(Bloomberg Opinion) -- Launching a special purpose acquisition company has been pretty easy with all the money sloshing around the financial system. Finding a target for the SPAC that shareholders get excited about is another matter. Billionaire entrepreneur Richard Branson knows plenty about dealmaking. Even he’s struggling now.

A SPAC raises cash in an initial public offering and then looks for a company to merge with and thereby take public. So far this year these cash shells have raised more than $90 billion in North America, surpassing 2020’s haul in less than three months.

But with bond yields rising investors have other options to deploy cash and SPAC fever has cooled. One benchmark, the IPOX SPAC index, has entered a bear market and hundreds of SPACs are trading below the $10 level at which they sold units (consisting of a share and a fraction of a warrant) to the public. Only a few weeks ago most traded at a chunky premium to their cash holdings. For SPACs like Branson’s, which have announced but not completed deals, the downdraft creates a unique set of problems.

The bearded tycoon’s first SPAC , VG Acquisition Corp., announced a $3.5 billion deal in February to merge with 23andMe, a genetic-testing company for regular consumers that provides personalized information about people’s ancestry, genetic traits and health risks. 23andMe can tell if you have a heightened risk of breast or colorectal cancer and inform you of more lighthearted matters, such as a genetic preference for a particular ice-cream flavor.

Cofounded by Anne Wojcicki more than a decade ago, the company wants to use its millions of genetic customer datasets to develop new therapies. 23andMe has a partnership with GlaxoSmithKline Plc to co-fund the drug development. The British pharma giant made a $300 million equity investment in Wojcicki’s company in 2018.

Investors in Branson’s SPAC initially cheered the 23andMe merger plan, but they’ve become less enamored over time. Shares in VG Acquisition Corp. have declined more than 40% since the February peak and trade only a fraction above the $10 level at which the deal was struck.

If a SPAC’s shares fall below $10 it makes financial sense for shareholders to redeem their holdings for cash rather than fund the merger. Depending on the minimum cash requirement the merger parties have negotiated and the level of any concurrent institutional financing (known as a PIPE), a SPAC deal could fall apart. Even if the deal goes ahead, high redemptions could deprive the target company of some of the cash on which it was counting.

Serial SPAC sponsor Chamath Palihapitiya has warned of “busted mergers” if the SPAC market continues to sag. A blank-check company backed by private-equity company Cerberus Capital Management is among more than a dozen SPACs with pending deals trading below $10.

“A lot of SPAC deals were struck a couple of months ago when the market was in a different place,” Julian Klymochko, the boss of Accelerate Financial Technologies Inc., which manages a SPAC-focused ETF, tells me. “I wouldn't be surprised to see some of those recut at lower valuations to prevent the deal failing.” (He was speaking generally and not referring to any particular transaction.)

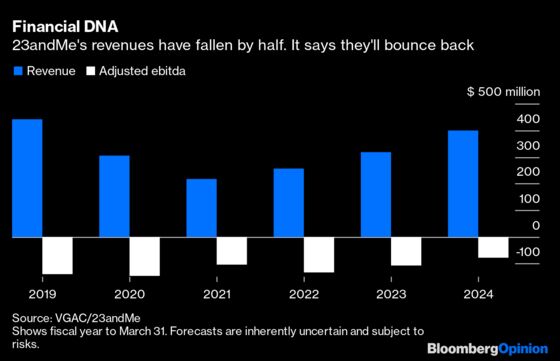

It’s not just the broader market rotation out of growth stocks that’s working against Branson’s SPAC foray. In the past two years 23andMe’s revenues have roughly halved and it makes significant losses. Even in 2024 the company expects revenues will be lower than they were in 2019.

Demand for the company’s personal genetic kits has slowed and much of its past sales growth was bought with expensive internet marketing, the deal prospectus reveals. To reduce losses 23andMe has cut back on advertising spend, undergone a restructuring and laid off about 100 staff. It projects revenue will increase 22% annually until 2024. It started a new subscription service late last year but that won’t generate much revenue to begin with.

I’ve written before about how SPACs’ financial projections are often too optimistic and unreliable and why publishing such information is particularly flattering for startups whose sales are falling. Traditional IPOs usually shy away from making such forecasts.

The slowdown in the consumer business won’t matter as much if 23andMe can use its database to develop new drugs. Its most advanced program, a cancer tumor treatment partnership with GSK, began early human trials last year. However, R&D is expensive and regulatory approvals take years.

In view of these risks you might have expected Branson to negotiate a discount, yet the agreed valuation is $1 billion higher than 23andMe’s last disclosed private financing round. If the SPAC’s share price continues to sink, that would indicate he’s overpaid — and he wouldn’t be the only sponsor to have done so in a euphoric market. An investor reassessment is now underway and even experienced dealmakers will have to sweat.

Branson now has two SPACs and a third is in the works.

The SPAC is obliged to deliver at least $500 million of cash to 23andMe. Including the $250 million Pipe, this means around half the SPAC shareholders could opt to redeem without breaching their agreement.

In some cases GSK will shoulder all the drug development costs in return for a royalty fee

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2021 Bloomberg L.P.