Elizabeth Warren’s Wrong Answer to the Wells Fargo Problem

(Bloomberg Opinion) -- Elizabeth Warren wants the Federal Reserve to break up Wells Fargo & Co. That is sort of funny and silly in equal measure.

The U.S. senator wrote to Fed Chair Jerome Powell to demand that Wells Fargo ditch its investment bank so management could focus solely on fixing the problems in its main street business. The latter is the division that’s led to more than $5 billion in fines and settlements over the past five years.

The industry joke is that Wells Fargo is possibly the only institution where the reputation of the Wall Street business was dragged down by the main street side — though, of course, there is nothing funny about the harm to customers from the fake accounts and other scandals that began to emerge in late 2016.

The cure being suggested by Warren is silly because forcing the bank’s management to deal with the costs and complexities of splitting up a major financial institution would be a huge distraction from the rehabilitation that Wells Fargo must put itself through. The task would be a bigger headache for its top management team than trying to win new business advising companies on deals and capital raising, the activities that concern Warren the most.

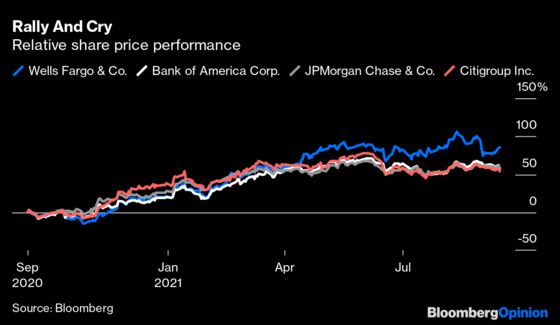

This is not to make light of the problems at Wells Fargo. It was fined another $250 million last week for a lack of progress in fixing problems related to its mortgage division. At the end of August, when the likelihood of more fines was first reported, its stock price tumbled 11%. Over the past year, Wells Fargo shares have rallied more than those of JPMorgan Chase & Co. and Bank of America Corp., but it remains far behind in terms of valuation.

For Warren, this intervention is consistent with her campaign to reinstate something like the Glass-Steagall Act that once kept investment and commercial banking apart. She’s also been blasting Powell over financial regulation before the White House has to decide whether he remains Fed chair after his term expires in February. Warren says Powell’s too soft and too close to Wall Street.

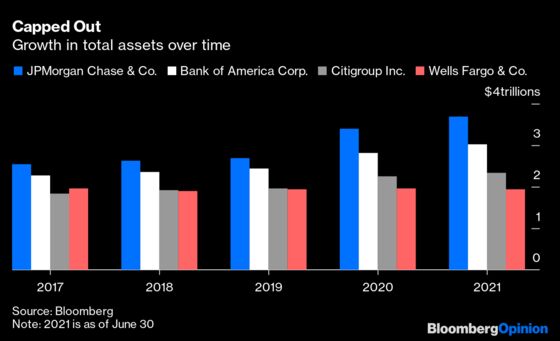

It is extremely unlikely that the Fed will heed the senator’s break-up call. But her intervention could still be a pain for Wells Fargo. It will make Powell and his colleagues even more wary of granting the bank an early reprieve from the asset cap of $1.95 trillion imposed in 2018 restricting the bank’s growth while it sorts out the shortcomings that led to the scandals.

Charlie Scharf, chief executive officer since late 2019, has said in recent earnings calls that the cap has hurt revenues because the bank has had to prioritize assets in the consumer and commercial bank over the investment bank. Trading assets in the latter shrank almost 17% between the end of 2019 and the middle of this year. Executives had privately hoped that the Fed might remove the restraint later this year; Fed officials saw it remaining until next year or beyond. The bank has declined comment.

Whether you want to rebuild Glass-Steagall’s walls or not, Warren’s reasoning makes no sense. Forcing America’s fourth-biggest bank by assets to hive off a significant chunk of its balance sheet would demand a massive amount of time for legal, regulatory, technical and financial disentangling.

If, as Warren suggests, management distraction is the obstacle to reforming Wells Fargo, then a major restructuring can't possibly be the solution.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for The Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.