(Bloomberg Opinion) -- France SA’s romance with the Chinese car industry could be nearing its end.

Dongfeng Motor Corp., a state-owned giant that runs joint ventures with PSA Group, Nissan Motor Co. and Honda Motor Co., is looking at options for its 12.2% stake in PSA including a sale or bond issuance backed by the stock, people familiar with the matter told Bloomberg News on Thursday.

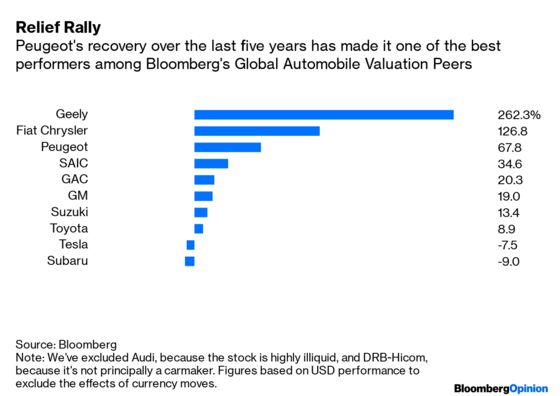

On purely financial terms, such a move makes a great deal of sense. Dongfeng bought the shares as part of a 2014 bailout of the maker of Peugeot and Citroen cars, brokered by the French government. That investment has done rather well: PSA has seen the third-best share performance in Bloomberg’s Global Automobile Valuation peer group over the past five years, after Geely Automobile Holdings Ltd. and Fiat Chrysler Automobiles NV. The 800 million euros ($897 million) Dongfeng spent at the time is now worth around 2.2 billion euros.

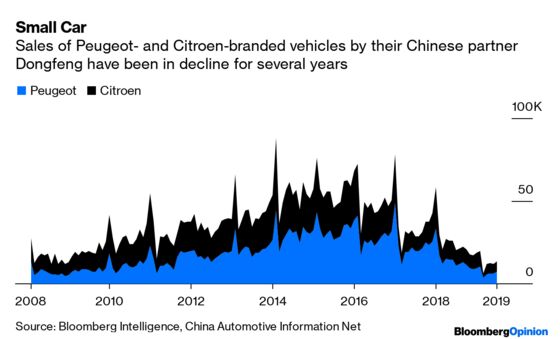

On top of that, the operational ventures that underpinned the shareholding have seen better days. Listed subsidiary Dongfeng Motor Group Co.’s sales of Peugeot- and Citroen-branded cars fell by about half in the first six months from a year earlier and are running at less than a quarter of their level in 2015. In the key crossover SUV market, models like Citroen’s C5 Aircross and Peugeot’s 4008 have simply failed to catch fire against competition from Asian and domestic rivals.

Unless there’s a serious pick-up in the second half, Dongfeng’s PSA production lines, dedicated to turning out as many as 600,000 vehicles a year, will be running at little better than 25% utilization – levels at which it should be hard for the business to make money. Losses at Dongfeng’s PSA venture were already running at the equivalent of $251 million in 2018; it would hardly be surprising if they were worse this year.

Management in China clearly see little sign that sales are about to pick up. Dongfeng’s dealer network for PSA-branded cars shrank by almost 80% between 2015 and 2018, and now stands at just 666 outlets compared with 1,186 for Renault-Nissan marques. The showrooms that remain suffer low productivity, shifting an average of 400 PSA vehicles each in 2018 compared with 1,431 at Nissan outlets and 761 at Honda-branded locations. (For what it’s worth, Renault does even worse, on just 204 vehicles).

There’s a more proximate issue, too. Cash has been looking a little tight for Dongfeng’s listed subsidiary of late, owing largely to a huge increase in working capital, two years of negative Ebit, and net debt of 2.15 billion euros that was running at 8.1 times Ebitda at the end of December. In the 2018 fiscal year, operating cash flows actually turned negative to the tune of about 1.25 billion euros, a relatively rare event for carmakers that aren’t in the grip of a financial crisis or corporate scandal.

Dongfeng still has ample liquidity. Its ratio of short-term assets to short-term liabilities was 1.36 at the end of December, above the industry average. But China’s auto market is grim, with sales declining from a year earlier for 12 straight months even as the government ratchets up pressure to spend money on the switch to electric vehicles. Faced with such headwinds, 2.2 billion euros could come in handy.

At present there’s no word that Dongfeng is planning to unwind the JV to manufacture PSA cars in China – but it would probably welcome such an outcome, especially if it could persuade its European affiliate to pay to take more control of the partnership in the manner of the deal last year between BMW AG and Brilliance China Automotive Holdings Ltd.

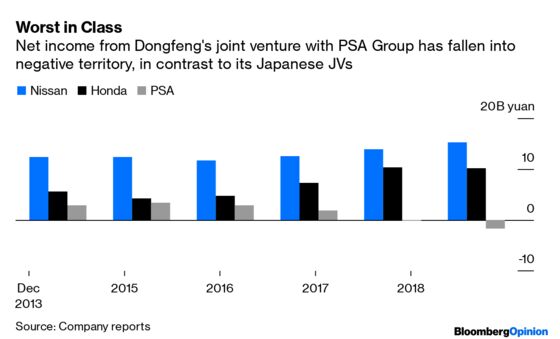

Dongfeng’s partnerships with Nissan and Honda are clearly the better performers, and PSA may feel it needs more of a free hand to turn around its Chinese operation. If a sale of a strategic stake can help ease the path toward that happier outcome, both sides stand to benefit.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.