(Bloomberg Opinion) -- The remorseless strength of the U.S. dollar as the global haven is starting to cause problems — and not just in emerging markets. Japan and Europe have traditionally preferred to have their currencies run a little weak to the dollar to boost exports. But the slide this time is worrisome. The yen has fallen to its weakest levels in two decades, testing the Bank of Japan's resolve in maintaining a lid on bond yields. The eurozone, however, is where the most discomfort is felt because it is exacerbating inflation, in part because imports become more expensive. The common currency anchors the European Project so a precipitous drop risks becoming existential for continental unity in a way that yen weakness doesn’t.

The euro has declined steadily for the past year from above 1.22 per dollar to within close range of the 1.0640 low of March 2020, when the pandemic first hit. A test of parity to the dollar later this year is no longer a low-probability risk. A currency crisis of confidence is the last thing the European Central Bank needs. It already faces an almost impossible choice between counteracting soaring imported inflation or risking a renewed recession. But doing nothing is rapidly ceasing to be an option.

Imported inflation is exacerbated by the war in Ukraine because much of Europe’s energy purchases are priced in dollars. A weaker euro just magnifies the short-term problem. It is a reverse of the situation for most of this century when an arguably underpriced common currency drove exports to China and Russia. Those trade partners are either slammed shut or suffering their own economic downturn. It doesn't help when the U.S. Federal Reserve seems to be on a mission to raise interest rates at the fastest pace in decades to combat its own inflation surge. The differential to negative rates in Europe is glaring.

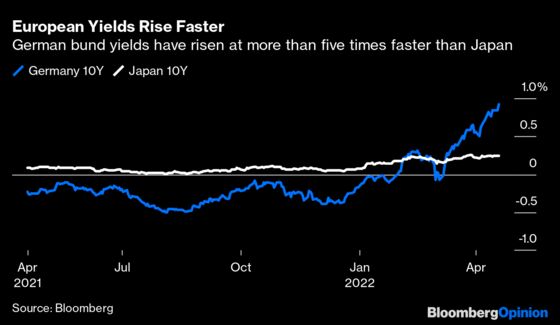

The only logical answer is for the ECB to raise its official deposit rate from the current super-stimulatory negative 50 basis points. But it must also ever-so-carefully keep financial conditions lax via other monetary tools, such as bank lending incentives. While bond yields have moved multiple times higher in Europe than in Japan, the ECB has not yet offered any meaningful support for the euro. Something's got to give and the first step is to stop its QE bond-buying programs by early summer and pave the way for the first rate hike in September.

Unfortunately, at last week's Governing Council meeting, it chose to do essentially nothing except buy time until the next quarterly economic review on June 9. The press conference guidance from President Christine Lagarde focused on long-tern inflation expectations remaining below its official inflation target of 2%. The council didn’t even discuss the currency (though Lagarde said she and her colleagues were “attentive” to it, whatever that means). The market could tell the ECB was avoiding the problem, hence the renewed weakness in the euro.

Perhaps the ECB will get away with it. But let’s be honest here: Postponing rate hikes often precipitates a deeper crisis. The weak link in the chain is no longer the peripheral bond spreads of countries like Italy or Greece to the European bellwether of Germany. It is the euro itself. Lagarde speaks twice this week and needs to provide clarity about the timetable for reversing the over-generous pandemic stimulus that is contributing to the surge in inflation. A 7.5% annual CPI rate in March requires action, not lame epithets that the Governing Council will act if necessary. When will it know things are broken? With double-digit inflation?

Europe has, so far, been fortunate. The current presidential contest between Emmanuel Macron and Marine Le Pen has not affected markets the same way it did during their first face-off in 2017, when there was a sharp rise in French bond yields. There have also been no sharply rising wage demands yet. But the ECB cannot dilly-dally hoping for divine providence. As the Fed and Bank of England have realized, unless the monetary-policy response is quick and aggressive, markets lose confidence rapidly. This is a risk the ECB can no longer take. It has to raise rates this year and telegraph its expected actions clearly. Otherwise, its already entrenched problems will worsen.

More From Bloomberg Opinion:

-

Zero Is a Good Destination for ECB Interest Rates: Marcus Ashworth and Mark Gilbert

-

Elevated Inflation Settles In for the Long Run: Jonathan Levin

- Dethroning King Dollar Won’t Be an Easy Feat: Robert Burgess

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2022 Bloomberg L.P.