(Bloomberg Opinion) -- Any takers for a couple of big stakes in an old-style, carbon-emitting power generator?

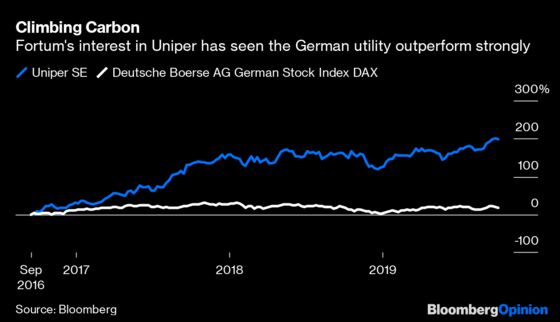

Germany’s Uniper SE is not a business that fits with the times. Yet hedge funds Elliott Management Corp. and Knight Vinke have just succeeded in squeezing a high price from the one keen buyer of their combined 21% holding, the Finnish utility Fortum Oyj.

Investors sitting on the other 30% not already owned by Fortum can only look on in dismay and ask how they missed out.

Fortum made a takeover bid for Uniper in 2017 but had to settle for a stake just below 50% after it emerged that Moscow had an effective veto on it gaining control (the German company owns a water facility in Russia and Fortum is controlled by the Finnish state, hence Russia’s right to block the deal).

All of a sudden, something has changed. Fortum sees a potential path to Russian approval, although it won’t say precisely what it is. The Finnish company has agreed therefore to pay 2.3 billion euros ($2.5 billion) for the position held by Elliott and Knight Vinke. That would give it a 71% stake, assuming Russia’s approval is forthcoming.

For Elliott, it’s a classic short-term win from opportunistically buying into a bid target. For Knight Vinke, it’s the profitable culmination of a longstanding activist campaign that began with nudging the German power giant E.ON SE to carve out Uniper in a demerger three years ago.

As for Fortum, it’s a victory of sorts in a war of attrition with Uniper’s management. The Finns look set to gain de facto control. Key shareholder votes in German companies require 75% approval and Fortum would almost certainly clear that hurdle, gaining the power to appoint directors to Uniper’s supervisory board, who in turn oversee the management board. True, Fortum can’t fully integrate the German business into its own company. But it will get to direct Uniper’s strategy and receive dividend payments to cover the cost of its stake.

There’s nothing here for Uniper minority investors, though. They were hoping to get a fresh takeover offer from Fortum, made available to all shareholders. Either that or a so-called “domination agreement” whereby Fortum got full access to Uniper’s cash flow in return for paying minority shareholders a chunky dividend. Fortum says it has no plans to make a fresh bid and won’t seek a domination agreement for at least two years. Why would it?

It would have been better if Uniper had extracted some sort of agreed deal with Fortum. The German target appears to have relied on the Russian water asset being a poison pill. Fortum seems to have found a way around that. But with Fortum having a blocking stake and the hedge funds agitating for an exit, negotiating a grand bargain between all the stakeholders would have been the best way forward for Uniper.

Minority investors are always in a tough spot when the register includes other big beasts, especially when one is a strategic bidder and another is Elliott. The episode is a reminder that sometimes their interests are best served by management not fighting too hard.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.