(Bloomberg Opinion) -- At last we have at least a partial explanation for why Tesla Inc.’s stock gained 500% this year: Massive bets on high-flying technology shares by SoftBank Group Corp. and others using equity derivatives. The extraordinary rise valued Elon Musk’s electric car business at $464 billion at the peak in late August, when only six U.S. companies were worth more.

Unfortunately for Tesla’s devoted followers and the retail investors who’ve been giddily tallying up their winnings, the surge in the market value has very little to do with it selling more vehicles.

Rather, it’s partly a tale of plain old financial speculation. If that feverish sentiment cools suddenly, it could leave the stock vulnerable to another sell-off. Tesla shares have tumbled 16% since the start of September, incinerating $75 billion of paper gains, and they fell about 15% in pre-market trading on Tuesday after the company wasn’t added to the S&P 500 index. The news that General Motors Co. has taken a $2 billion equity stake in Tesla rival Nikola Corp. won’t have helped.

Not everyone accepts the argument that SoftBank’s huge derivatives bets have by themselves powered the epic run-up in technology stocks, including Tesla, as the Financial Times reported last week. But it’s certainly plausible that speculative purchases of call options — which give investors the right to buy a stock for specified price — by a much larger cohort of retail and other investors played a part in the rally.

When brokers sell short-dated call options they often need to hedge their exposure by buying the underlying stock. You can see how a cycle of rising prices might then become self-perpetuating.

Call-option buying has been buoyant lately and volumes in Tesla stock trading have been astounding — almost $65 billion of its shares changed hands on just one day in mid-July, according to Bloomberg data. Tesla’s recent five-for-one stock split seemed purpose-built to encourage more buying by making the nominal cost of the shares cheaper. The shares gained about 80% following the announcement in early August.

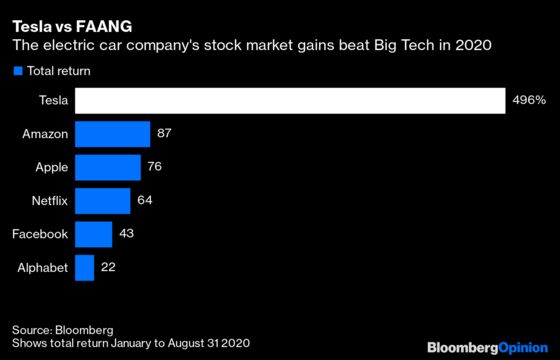

The stock’s gains were much larger than most large tech companies’ (see chart below), and they also defied simple explanation. Unlike Amazon.com Inc., say, Tesla hasn’t derived a material benefit from the pandemic. On the contrary, its California car plant had to shut for a while.

And while some investors see large-cap tech stocks like Alphabet Inc. — with their massive cash flows and entrenched market positions — as ports in a storm, Tesla doesn’t match that description either.

If you strip out the benefit from selling regulatory pollution credits to rival manufacturers, Tesla’s car business remains loss-making and it’s facing mounting competition as the industry’s giants start mass-producing their own electric vehicles.

In fairness, Tesla has built a compelling brand and the car’s features and automated driving functions get better the longer you own it. It has also improved its manufacturing. A new Shanghai plant was up and running in no time.

Meanwhile, the $5 billion stock sale that Tesla announced last week will help pay for its spending plans, which include new factories in Germany and Texas, and provides a safety net in case of any financial mishaps. The company’s inflated valuation means issuing all those shares will barely dilute shareholders.

While Tesla has shown repeatedly that it can raise massive sums of money, it’s yet to prove it can generate decent returns on that capital.

The current $390 billion market capitalization — four times that of Volkswagen AG, the world’s largest carmaker — is still impossible to justify with any normal metric. Most analysts are bullish on large tech companies but they’re tepid on Tesla. The average price target implies the shares will fall more than 30%.

Wall Street analysts have been consistently wrong this year, but even Musk thinks Tesla’s stock price is “too high”. His Twitter intervention came in May when the market capitalization was less than 40% of what it is now.

Ideally, Tesla would gradually ease into its oversized valuation by delivering much higher revenues, earnings and cash flow in the coming years. However, speculative bubbles have a habit of deflating suddenly, particularly if there’s unexpected bad news. Tesla investors had been looking forward to its inclusion in the S&P 500, which was expected to trigger yet more buying of the stock by index-tracking funds. But Tesla is strangely absent from the new list.

Back in the real world, it’s getting harder to ignore the onslaught of new rival electric cars hitting the market. That might explain why Tesla’s revenue growth has been so unimpressive lately.

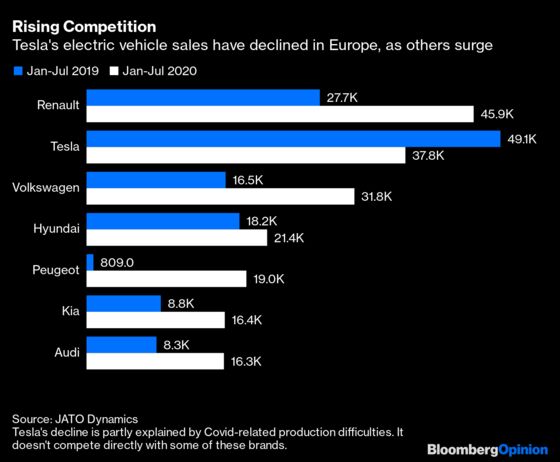

The competition is most evident in Europe, where tough regulation has forced incumbents to clean up their act. Tesla’s European sales and market share have declined this year, and that’s before the launch of several keenly priced electric SUVs from Volkswagen. The VW group will probably pass Tesla to become the world’s largest electric car maker in a couple of years.

Musk is a master of sustaining hype, either by announcing new product categories such as the Cybertruck pick-up and the Semi heavy truck, or teasing new technologies like fully automated driving. And yet, the company’s current automated driving capabilities have received mixed reviews.

Tesla’s battery-technology day later this month can probably be relied upon to deliver a required booster shot of investor excitement. But to sustain the nosebleed share price, Musk will need to be on top form.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2020 Bloomberg L.P.