(Bloomberg Opinion) -- The European Central Bank will doubtless cut its overnight deposit rate even deeper than the current -0.4% at its next meeting in September. That doesn’t mean it’s the right way to try to breathe life into the euro zone economy. It might just make things worse.

By the time the ECB’s governing council gets around to making the cut official, it’s highly likely that the benchmark yield on 10-year German bonds will already be deeper in negative territory than the central bank’s deposit rate. HSBC analysts reckon 10-year bunds will end 2019 at a mind-boggling -0.8%. You now have to pay to hold any kind of German debt from the shortest maturities right out to three decades. As my colleague Mark Gilbert wrote this week, the bond market has gone through the looking glass.

Given the expectation of the ECB cut, it’s no surprise that traders are pricing in more stimulus. But we’re entering dangerous territory here, not least because the plunge in yields is also dragging down long and ultra-long maturity bonds. There’s something seriously wrong in the euro area when lending money to Austria for 100 years produces an annual return of about 75 basis points.

That longer duration bonds are behaving like this isn’t just a concern for yield-starved bond investors, it also represents a potentially critical problem for the real economy. That’s because it removes the incentive for the finance industry to take risk: If lending overnight yields only slightly less – or sometimes even more – than lending for longer-term investment, then why bother extending credit? German debt already yields more for three-month paper than it does three-year bonds, a phenomenon known as an inverted yield curve.

Such inversions usually indicate a recession is headed our way, but they can actually cause recessions too if they’re prolonged. They create a disincentive to invest if the so-called “time value of money” (the higher cost that debt issuers usually pay for borrowing longer) stays reversed for a protracted period.

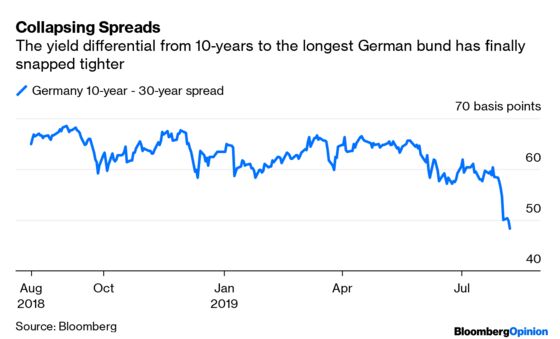

The recent plunge in yields in the 10-year to 30-year range is the really scary bit of this phenomenon and is the last domino to fall. The longest maturity debt is falling in yield faster than shorter-dated bonds. The traditional yield curve, where interest rates rise as durations get longer, is imploding.

This creates big problems for Europe’s finance firms. The fundamental nature of banking is to borrow short and lend long. Having overnight borrowing rates that are higher than 10-year bond yields turns everything upside down, resulting in collapsing net interest margins and profitability.

It creates even bigger problems for the continent’s savings industry. Pension funds and insurers in need of long-term assets to match their liabilities have been forced into a hunt for any positive yield. With the ultra-long yields plunging too, where can they turn now?

One can sympathize with the ECB chief Mario Draghi, who has recognized the limitations of monetary policy in fixing the euro zone’s ills and has pleaded with the bloc’s political leaders to use fiscal policy to help (a plea that Berlin appears ready to ignore). It’s hard to think about raising rates when everyone else is cutting, from Jay Powell at the U.S. Federal Reserve to Adrian Orr at New Zealand’s Reserve Bank. Draghi and his successor Christine Lagarde probably won’t want to make the euro stronger when Europe’s manufacturers are already struggling.

But permanent easing isn’t working, with the bulk of the money being printed ending up parked back at the ECB. Until Europe’s policymakers work out a way to bring this to an end, expect the bond madness to worsen.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.