(Bloomberg Opinion) -- The big difference between the European Central Bank and the U.S. Federal Reserve’s pandemic recovery efforts has been their respective approaches to the high-yield bond market.

The ECB has barely dipped a toe in the sub-investment grade waters, limiting itself to some modest collateral help for firms that slipped into BB ratings because of the crisis. That’s in marked contrast to the Fed’s splashy foray into buying junk debt for the first time, mostly via exchange-traded funds.

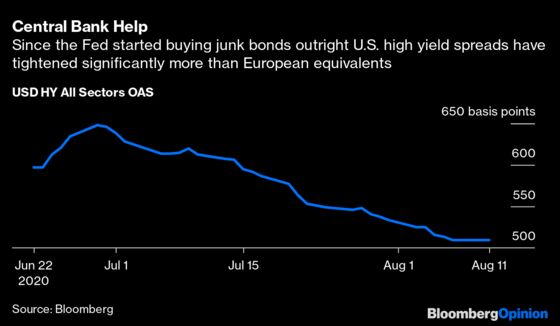

So it’s unsurprising that U.S. high-yield spreads (the difference between interest rates on junk bonds and their benchmarks) are tightening much faster than Europe’s. Some new American records are being set, such as the sub-3% coupon achieved by Ball Corp. on Monday for a 10-year sale. That’s the lowest yield recorded for a U.S. junk bond of that maturity.

The worry for Europe’s policy makers is that junk-rated companies are often an important part of the economy, employing lots of people, so their health is important. Fortunately, the continent’s high-yield market is functioning well for now, but it will need to be monitored as we move into the next stage of a fragile economic recovery.

At least the European Central Bank has left itself some room to help out sub-investment grade businesses if that becomes necessary, although the Fed is in a better position because it has that tool available already.

There are technical reasons too for the difference in the U.S. and European approaches to high-yield debt, and the recent American outperformance. This type of credit is less common in Europe; it’s equivalent to less than a fifth of the investment-grade corporate debt in circulation. In the U.S., many junk bond issuers have stock listings too, making them more visible — and arguably more important — to policy makers. In Europe, private-equity vehicles dominate the market.

The European market also tends to be concentrated at the higher-quality end of the junk ratings, with the bulk of outstanding euro supply in the BB bucket. Generally there’s a higher hurdle to attract sufficient investor demand. As such, default rates remain low, although the full effect of the pandemic has yet to play out as labor support schemes and access to cheap capital are still freely available.

European supply has returned pretty strongly of late. There have been 100 new high-yield deals in Europe worth about 50 billion euros ($59 billion), some 20% higher than at this point last year. Nonetheless, that’s dwarfed by investment-grade company issuance of 300 billion euros, more than 50% higher than last year.

Americas’s junk market is significantly wider and deeper, with a raft of issuers in the lowest rated CCC segment. This mix of higher and lower risk means the U.S. junk index will suffer more in times of stress but snap back quicker.

The Fed’s backing of high-yield companies highlights their importance to the U.S. Economy. The ECB isn’t dealing with as big a beast, but this corner of the market is still systemically important, even if many of these companies are in private-equity hands. Looking at the economic carnage around Europe, we’re not done yet with extraordinary central bank support. At some point that may have to include junk.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.