Drill, Baby, Drill Hasn’t Died in the U.S. Shale Patch

(Bloomberg Opinion) -- Conditions in the U.S. shale patch look dismal. Nearly two years after the number of horizontal rigs drilling for unconventional oil peaked, they bottomed out six months ago at just 22% of their previous levels. Rather than a robust rebound, the recovery in activity has been a tired grind upward.

That’s not a description of the U.S. upstream oil industry at the start of 2021. Instead, it’s how things looked in late 2016, as the industry licked its wounds from the crash in crude prices below $30 a barrel after four years when it hovered around $100. If you paid too much attention to the gloomy outlook at the time, you’d have missed the way that the U.S. was just 18 months away from overtaking Russia and Saudi Arabia to become the world’s biggest crude producer.

The selloff in oil prices over the past two weeks indicates this pattern could be repeating a second time. The oil majors are still shying away from shale after getting burned by last year’s looking-glass dip below zero. For the industry as a whole, though, it’s still too soon to say whether the productivity benefits that allowed shale to recover from its last slump have gone away, or whether we’re about to see another round of improvements.

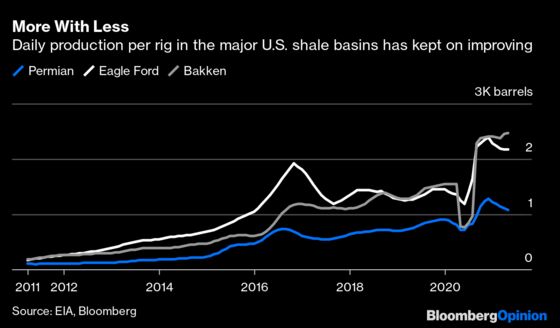

There’s certainly evidence for the latter position. The amount of oil produced per rig, per day in the major oil patches has soared in recent months, to roughly twice its early 2016 levels in Texas’s Permian and Eagle Ford basins and more than three times in the Great Plains’ Bakken.

Such estimates tend to be volatile when the market is in turmoil. Drillers will shut down their least productive wells first, leaving the remaining group skewed towards the very best strikes. Still, the pattern has been persistent enough this year that it’s hard to deny genuine improvements have been made. The Permian’s 203 rigs operating in February are expected to produce 4.3 million barrels in April . The 199 rigs in September 2016 produced less than half that amount, at 2.1 million barrels.

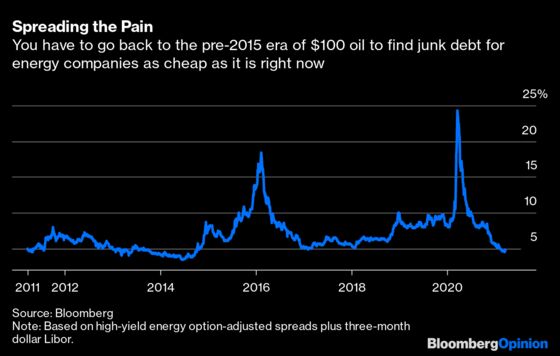

All this is helped by a much more supportive environment for credit, which is to shale oil as oil is to the economy — a still-indispensable fuel. Option-adjusted spreads for junk energy debt — a measure of the premium over benchmark borrowing costs that smaller exploration and production companies have to pay to finance their activities — have fallen from 22.4% 12 months ago to just 4.6% Tuesday.

When combined with the general slump in interest rates as the Federal Reserve works to spark the economy back to life, borrowing costs for shale drillers are now cheaper than they’ve been at any point since 2014, when crude was north of $100 a barrel, as Bloomberg Intelligence’s Spencer Cutter points out.

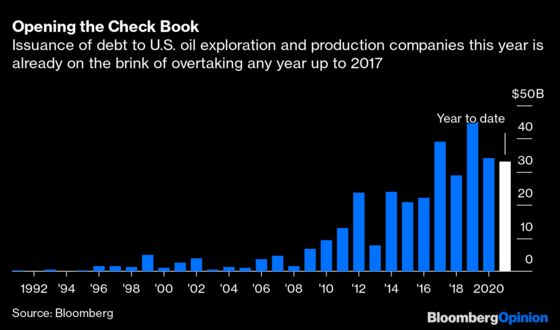

Oil producers haven’t been just sitting back and admiring that slump in finance costs. Indeed, less than three months into the year, issuance of new bonds and preferred stock to the U.S. upstream sector is already a whisker away from overtaking funding during the whole of last year, and is ahead of every other year in history barring 2017 and 2019.

Some of those funds will go to repair still-tatty balance sheets and refinance debts at lower rates — but once that fundamental work is done, E&P companies will get back to their everyday business of finding new wells and developing them.

As my colleague Liam Denning has argued, current levels of $50 a barrel to $60 a barrel are quite sufficient to bring on new production outside the ranks of OPEC+, while being mostly insufficient for members of the cartel to balance their budgets and external accounts.

That’s a wicked position to be in. All the drama of last year’s swings in the oil market, far from killing off U.S. oil production and delivering the future to Saudi Arabia and Russia, have only succeeded in driving down output to the 11 million barrels-a-day levels it was trending at late in 2018. Next year will see output of 12 million barrels, according to the Energy Information Administration, which would have been a record in any month up to February 2019.

After the initial shock, the oil patch is learning to survive and thrive with lower prices, stealing OPEC+’s traditional role as the industry’s swing producer. For drillers elsewhere in the world, that’s a troubling prospect.

The Energy Information Administration reports the rig count with a two-month lag to ensure that only fully operational wells are counted towards the production total.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.