth is unlikely to rise much higher than 1% for the foreseeable future.

Where the pound eventually settles after an eventual Brexit resolution will be a key policy determinant; a sustained rally would naturally cap inflation, undermining any case to raise rates. Of course if a deal was achieved and Johnson capitalized by winning a majority in a general election, it would unleash a fiscal splurge and upward pressure on prices. But this outcome is far from certain and would most likely encourage the bank to sit on its hands to assess the impact on wage inflation.

The economic reality is that the world’s slowing down, and even a partial trade deal between the U.S. and China wouldn’t repair all of the damage to the manufacturing sector’s confidence. It will be a similar story with Brexit; much of the lost output and investment will never be recovered. The U.S. Federal Reserve is on a rate-cutting cycle and the European Central Bank has left its incoming president Christine Lagarde with a full range of stimulus options. The BOE will find that easing trend hard to resist even in a “sunlit upland” Brexit.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.