Elliott and Blackstone Enter Hostile Territory in Japan

(Bloomberg Opinion) -- A small $1.5 billion company is attracting the biggest movers in finance in what’s shaping up as the first high-profile foreign hostile takeover in Japan. If successful, it could wake up the sleepy $228 billion market of publicly listed real-estate companies.

The attention is on Unizo Holdings Co., until recently an obscure developer and hotel operator. The company has a big chunk of its office rental business, which accounts for about 90% of operating income, in Tokyo, where the vacancy rate is as low as 2% and a decent 3.5% yield can be earned.

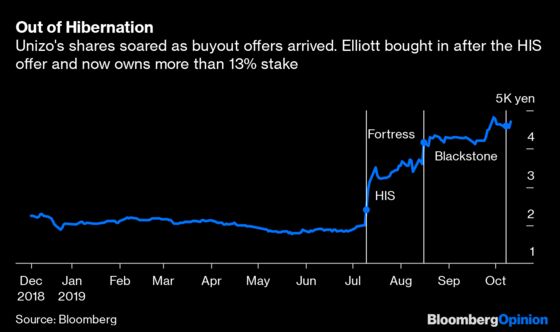

The developer’s stock came alive in July following an unsolicited tender offer from Japan’s leading travel agency, HIS Co. Unizo looked for white knights to come to its rescue. Two appeared: Fortress Investment Group, a subsidiary of SoftBank Group Corp. that has invested about $100 billion in real-estate deals worldwide; and private-equity giant Blackstone Group Inc., which came in with a 25% premium to the Fortress bid.

Meanwhile, perhaps smelling a good event-driven trade, Paul Singer’s Elliott Management Corp. began buying Unizo shares; the activist hedge fund is now the largest shareholder and has a stake of more than 13%. With all this activity, Unizo’s stock has soared 128%, and short-sellers have started circling.

But Unizo may have only been playing for breathing room. Its board of directors has gone from full support of the would-be rescue to demanding extra terms. Embedded in the Fortress offer in mid-August, for example, is an understanding that employees would have discretion over how Unizo is run in the first two years but Fortress would take full control afterward. In late September, though, management decided that employees – not shareholders – would be the ultimate bosses.

Under that acquisition guideline, a new owner will not be able to restructure or dissolve Unizo without the consent of employees. They will also determine the method of the fund’s exit – whether via buybacks, strategic sales or re-listing on the Tokyo Stock Exchange. Considering that restructuring is private equity’s bread and butter, it’s hard to see how any fund would be willing to agree to such terms.

Elliott has taken its disappointment public. In its first open letter to management in Japan, the hedge fund asked pointedly why Unizo had such a change of heart. This marked a departure from the polite approach taken by foreign activist shareholders that has seemed to get things done in Japan.

Elliott has spent about 16 billion yen ($148 million) for an average price of 3,654 yen per share on the Tokyo Stock Exchange, and will have to carry the paper loss for months if both the Fortress and Blackstone deals fall through. It may not be able to call an extraordinary general meeting until January, according to Travis Lundy, a special situations analyst who publishes on Smartkarma.

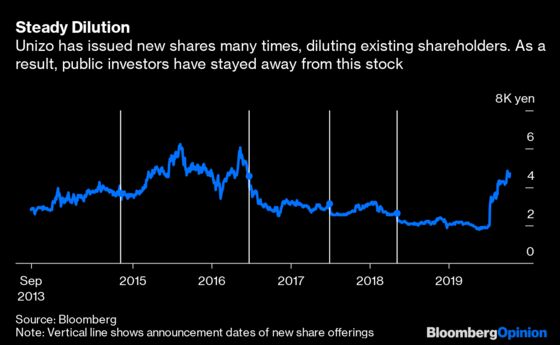

Fortress has extended its offer to expire Thursday. If the foreigners stay in the game for control of Unizo, they could be in for a tough fight. They’re confronting a stubborn Japanese company so keen on independence that it doesn’t mind diluting its shareholders many times over. Originally an affiliate of Mizuho Financial Group Inc., Unizo issued new shares – annually, in recent years – to distance itself from the megabank. In 2011, Kyoritsu Co., an insurer affiliated with Mizuho, was Unizo’s largest owner with an 11.8% stake; by March, it was down to 4.3%.

Unizo’s value is of the hidden-gem variety. With a net debt-to-Ebitda ratio of 14.7 times, it’s already heavily indebted, meaning the usual private-equity tactic of piling on debt to engineer returns won’t work. It’s trading at 1.4 times book value, not cheap by Japanese standards.

But under Japan’s accounting rules, developers don’t record the rise and fall of the value of their land banks or buildings. As a result, Unizo’s net asset value, once we account for a valuation gain of 220 billion yen suggested by management, would come to 7,857 yen per share. That’s more than twice the book value and makes even Blackstone’s offer look like a great deal – but only if Unizo allows the funds to divest assets and pay off debt.

Prime Minister Shinzo Abe has nudged Japan Inc. to improve shareholder returns since 2013, but enthusiasm for better corporate governance has evaporated over the last year. Japan has hundreds of listed real-estate companies with hidden gems and weak valuations. Billions can be unleashed from asset spin-offs.

The time for politeness may be over.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.