European Rescue Fund Creates a New Big Beast in Bond Market

(Bloomberg Opinion) -- Congratulations to the European Union for agreeing a groundbreaking deal to distribute 750 billion euros ($864 billion) of grants and loans among its 27 members to bolster the recovery from the pandemic. Now it has to find a way to pay for it. And bond investors are ready, willing, able and eager to help.

Step forward an oven-ready vehicle already used by the European Commission, which already borrows in the name of the EU to satisfy centralized funding needs in the bloc. The Commission can tap the highly liquid bond market to pay for the rescue fund, with the financing spread out over the next seven years in line with the EU budget framework. The actual debt maturities will be much longer and will be spread out across the yield curve, allowing for a lot of flexibility to adjust bond sales to wherever investor demand is strongest.

Austria’s recent successful issue of its second 100-year bond illustrates there’s investor appetite for high-quality assets offering any hint of a yield — or even something whose rates aren’t as negative as other European benchmarks. It also suggests that there’s no upper limit on how long-dated EU bond issues can be, although as markets enter the summer quiet period, it will be wise to tread carefully in assessing investor interest. It will likely initially issue in more liquid maturities such as 5- or 10-year terms before selling longer-dated bonds.

Before long, EU debt will be totally interchangeable with the other liquid sovereign debt issued by European countries. It will become part of the capital market’s furniture.

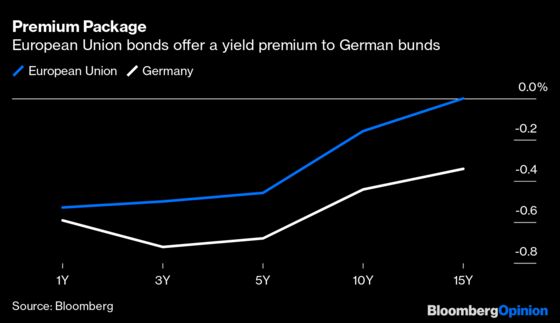

With the European Central Bank’s bond-buying program hoovering up so much of the German bund market, investors are sorely in need of a so-called safe asset. EU debt fits the bill, with credit ratings of AAA from Moody's Investors Service and AA from S&P Global Ratings. The existing market for EU-issued debt issued is small, at just 51 billion euros, of which almost 10 billion euros matures next year, so a boost in supply will meet a need. Annual issuance is in line to increase by 150 billion euros or more, roughly equivalent to a large European country’s needs.

Moreover, with the euro zone’s benchmark debt yields in deeply negative territory — investors pay about 44 basis points for the privilege of lending to Germany for a decade — the premium offered by EU bonds gives bondholders some relief, albeit still at yields below zero. And the new pandemic bond issues might well offer positive yields given their vastly bigger size and the need to keep them attractive.

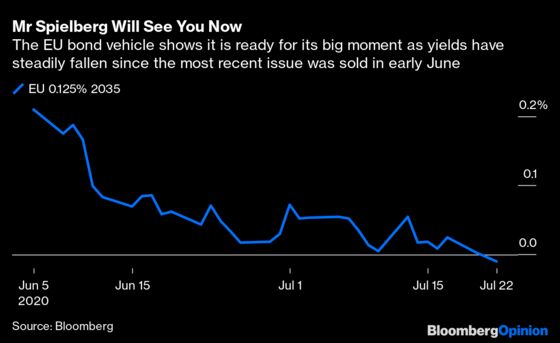

And the prospect of a massive increase in the supply of EU bonds hasn’t frightened the horses. The most recent issue in its name, 500 million euros of 15-year bonds sold at the beginning of last month, has steadily improved in value, driving the yield down to just below zero from an initial level of about 0.2%.

EU debt is already the closest thing to a common bond that exists in the bloc. Needs must: Germany has overcome its mistrust of debt mutualization in its desire to keep the union intact and sanctioned a flood of securities that are euro bonds in all but name. The rescue package may not meet the definition of a Hamilton moment, but it marks a true turning point in the EU’s relationship with the capital markets.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.