Economists Join Congress in Not Worrying About the Deficit

(Bloomberg Opinion) -- For at least a generation, economists have been all but unanimous in warning Congress about the dangers of excessive government debt. Yesterday the U.S. House Budget Committee held a hearing about whether debt might not be so bad after all — and the star witnesses were economists.

The committee heard testimony about two rising schools of thought that at first seem to agree about the debt. But proponents of so-called modern monetary theory and those of what might be called the “New View” have deep disagreements about how the economy works.

First, some history: The consensus among economists has long been that, while budget deficits are sometimes necessary (in case of war, for example, or recession), they are ultimately a threat to economic growth. That’s because when the government borrows, it “crowds out” investment in the private sector. At this point, one of three things can happen: Private investors competing over the smaller pool of savings can bid up interest rates until some borrowers are pushed out of the market; foreign savers can step in and add to the pool of savings; or some combination of both. In any case, future Americans will be worse off, either because domestic investment will be lower or foreign debt will be higher.

So economists customarily recommended that Congress get serious about reducing the long-term deficit. Congress mostly didn’t listen, though the U.S. government did run a surplus for a few years in the late 1990s.

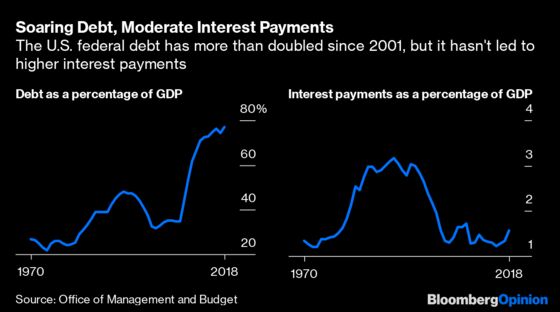

After 2000, everything changed. A mixture of recession, tax cuts, wars, a global financial crisis and the Great Recession sent the deficit soaring. Rather than rising, however, interest rates fell — and rather than being saddled with billions in net payments to foreigners, the U.S. earned net income from overseas.

Advocates of modern monetary theory find these facts encouraging. They argue that the sluggish growth of the last two decades has been caused by deficits that were too small, not too large. If the large deficits were truly unsustainable, they argue, they would have led to rising inflation, not an economic downturn. But inflation has been falling since the 1980s.

Underlying this hypothesis is the view that the economy is fundamentally demand-driven. Investment occurs in response to rising sales, not falling interest rates. Rising sales, in turn, are the result of more spending — by either the government or consumers. This leads modern-monetary theorists to favor such programs as a federal job guarantee or a Green New Deal to ensure the flow of spending continues. They do not favor cutting the deficit.

The proponents of the New View don’t either — but they see very different forces at work. As a result of an aging population, global uncertainty and unpredictable changes in technology, they say, there is an unprecedented international demand for safe assets such as government bonds. Private-sector investments, meanwhile, have had trouble expanding in the wake of the Great Recession. Tech startups that offer potentially enormous returns can attract financing, but small businesses can’t.

This is ultimately a supply-side problem: The economy is lacking the capital investment necessary for healthy growth. To address this, proponents of the New View recommend that the government either cut taxes on business investment or increase spending on infrastructure. In effect, they see government as a financial intermediary, borrowing cheaply from the pool of risk-averse savers to fund investments that would increase long-run productivity.

So both schools of thought are more accepting of budget deficits than the previous consensus. But their rationales differ. And members of Congress should be aware that while many economists say the deficit is not a problem now, that’s not the same as saying it never will be. More generally, politicians should be wary of approving transformative spending programs without considering how they will be financed when economic circumstances change.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

©2019 Bloomberg L.P.