(Bloomberg Opinion) -- Utilities are, by design, a bit of a snooze. We feel no excitement at the miracle of instantaneous light, television and coffee grinding, expecting these things simply to happen when we want them to – which, virtually all the time, they do. Similarly, investors own utilities for their steady dividends funded by all of us unthinking bill-payers. This mundane arrangement has fed widows and orphans for decades.

Oil, on the other hand, is wild; a never-ending dance of discoveries, disappointments, Viennese jamborees, wars, trade, presidential tweets and palace intrigues. At times, we really have worried about the pumps running dry. Fortunes and whole economies are lost when prices crash, but the allure of the next killing has been impossible for more adventurous investors to resist.

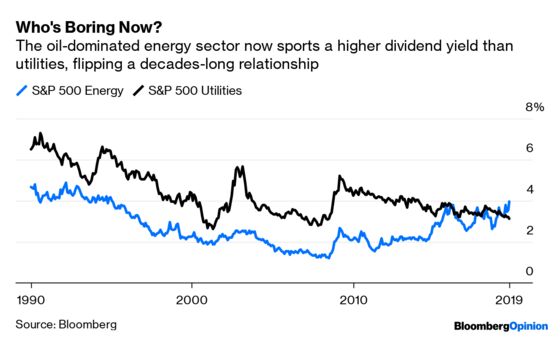

All of which makes this chart quite interesting:

This isn’t the first time the oil-heavy S&P 500 Energy index has offered a higher dividend yield than utilities (that was in August 2015). But we’ve now had almost four months of this situation, by far the longest run, and the spread has widened. After almost three decades of utilities offering roughly 1 to 3 percentage points of extra yield compared to their oilier energy brethren, the script seems to have flipped.

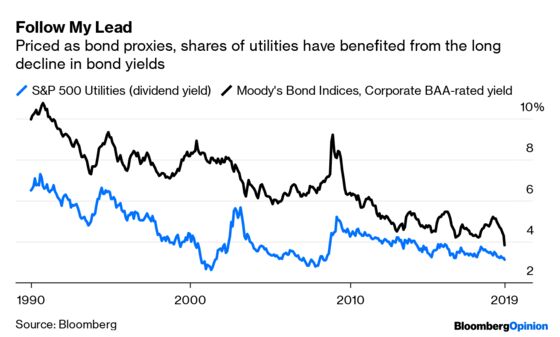

One explanation for this is, as you might expect with utilities, rather prosaic. Valued as bond proxies, they have been towed along more than most by the bull market in debt. Current economic fears help, too.

There is also a potentially more interesting interpretation to consider here: What was growth is now viewed as value, and vice versa.

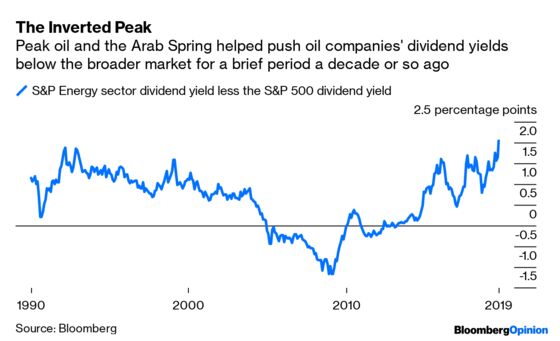

The first decade of this century was dominated by China’s commodity-hungry growth spurt and fears of peak oil supply. The oil business was spewing cash, but also investing a lot of it in new fields. After the brief buzzkill of the financial crisis, the Arab Spring pushed oil back into triple digits, making this seem like the new normal and spurring yet more drilling, including in U.S. shale. This was a time when you owned oil stocks for growth and were OK with cash flow going into the ground rather than your pocket. Hence, it is also the only time in several decades when the energy sector’s dividend yield dipped below that of the S&P 500.

That all changed with the oil crash beginning in late 2014. Investors woke up to the reality that the world was awash with oil and the industry’s investment binge had trashed return on capital. Meanwhile, growing awareness of climate change and the appearance of actually desirable electric vehicles flipped fear of peak oil supply to speculation about peak demand. The other sea change is protectionism, putting a damper on economic growth and a question mark over the future of global supply chains, including those for traded energy.

“The bottom line is that the market appears to be saying that value propositions are not competitive with other sectors and until they are, energy may have a hard time finding a bottom,” says Doug Terreson, analyst at Evercore ISI.

Utilities, meanwhile, continue to enjoy reasonably steady earnings growth. While U.S. electricity demand has flatlined, demand doesn’t drive earnings for regulated utilities; investment in old grids (including for natural gas) does, and that has kept on going. In other words, a utility with ever-expanding capital expenditures rewards investors regardless of demand for electrons. The same cannot be said for oil and gas spending.

Importantly, electricity’s expanding share of energy demand, and especially the rise of renewable power, give this old value sector a more credible growth story. We’re talking more like 4% or 5% per year rather than the double-digits touted by frackers. But the latter narrative has worn thin and the utilities’ targets look more dependable.

Since 2000, global electricity consumption has been rising about two-thirds faster than overall energy consumption and it now competes (at the margin) in oil’s chief market, transportation. Investment in power infrastructure is now higher than for oil and gas, having overtaken it in 2016, according to the International Energy Agency. There’s a reason Royal Dutch Shell Plc, among other majors, is dipping a toe or two into the current, including this week’s bid for Australian electricity retailer ERM Power Ltd. As Maarten Wetselaar, who runs Shell’s integrated gas and new energies business, put it earlier this year:

We are not interested in the power business because we like what we saw in the last 20 years; we are interested because we think we like what we see in the next 20 years.

The upshot is that money has moved into utilities, attracted by the dividends, yes, but also the promise of growth. With their own growth narrative having ebbed, oil and gas producers must pay investors to hold their stocks.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

Nathaniel Bullard is a BloombergNEF energy analyst, covering technology and business model innovation and system-wide resource transitions.

©2019 Bloomberg L.P.