ECB Issues a Partial Mea Culpa in Wake of Woodford and H2O

(Bloomberg Opinion) -- In a rare bout of introspection, the European Central Bank has conceded that it’s partly to blame for creating the landscape that led to the misadventures in illiquidity that undid Neil Woodford and prompted investors to pull billions of dollars out of GAM Holding AG and H2O Asset Management. It’s right to be worried about asset managers stocking up on hard-to-trade assets. But people buy them as an alternative to the paltry returns you get from government bond yields, and that backdrop isn’t likely to change anytime soon.

In its latest Financial Stability Review published this week, the ECB acknowledges that the negative interest rates and bond-buying program it’s using to keep the economy afloat are driving fund managers to chase yield by loading up on riskier securities.

“While the low interest-rate environment supports the overall economy, we also note an increase in risk-taking which could, in the medium term, create financial-stability challenges,” the central bank’s vice president, Luis de Guindos, said in a statement accompanying the report.

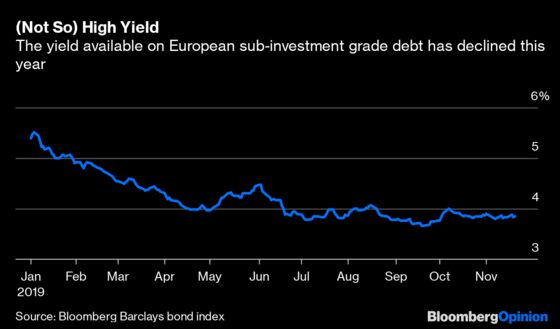

The average yield available on the 325 billion euros ($360 billion) of European corporate debt rated below investment grade has been driven lower this year as investors have allocated more capital to the increasingly misnamed high-yield market.

Sales of leveraged loans and high-yield bonds in the Europe, the Middle East and Africa reached $33 billion in October, the highest monthly total for almost two years, Moody’s Investors Service said in a report on Thursday. “The market is being driven by quantitative easing and interest-rate announcements,” the credit-rating company said.

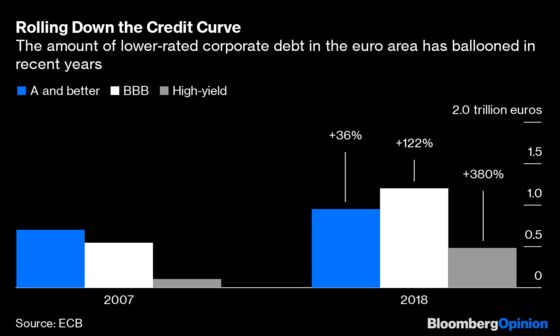

And in the past decade or so, the amount of corporate debt with ratings of BBB, the bottom of the investment grade category, has surged to surpass the total graded at A or better, the ECB notes.

The central bank estimates that BBB securities now comprise about 34% of the bonds owned by investment funds, up from 29% at the end of 2013. Junk debt accounts for about a fifth of their holdings, up from 15%. Meantime, the share of what the central bank deems to be “highly liquid bonds” in portfolios has dropped to 30% from 40%.

That’s a worry for the ECB:

Given the associated credit and liquidity risk, elevated and increasing exposure of non-bank financial intermediaries to such assets could result in greater losses, should, for example, the corporate credit cycle turn. And possible downgrades from BBB to sub-investment-grade ratings pose a risk in terms of forced asset sales due to investment mandate restrictions.

That warning was echoed Thursday by the Organization of Economic Co-operation and Development. “Sustained negative interest rates at longer maturities would likely incentivise insurers and pension funds to rebalance their portfolio from safe assets into risky assets, with ensuing risks for their clients,” it said. “This would increase the chances of incurring financial losses, in particular during a downturn.”

So far, those risks haven’t materialized. The ECB notes that Woodford, H2O and GAM were “idiosyncratic events” occurring in a “benign market environment.”

But with the outlook for growth and inflation deteriorating, the central bank isn’t likely to be able to reverse either its negative interest-rate policy or its bond-purchase program for the foreseeable future. That leaves investors hunting for the higher yields available from riskier securities — and praying for the longevity of that benign market environment.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.