(Bloomberg Opinion) -- EOG Resources Inc. delivered something of an antidote to the venom that coursed through the fracker stocks Wednesday. Another darling of the sector, Diamondback Energy Inc., had sickened investors with a shock miss on production, adding to the growing chorus of voices announcing shale’s imminent demise (while oil prices also fell on trade fears). EOG’s combination of soundly beating production guidance with lower-than-expected spending, released Wednesday evening, was like a calming tumbler of whiskey at the end of a grueling day.

Or grueling earnings season; EOG’s call marks the end of quarterly numbers for the biggest exploration and production numbers, and investors will mostly be glad to see the back of them. Chesapeake Energy Corp.’s slump below a buck a share was an extreme example — albeit with a certain fin-de-siècle frisson — but the problems of high leverage and too much spending remain endemic across the sector.

EOG stands out for bucking that trend. And though it seems churlish to say, it could quite easily stand out even more.

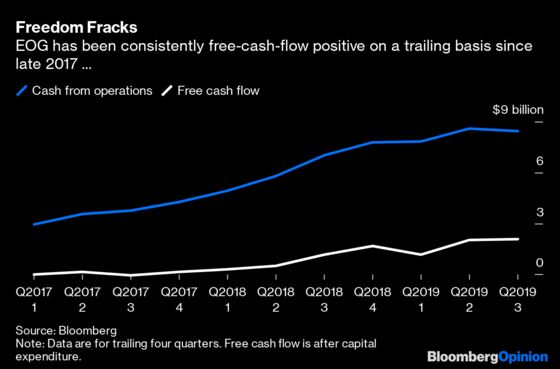

EOG has cracked the formula for pleasing a cohort of energy investors who are increasingly ornery (if they even bother to show up, that is): steady growth twinned with free cash flow and low leverage. Higher productivity, generated by in-house improvements rather than just squeezing suppliers, according to the company, means EOG has dropped its average rig-count target from the year from 40 to 36. Net debt to Ebitda has dropped from an already conservative 0.7 times a year ago to just 0.5 times at the end of the third quarter. Little wonder EOG’s benchmark 2023 bonds have rallied by more than 5% this year.

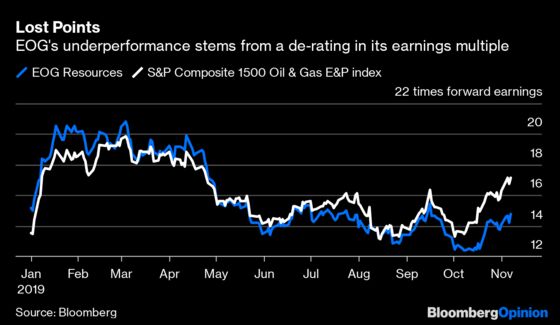

That stands in marked contrast to the stock, which, even after Thursday morning’s 5% bump, is down 13%. Weak oil prices and broader revulsion to any company producing the stuff explains some of that, of course. But EOG has lagged a falling sector as its earnings multiple has dropped a couple of points.

With others suffering — Diamondback’s multiple has slumped to less than 9 times — investors may be worried about EOG making a big acquisition, which hasn’t exactly been the path to prosperity in the sector. EOG went out of its way on Thursday morning to dispel such notions. Another risk that has surfaced of late, that a Democratic president might restrict fracking on federal lands, also prompted EOG to add a couple of slides to its presentation. Given the number of moving parts, not least exactly how much a president antipathetic to fracking could actually do, this seems a minimal risk for now.

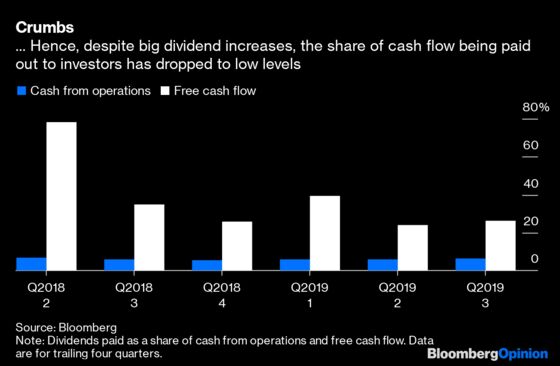

One way to address it all at a stroke would be to bump up EOG’s dividend substantially. The company has been raising payouts at a fair clip already, up more than 70% over the past two years. But the actual amounts are pretty small, with EOG paying out just $166 million in the third quarter, equivalent to just 8% of cash from operations and about 29% of free cash flow after capital expenditure. On a trailing four-quarter basis, the proportions are even lower.

EOG’s stock now yields about 1.5%, and the company targets 2%, which would take it slightly above the S&P 500. That’s a significant level to beat given the E&P sector’s history of benchmarking by navel gazing, judging its own performance against the weaknesses of peers.

Getting there wouldn’t actually cost that much: an extra $200 million or so, annualized. That would take payouts to 10% of cash flow from operations and 42% of free cash flow. EOG of course doesn’t want to set itself up for a potential cut down the road if oil prices drop, perhaps as early as next year. But low leverage and the wide cushion of free cash flow above and beyond dividend payments provide a significant buffer already.

Moreover, EOG spent much of Thursday morning, as it does every quarter, playing up the low breakeven prices of its drilling inventory, providing resilience to the inevitable swings in commodity prices. A relatively small increase to the dividend bill would go a long way in backing that up, and closing the valuation gap.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.