Draghi Throws Everything But the Kitchen Sink at Europe's Problems

(Bloomberg Opinion) -- Mario Draghi, the European Central Bank’s departing president, delivered a bit of something for everyone on Thursday. As one market wag (Andreas Billmeier at Western Asset) put it, this “wasn’t quite the kitchen sink” but it was “all the other sinks” in the house. Most important, Draghi left plenty of room for maneuver to his successor Christine Lagarde.

A return to open-ended bond buying is a big policy shift by the central bank: Quantitative easing in perpetuity. The euro reacted swiftly by falling below 1.10 to the dollar — although those losses were pared back after the ECB’s governing council declined to discuss whether it would lift the cap on the proportion of a country’s bonds it is allowed to hold (a limit it is already close to hitting).

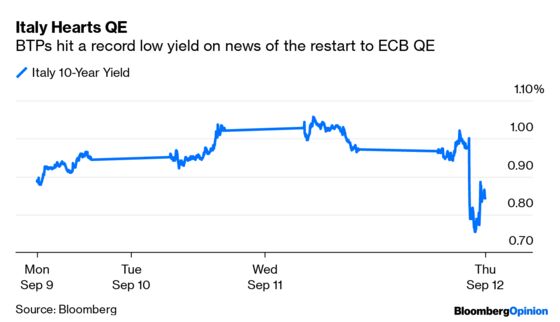

Bond traders loved the announcement nonetheless. Italy was a markets basket case not that long ago, but the country’s 10-year government bonds were the biggest beneficiary of Draghi’s largess, with yields falling 11 basis points to 0.86%.

QE is the perfect weapon to stop the euro from rising and killing off any fledgling European economic recovery (despite Draghi's habitual denial that the ECB targets exchange rates). U.S. President Donald Trump was quick to tweet his fury about the Federal Reserve’s more leisurely approach to monetary policy. Global currency tensions will no doubt get worse as central banks race to cut interest rates so it’s prudent for the ECB to kill off any impression that it’s running out of ammunition.

At what was his penultimate ECB meeting, Draghi gave another master class in keeping the euro project afloat. In the absence of any coordinated fiscal package from euro zone governments, his monetary deftness has been invaluable.

It was a bold move to reintroduce asset purchases barely 10 months after the last round of QE was suspended, especially when the ECB will keep buying until whenever the next president decides to stop.

The purchases can be scaled up too, and a wider range of assets purchased if the economy takes another shift downward. Draghi said economic risks would probably persist as the bank lowered its growth and inflation forecasts for this year and 2020. Note that these uninspiring forecasts are premised on a smooth Brexit. (Try not to laugh).

Similarly, by cutting the benchmark deposit rate by just 10 basis points to minus 0.5%, Draghi has left room to cut again next year. This smaller-than-expected cut was softened by the tiering of the rate charged to commercial banks placing their funds at the ECB, meaning some of their money will be exempt from negative rates.

And there was yet more stimulus in the form of “targeted long-term refinancing operations” (Tltros), which are super-cheap loans for weaker banks. The term available on the loans has been extended to three years and the cost lowered by 20 basis points effectively.

Open-ended QE is the really punchy bit, though, even if the initial amounts were less than some analysts anticipated. If Lagarde can somehow convince Europe’s political leaders to get serious finally on fiscal stimulus, it might even work. Italy is already reaping the benefits. Draghi has given his successor something to work with.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.