Will Slow-and-Steady Europe Win the Economic Recovery Race?

(Bloomberg Opinion) -- So far this year, the pandemic recovery limelight has been hogged by the U.S., and to some degree even the U.K. But move over you two English-speaking economies! It might be time for the European tortoise to catch up with the hares.

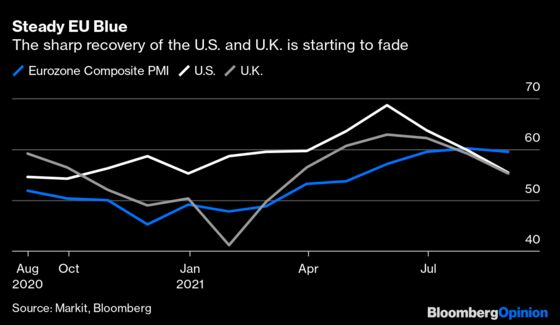

Purchasing managers surveys are probably the best real-time snapshots into to how an economy is faring. While reading across the indexes produces a far from exact picture, it does provide a decent guide to the direction of travel. Those released Monday for major developed countries — on a preliminary basis for August — showed a notable swing between the solid growth of the euro area (despite a blip lower in German manufacturing) and the fading stars of the both the American and British economic recoveries. The service sectors of both of the latter took a nasty tumble this month due to shortages of staff and widespread logistics issues. The sugar rush of major fiscal stimulus could be wearing off fast.

Europe is holding its own for interesting reasons. First, though the European Union’s vaccine program suffered from a troublesome start, it has recovered strongly and major progress has been achieved, allowing the wider economy to reopen. Second, the long-awaited 800 billion-euro ($940 billion) NextGenerationEU recovery fund is just starting to kick in with multi-billion grants transferred to the countries most in need. Italy received its first slug of 25 billion euros in mid-August. Third, due to the relentless strength of the dollar, the export-focused euro-area economy has won some respite for recovery to properly take hold without the headwind of an overly-strong currency.

There is another factor as well: What happens if the Fed grasps the nettle and starts tapering its vast QE bond-buying program this year only to trigger another taper tantrum. We may find out more at the Federal Reserve's annual Jackson Hole symposium this week — or not. But with Europe being significantly behind in its pandemic recovery — and being in a much weaker state going into the crisis with several countries on the verge of recession — the risks of stimulus being withdrawn prematurely are much more acute.

Yet European Central Bank President Christine Lagarde has moved swiftly to immunize the bloc as much as practically possible against these risks. Earlier this summer, she instituted a comprehensive review of the ECB’s monetary arsenal and a simplification of its 2% inflation target. This will afford the governing council a lot more flexibility to roll with the the punches if conditions become adverse again. Its Sept. 9 meeting will no doubt see some lively commentary from hawkish members but they remain in a minority.

With the Pandemic Emergency Purchase Program due to expire in March, there needs to be a contingency plan to ensure a smooth transition to the pre-existing Asset Purchase Program. The PEPP's flexibility — in size and ability to buy less restricted amounts of an individual country’s debt — will need to be morphed into its replacement. But Lagarde, and the Chief Economist Philip Lane, have ensured that monetary stimulus is plentiful and sufficient for the duration. This will in turn smooth the way for the NextGenEU fiscal ammunition to garner more traction and propel the recovery forward.

It is clear some of the wind has come out of the stateside recovery. Analysts at Goldman Sachs Group Inc. have revised downward U.S. third-quarter growth estimates, to 5.5% from 9%. The full year forecast has been trimmed from 6.4% to 6%; the 2022 estimate has been only marginally raised. A similar pattern is being seen in the U.K. where 4.8% second-quarter growth is likely to fall to around half that this quarter; second-half growth could disappoint further.

But European estimates are likely to be revised modestly higher, as the monthly Bloomberg survey of 50 European economists shows. The EU Commission in July revised up its expectation for growth this year to 4.8% and 4.4% for 2022, though these might also be further revised in coming months. Albeit the usual engine for European growth — German manufacturing — is struggling along with the rest of the industrial world from chip shortages and a slowdown in demand in China.

European equities are closely tracking U.S. gains this year for good reason; they are also strongly outperforming both U.K. and Asian stock markets. There is plenty of life left in the euro area’s recovery. Don’t write off the tortoise.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.