(Bloomberg Opinion) -- It’s the Tiffany T bangle versus the Louis Vuitton Neverfull bag.

Tiffany & Co. this week filed a lawsuit against LVMH Moet Hennessy Louis Vuitton SE seeking to undo the French luxury group’s decision to abandon its $16 billion takeover of the company. Now LVMH is counter-attacking, moving to sue the jeweler over its handling of the Covid-19 crisis.

The twist elevates the tensions between the two sides. Founder and Chief Executive Officer Bernard Arnault may well be trying to negotiate a cheaper deal. But the bad blood ratchets up the risks of such a strategy.

Folding Tiffany into the LVMH empire still makes sense strategically. LVMH has room to expand in jewelry. There is scope to polish up the iconic U.S. brand and, anyway, there aren’t that many targets in luxury that would make a meaningful impact on the French conglomerate, especially ones that lack controlling shareholders.

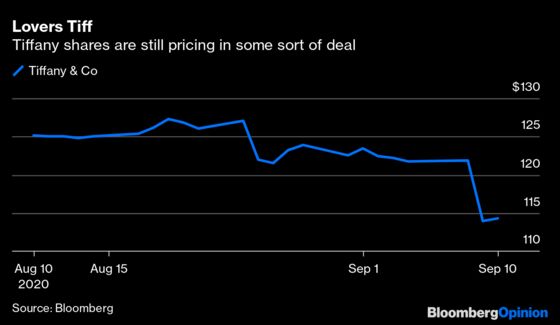

Given the battering that luxury demand has taken from the pandemic – sales could be up to 35% lower across the luxury market this year – the $135-a-share offer price agreed in November is clearly too high. Assuming the deal collapses completely, Tiffany stock could fall to between $70 and $80, according to analysts at Cowen and Company. Adding a 50% takeover premium to that — Tiffany remains a trophy asset — would suggest a revised price of $105 to $120 per share.

At $115, incidentally not far from Tiffany’s current share price, Arnault would be saving about $2.4 billion. That doesn’t sound like small change, but it’s only around 1% of LVMH’s market capitalization.

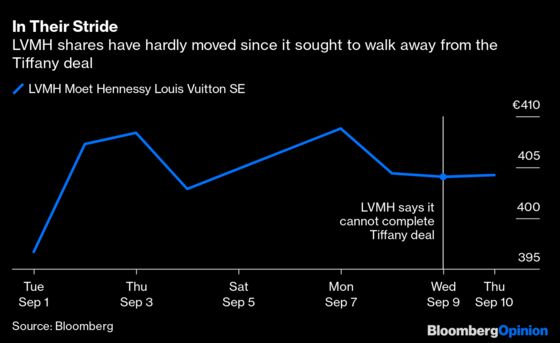

This level of discount might not be worth the reputational damage, particularly if there is a lengthy court battle between the two sides. Shares in LVMH have taken the developments in their stride so far. But for some investors, if they believe he really doesn’t want the deal at all, Arnault’s move might be read as a worrying signal about the strength of LVMH and the future of luxury. While the group’s travel retail division has been badly hurt by the pandemic, its fashion and leather goods division has appeared to be holding up well.

Then there are the risks of antagonizing the U.S. political establishment by dumping Tiffany so dramatically. Suddenly LVMH has become a controversial element of U.S.-French relations.

There could still be an amicable solution. After all, the alternative for Tiffany is continuing with its turnaround against the backdrop of a luxury slump, an economic downturn and a U.S. presidential election. For LVMH, the risk is that this unique asset now gets bought by one of the other big luxury houses.

Arnault is known as a tough negotiator, and he has a duty to his shareholders to get the best value. But the costs of getting this bling bargain look high relative to the likely discount.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.