(Bloomberg Opinion) -- Elliott Management Corp. is resuming confrontational activism in Germany, potentially reviving fears that “locust” funds are back and up to no good. Investors are probably being too skeptical that Elliott will be able to force positive change.

The activist hedge fund has lambasted managers at Scout24 AG, a Frankfurt-listed online real estate and car classifieds business capitalized at 5.4 billion euros ($6 billion). They are a soft target. The company’s board backed a cheap bid from Scout24’s former private-equity owners in February, only to see shareholders resoundingly reject the offer in May. The debacle has exposed the group to the broader attack that bad management is the reason for the share price weakness which triggered the attempted takeover.

Elliott has had some Teutonic success through behind-the-scenes activism with SAP SE and Bayer AG. Here, it’s publicly calling for a break-up and much more aggressive leverage, accusing management of a “shocking lack of ambition” that has left the shares trading at a near 25% discount to an estimated fair value of 65 euros share.

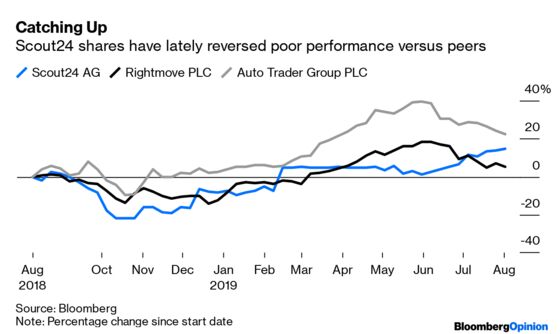

The market isn’t so sure. Scout24’s shares barely moved in response. It’s not hard to see why. To get to this higher value would require an uplift in operating performance. Scout24 already trades on 19 times expected Ebitda, nestling between real estate and auto peers Rightmove Plc and AutoTrader Group Plc. That feels about right given it’s a hybrid of the two. To be worth substantially more, the company will have to lift revenue and margins while maintaining its valuation multiple. That probably means raising prices.

Suppose Scout24 could lift Ebitda from the 321 million euros expected this year to 375 million euros, a 17% jump, and nudge its valuation multiple a little higher to 20 times. That would imply an enterprise value of around 7.5 billion euros. Deduct net debt and the equity would be worth 6.8 billion euros, or 63 euros a share. Increase leverage via a buyback and Elliott’s share price target isn’t far off.

It’s easier said than done. Elliott reckons a sale or demerger of the auto arm would help speed things along. Not only would it likely fetch a full price if there were competing bids, but Scout24 management could focus on lifting the performance of the real estate business. Perhaps.

The danger is that Elliott has made change harder to achieve by blatantly telling the board what to do. The forthcoming annual meeting will see three new directors nominated. That provides a chance for Elliott to put forward an alternative slate. But suspicions have lingered around hedge funds and private equity in Germany ever since 2005, when politician Franz Muntefering described them as “swarms of locusts” that devour companies and destroy jobs. Elliott’s approach may be friendly to other shareholders, but the firm will need to tread carefully if it ups the pressure.

The best hope is that a bidder now surfaces with an offer for the auto business that management can’t refuse. That would give Scout24 management a pretext to re-think leverage levels for what remains and adopt much of Elliott’s thinking without it looking that way. But whether that happens is not in Elliott’s hands.

To contact the editor responsible for this story: Stephanie Baker at stebaker@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.