(Bloomberg Opinion) -- In business, Adam Smith’s invisible hand often does the job of aligning the supply of and demand for financial products to the benefit of both buyers and sellers. Sometimes, though, imbalances develop that require the heavy hand of the authorities to re-calibrate the scales. Europe’s investment industry is a market sorely in need of intervention.

The European Securities Market Association has just published a 117-page report analyzing the performance and costs of retail products in the European Union. It makes for depressing reading — all the more so given the increasing need for the region’s aging population to put aside sufficient retirement funds to ensure a decent standard of living in its twilight years.

The highlight — or lowlight, if you prefer — is the measure of just how much investors are paying for the privilege of investing in so-called Undertakings for Collective Investments in Transferable Securities, the EU’s 10 trillion-euro ($11.5 trillion) equivalent of the U.S. mutual fund industry. The study shows that between 2015 and 2017 costs eroded returns by an average of 25 percent across different asset classes. Returns on bond funds were so low in 2017 that fees, which haven’t changed much in recent years, absorbed more than half of the gross returns. Those are incredible numbers.

Moreover, ESMA said it found “high heterogeneity in costs across member states,” suggesting that the passport system that allows firms to sell investment products across the bloc’s national boundaries isn’t resulting in the sorts of competitive pressures that would bring fees down.

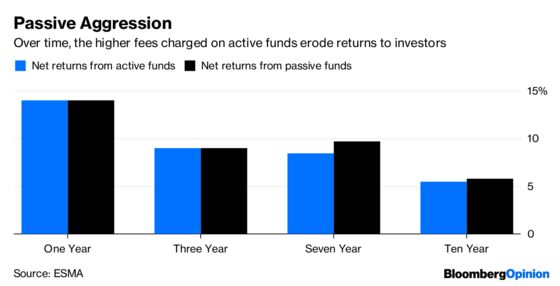

The study also provides more ammunition, if it were needed, for the cheerleaders of low-cost index tracking products. On a one- to three-year horizon through 2017, ESMA reckons that the higher gross returns generated by actively managed funds were so reduced by their higher fees that their net performance that of matched passive strategies. Over the longer term, those elevated fees cost investors.

Unsurprisingly, costs are higher for retail buyers than institutional investors. ESMA estimates individual investors pay 1.9 percentage points in fees for equity funds compared with about 1 point levied on institutional clients, while for fixed-income products the retail premium is more than half a point.

Perhaps more worryingly, those gaps persist across all of the time horizons measured by the agency, ranging from one year to a decade. That shows fund providers haven’t cut their costs as governments and employers force employees to take more personal responsibility for their pension provision.

And that matters. Part of the European Commission’s drive to create an integrated Capital Markets Union is to encourage individual investors to shift their savings from bank accounts and into stocks, bonds and other securities to “meet the challenges posed by population ageing and low interest rates,” as ESMA puts it.

So what is to be done? ESMA isn’t, and shouldn’t be, in the business of imposing caps on how much investment managers charge for their services. But it can insist that the firms it oversees do a better job of being transparent about their fees, which in turn would give investors better information when making their selections. Smith’s invisible hand could then do a better job in helping money flow to the most cost-effective solutions.

ESMA notes that its study was impaired by “the unavailability of important cost data elements” including distribution and transaction costs and performance fees, as well as a lack of common reporting across the different EU countries.

If the market regulator can’t get to the bottom of fee numbers — the biggest factor investors can control when choosing where to put their money — what hope is there for Joe and Josephine Average trying to save for retirement?

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.