Frankfurt, We Have a Problem. Bond Yields Are Rising

(Bloomberg Opinion) -- It’s less than a year since European Central Bank President Christine Lagarde was forced to backtrack after her comment that “we’re not here to close spreads” roiled bond markets. As rising U.S. Treasury yields drive European borrowing costs higher, she now faces the prospect of having to intervene to cap outright levels.

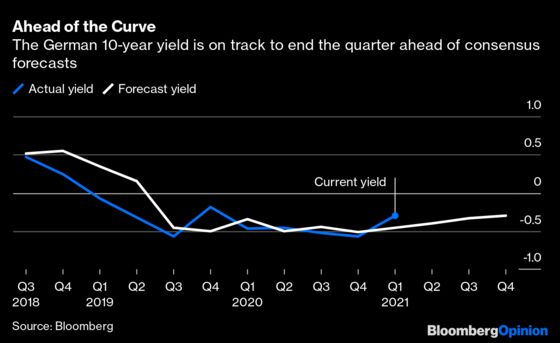

With commodity prices near an eight-year high, governments increasing their fiscal support for local economies and vaccine successes stoking optimism about an end to lockdowns, 10-year U.S. yields have climbed to their highest in a year. Correspondingly, the 30-year German yield has turned positive, rising to 0.2% from -0.2% in three short months.

That’s spooked the central bank. “The ECB is closely monitoring the evolution of longer-term nominal bond yields,” Lagarde said Monday. “We are watching long rates closely,” governing council member Francois Villeroy de Galhau said later that day. “We will ensure they remain favorable.” As Jim Reid, head of macro strategy at Deutsche Bank AG, points out, it’s remarkable that central bankers are feeling motivated to intervene verbally when German 10-year yields are still negative 0.3%.

While the ECB is understandably worried about the recent debt market moves, the U.S. Federal Reserve is less troubled. “It’s a statement of confidence on the part of markets that we will have a robust and complete recovery,” Fed Chair Jerome Powell said Tuesday when asked about the rise in yields. Given the more robust outlook for U.S. growth, he can afford to be more relaxed than his peers in the euro zone.

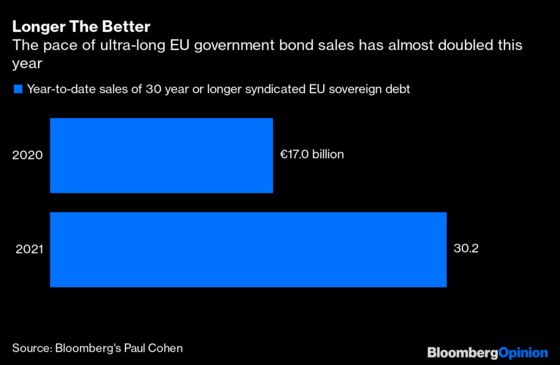

There is sufficient flexibility built into the 1.85 trillion euro ($2.25 trillion) pandemic bond-buying program for the ECB to increase its purchases and shift its support to longer-dated debt. But it can only acquire bonds with up to 31 years to maturity, while increasingly both European governments and the European Union itself have been issuing even longer-dated debt, out to 50 and even 100 years.

With the 750 billion euro pandemic Recovery Fund agreed last summer needing to be paid for, there’s a pressing requirement to sell a vastly increased amount of super-long maturity debt. And with the EU 50-year bond now yielding a positive 0.44%, having been negative in yield in December, this pandemic bailout is no longer for free. So, Frankfurt, there is a problem.

Acting to damp this jump in yields would sail perilously close to formal yield curve control, a step the ECB will be reluctant to take as its pandemic remit has already been tested once in the German constitutional court. So for now the central bank will restrict itself to trying to talk yields lower. As with all attempts to jawbone markets, though, at some point the authorities have to prove their message has bite.

The ECB has been careful to give itself some wiggle room with the introduction this year of a new and somewhat vague focus on keeping financial conditions favorable at least until the end of the crisis. While this includes corporate credit spreads, the value of the euro, loan rates and other metrics, the most important component is still benchmark government yields. And this remains by far the most easy for market participants to monitor.

The speed of the move in European government bonds, which has seen Germany’s benchmark 10-year yield surge to that eight-month “high” of -0.3%, has caught the market by surprise. Analysts surveyed by Bloomberg, who have consistently overestimated government borrowing costs, hadn’t expected bunds to reach their current level until the end of the year.

As with the recent strength in the euro, caused largely by dollar weakness, the EU’s financing rates are being buffeted by outside influences largely beyond its control. After the worst downturn in living history the recovery of Europe is at stake if higher long-term borrowing costs threaten to make its convalescence less comfortable.

The ECB has been at pains to reassure markets it has sufficient firepower to support a perennially underperforming economy. If the so-called reflation trade continues to imperil its efforts, it may be forced to unleash the bazooka of yield curve control.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.