(Bloomberg Opinion) -- If investors had been willing to give Deutsche Bank AG’s mammoth overhaul the benefit of the doubt, they have been just given cause to think again.

It's now clear that one of the key assumptions underpinning the fixed-income powerhouse’s July 7 restructuring plan was too optimistic – specifically that interest rates wouldn't fall as much as the market now expects them to. Without any relief from this deeper pain, Deutsche Bank’s goal of growing revenue at the businesses it wants to keep by 2% a year through 2022 is at risk.

“It does represent a revenue pressure for us, and all of the banks, if rates from here go down further,” Chief Financial Officer James von Moltke told Bloomberg Television on Wednesday as the bank posted its biggest quarterly loss since 2015.

If the European Central Bank doesn’t offset any cuts with, for example, the tiering of deposits – where it charges lenders less to park some of their surplus cash with it – the shift could have “a significant impact on revenues relative to our current expectations,” the company said in a statement. The ECB starts meeting today to set interest rates, and economists are divided on whether it will introduce such a measure if does decide to lower.

For a firm struggling to rebuild credibility with investors after five restructuring plans in four years, just a hint that its latest overhaul may be built on shaky foundations is unhelpful. Odder still, though, is that interest rate assumptions in the euro zone haven’t shifted much in the two weeks since the bank announced the plan. That makes the apparent change all the more troubling.

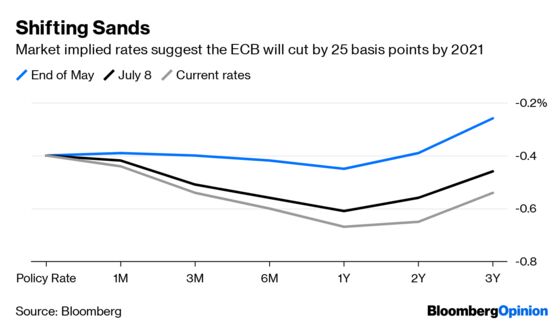

At the end of May, market implied rates pointed to little change in the ECB's policy in the coming two years. By the time of Deutsche Bank's statement earlier this month, expectations were for rates to decline by about 16 basis points. Now, the market is anticipating a drop of 25 basis points by 2021, as this chart shows.

Von Moltke says Germany’s biggest bank had to make “some planning assumptions” and “those happened to be at the end of May” – but it seems odd not to have spelled out the impact of the shift in rate expectations in June when it announced the plan to investors the following month.

To me, it looks worryingly like hope rather than realism may have formed the basis for some of the key estimates in the revamp. And remember this isn’t a small piece of tinkering. It’s an ambitious effort that will see the bank cut one in five jobs and exit the equities trading business. It will be especially challenging to keep growing the core bank as worried clients are wooed by rivals.

Deutsche Bank’s second-quarter numbers highlight other concerns, too. Revenue from fixed-income trading fell 11%, more than at its U.S. peers. Income from advising on deals – remember that corporate finance will be the heart of the new Deutsche Bank – dropped by a staggering 30%, trailing rivals that have reported so far. UBS Group AG reported an 18% increase on Tuesday.

Deutsche Bank Chief Executive Office Christian Sewing acknowledged this isn't good enough, and the investment bank must do better, saying he won't make excuses. Unfortunately, it's a refrain that has become all too familiar to investors.

While the German banking behemoth remains committed to shrinking its balance sheet by about 250 billion euros, the composition of its new bad bank has also changed from two weeks ago. The company now intends to keep more revenue-generating assets within the core bank. The bad bank's revenue will now be about 1.8 billion euros, down from the 2.5 billion euros the firm estimated on July 7. Sales at the investment bank are expected to rise by almost the same amount. While Sewing has said the adjustment reflects a desire to minimize the damage to the franchise, it’s still not clear exactly how the lender is deciding whether to keep or shed assets.

After abandoning talks to merge with smaller rival Commerzbank AG in April, Sewing has been under tremendous pressure to show what the firm can do on its own to restore profitability. If he is to stand a chance of delivering his turnaround effort, he cannot afford to fumble the execution. Counting on help from monetary policy makers to make his plan work isn’t a great start.

--With assistance from Mark Gilbert.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.