Europe’s Biggest Fund Managers Ride the Passive Wave

(Bloomberg Opinion) -- The failure of active fund managers to beat their benchmarks during this year’s fervid markets reinforces the argument that many investors would be better off buying low-cost index tracking funds. That backdrop is providing a handy boost to asset management firms that have built a stable of passive products, with DWS Group GmbH and Amundi SA reaping the benefits of having healthy exchange-traded funds businesses.

In Europe’s mutual funds market, known as Undertakings for the Collective Investment in Transferable Securities or UCITS, the percentage of net sales that went to exchange-traded funds climbed to 27% last year, up from 15% in 2018 and just 7% in 2015, according to the most recent figures compiled by the European Fund and Asset Management Association.

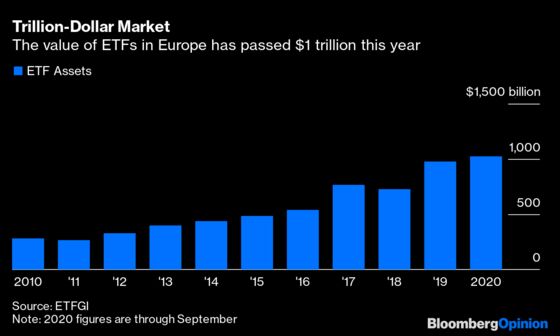

That trend has continued this year. Europe’s ETF market has surpassed $1 trillion in value for the first time, with assets doubling in the past five years, according to research firm ETFGI.

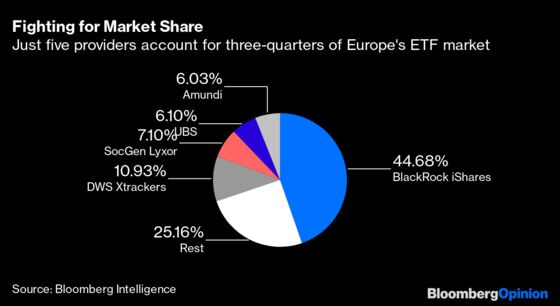

BlackRock Inc. dominates the European ETF market, as it does globally. But just five firms account for three-quarters of the sector in the region, with DWS ranked second and Amundi coming fifth in the league table of index-tracking product providers.

DWS said last week that it attracted net inflows of 10.5 billion euros ($12.3 billion) in the third quarter. The bulk of the new money flowed into its passive product range, which grew by 6.3 billion euros, while its active strategies suffered net outflows of 935 million euros. That echoed the second quarter, when passive attracted 6.5 billion euros while active suffered withdrawals of 4.1 billion euros.

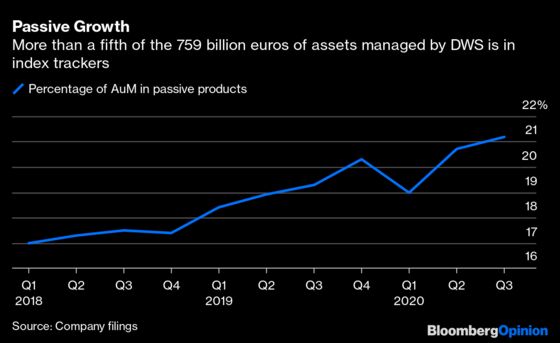

As a result, the percentage of the German fund’s assets that are in its index-tracking offerings has climbed to a record 21.2%, accounting for 161 billion euros of its 759 billion euros of total assets.

Amundi also saw its passive business grow in the third quarter. It said last week that net inflows of 3.2 billion euros boosted its assets in the category to 138 billion euros, out of a total under management of almost 1.7 trillion euros.

To be sure, selling index trackers is a low-margin business. When it last broke down the figures in 2019, DWS said the management fee levied on its passive business was just 21 basis points, down from 23 basis points a year earlier and compared with the 76 basis points it was able to charge for active equity management.

But charges for active management have also been dropping. Standard Life Aberdeen Plc, which has resolutely shunned the passive arena, was able to levy a management fee of just 27.9 basis points in 2019, down from 31.1 basis points in 2018.

Increasing your share of a growing market, even where fees head inexorably lower, still beats battling in active products that customers are shying away from. And with stock pickers continuing to disappoint their customers, asset management firms that don’t have the cushion of a suite of index trackers to offer clients should seriously consider expanding their horizons — and their product ranges.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.